Last Update01 May 25

Key Takeaways

- Zevia is poised for growth with better-for-you sodas and expanded distribution, especially in Walmart, enhancing market penetration.

- Marketing and new flavors are set to boost brand awareness and sales, with cost-saving strategies aimed at improving net margins by 2026.

- Increased marketing efforts and distribution changes may squeeze margins and delay expected sales growth, hindering short-term profitability and market expansion.

Catalysts

About Zevia PBC- Develops, markets, sells, and distributes zero sugar beverages in the United States and Canada.

- Zevia is positioned to benefit from the fast-growing better-for-you soda category, which is expanding at a much higher rate than the conventional soda market. This shift is expected to positively impact revenue.

- The company has plans to amplify its brand through increased marketing efforts, focusing on driving awareness and trial. This should help expand its consumer base and increase net sales over time.

- Zevia is launching new flavors and variety packs, which are anticipated to drive incremental sales volume and potentially higher margins as consumers shift from trial packs to straight flavor purchases.

- The expansion of distribution, most notably with an increased presence in Walmart stores and enhanced shelf placement in grocery stores, is expected to increase market penetration and drive volume growth.

- Cost savings initiatives, along with further optimization in product portfolio, are expected to improve net margins and lead to positive adjusted EBITDA by 2026.

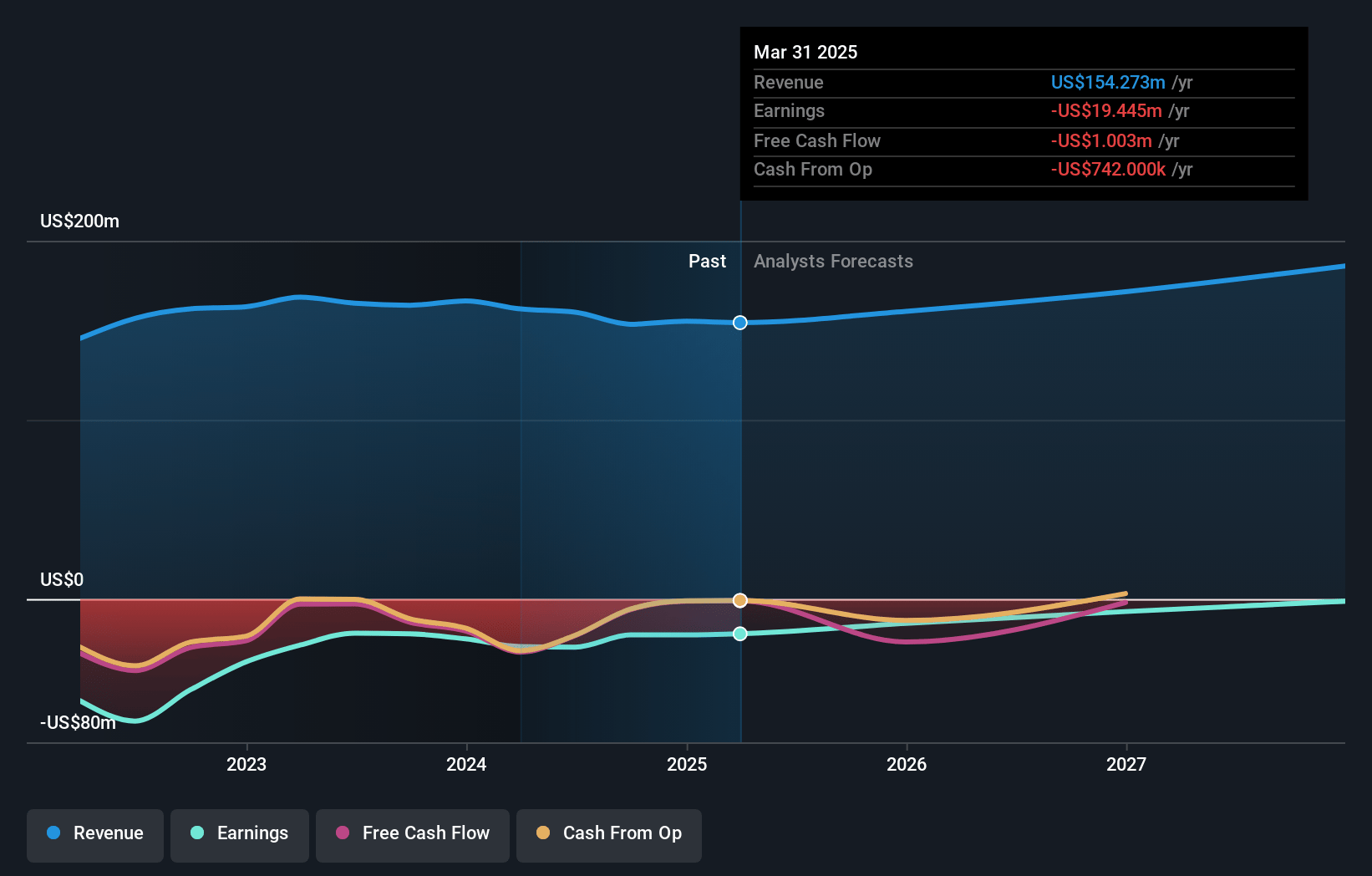

Zevia PBC Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Zevia PBC's revenue will grow by 6.6% annually over the next 3 years.

- Analysts are not forecasting that Zevia PBC will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Zevia PBC's profit margin will increase from -12.9% to the average US Beverage industry of 11.5% in 3 years.

