Key Takeaways

- E-commerce growth and strategic distribution partnerships are driving increased revenue and sales velocity.

- Transition to subscription model and efficient supply chain management enhance recurring revenue and margin stability.

- Persistent commodity price pressures, supply chain issues, and elevated expenses challenge Laird Superfood's profitability despite reliance on e-commerce for growth.

Catalysts

About Laird Superfood- Manufactures and markets plant-based natural and functional food in the United States.

- Laird Superfood's strategic focus on e-commerce, particularly through Amazon, achieved a significant 32% year-over-year growth and is expected to drive further revenue increases due to improved inventory management and targeted marketing.

- The expansion of wholesale distribution, including new partnerships with major retailers like Kroger and Safeway Albertsons, is projected to enhance sales velocity and broaden revenue channels.

- The transition to a subscription model in the direct-to-consumer segment, which now comprises nearly half of DTC revenue, is likely to bolster recurring revenue and customer loyalty.

- The introduction of a new 750-milliliter liquid creamer package, aligning with category norms, is anticipated to boost sales and optimize shelf space, positively impacting revenue and potentially net margins due to improved efficiency.

- Effective supply chain management, including the identification of new suppliers to mitigate product shortages, positions the company to better meet demand, supporting stable revenue growth and margin sustainability amidst cost pressures.

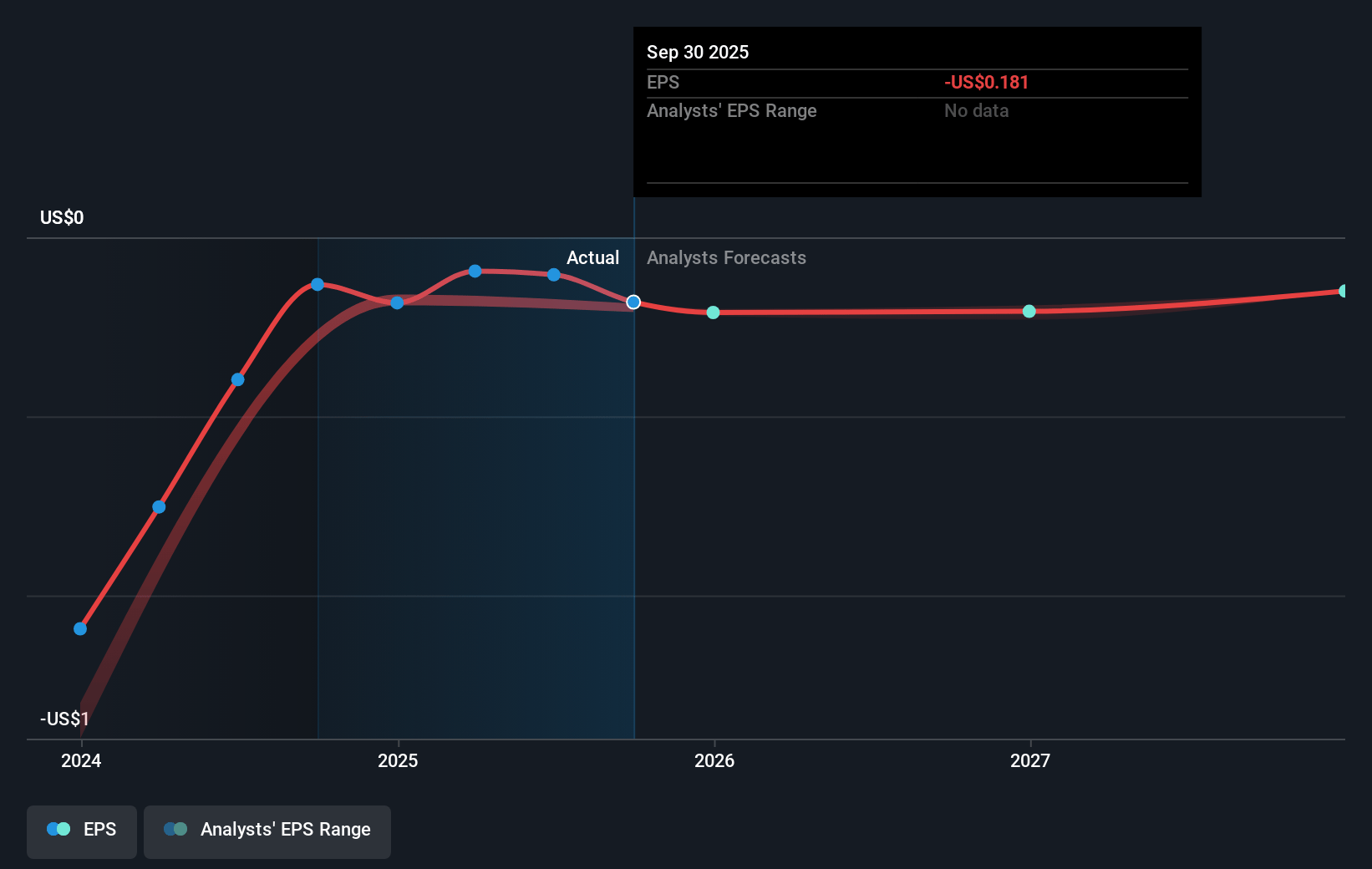

Laird Superfood Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Laird Superfood's revenue will grow by 20.0% annually over the next 3 years.

- Analysts are not forecasting that Laird Superfood will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Laird Superfood's profit margin will increase from -4.2% to the average US Food industry of 6.6% in 3 years.

- If Laird Superfood's profit margin were to converge on the industry average, you could expect earnings to reach $5.0 million (and earnings per share of $0.41) by about April 2028, up from $-1.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 37.7x on those 2028 earnings, up from -31.0x today. This future PE is greater than the current PE for the US Food industry at 17.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Laird Superfood Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent commodity price pressures in coffee, cacao, and coconut milk powder could squeeze margins and impact profitability if these costs do not decrease as anticipated. This could result in lower gross margins and net income.

- The company’s out-of-stock issues due to supply chain constraints have already led to an estimated $1 million in lost sales for Q4 2024, which could affect revenue and financial performance if such issues persist.

- The decision to trade gross margin percentages for gross margin dollars in the face of commodity cost pressures may result in temporary reductions in profitability and potentially impact net margins and earnings.

- The company's reliance on growth through e-commerce channels like Amazon poses a risk if there are shifts in consumer shopping behavior or if Amazon's terms or algorithms change in a way that negatively impacts visibility and sales, which could affect revenue stability and growth.

- Elevated operating expenses, including marketing investments and non-cash expenses such as stock-based compensation, could challenge the company's ability to achieve profitability and may weigh on net income and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.0 for Laird Superfood based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $74.9 million, earnings will come to $5.0 million, and it would be trading on a PE ratio of 37.7x, assuming you use a discount rate of 6.2%.

- Given the current share price of $5.48, the analyst price target of $13.0 is 57.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.