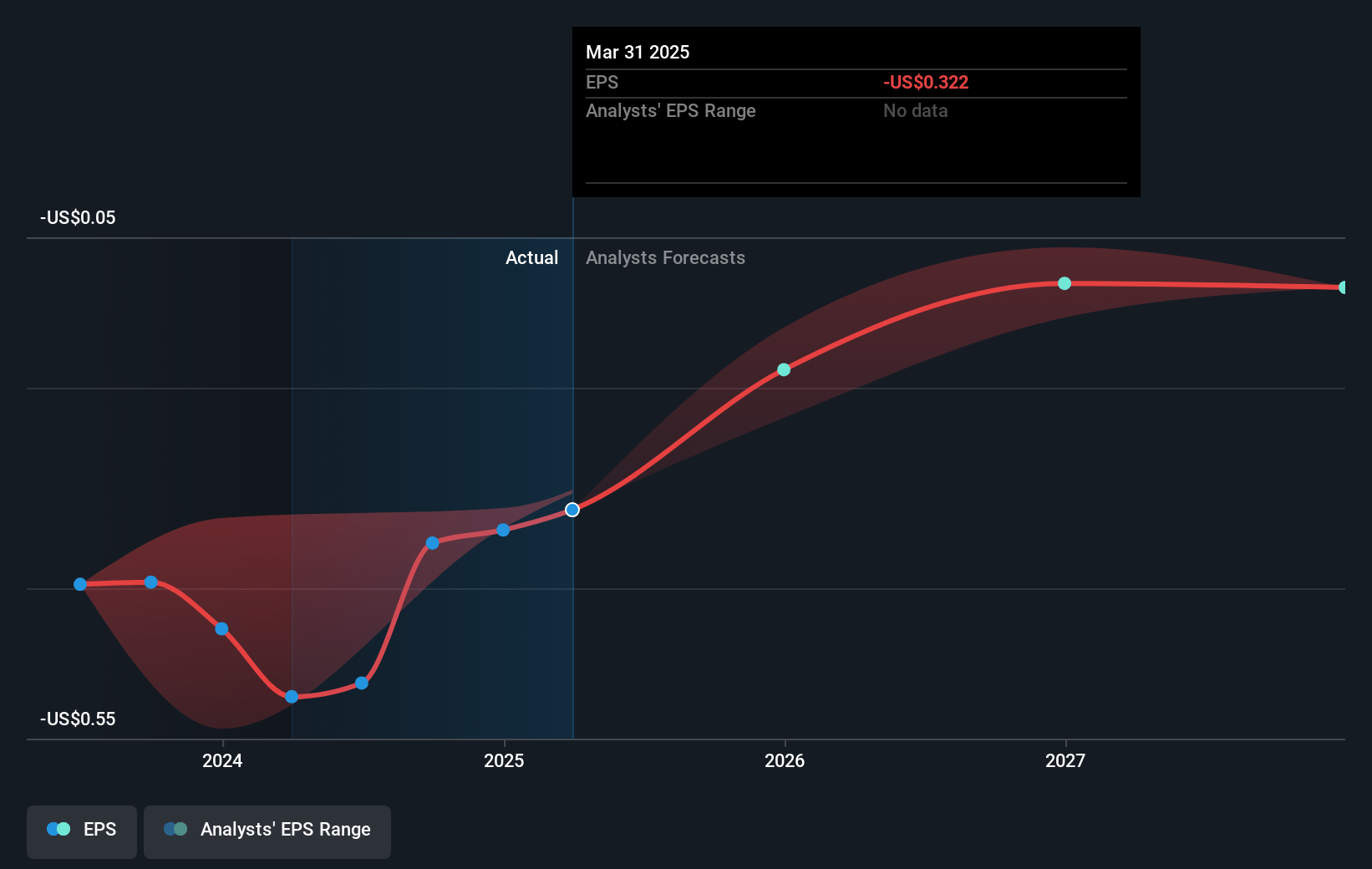

- If Zevia PBC's profit margin were to converge on the industry average, you could expect earnings to reach $21.7 million (and earnings per share of $0.25) by about May 2028, up from $-20.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.3x on those 2028 earnings, up from -7.0x today. This future PE is lower than the current PE for the US Beverage industry at 25.5x.

- Analysts expect the number of shares outstanding to grow by 6.49% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Zevia PBC Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The increase in promotional activities could squeeze margins, impacting profitability despite higher sales volumes. [Net Margins]

- The competitive environment, particularly with large retailers adjusting to bring more low and no-sugar brands, may hinder Zevia's market share expansion and revenue growth. [Revenues]

- Loss of distribution in the club and mass channels, coupled with the discontinuation of certain product lines, may lead to suppressed sales growth despite opening new distribution avenues. [Revenues]

- Despite gross margin improvements, the planned focus on significant marketing spend might not quickly convert into proportional sales growth, potentially resulting in larger adjusted EBITDA losses in the short term. [Earnings]

- The transition to a hybrid DSD model, while promising in certain regions, is a gradual process that might not yield immediate sales or profit gains as expected. [Revenues and Net Margins]

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.167 for Zevia PBC based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $6.0, and the most bearish reporting a price target of just $2.75.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $188.0 million, earnings will come to $21.7 million, and it would be trading on a PE ratio of 20.3x, assuming you use a discount rate of 6.2%.

- Given the current share price of $2.26, the analyst price target of $4.17 is 45.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.