Last Update07 May 25Fair value Increased 0.16%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- Terminating low-margin contracts and focusing on premiumization are set to improve margins and revenue growth across strategic regions.

- Strategic shifts towards non-alcoholic products and share repurchases aim to boost market segment capture and enhance earnings per share.

- Potential challenges in the U.S. and Europe, along with contract brewing exits, pose short-term revenue pressures amid complex global operations and risk of supply disruptions.

Catalysts

About Molson Coors Beverage- Manufactures, markets, and sells beer and other malt beverage products in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

- Molson Coors expects a positive impact on brewery net effectiveness, product mix, and margins in 2025 and beyond due to the termination of low-margin contract brewing agreements, which implies an improvement in net margins and earnings.

- The company is focusing on premiumization, especially in the EMEA and APAC regions, which has resulted in double-digit net sales revenue growth from their premium lager brand Madri. This ongoing premiumization is likely to enhance revenue growth and improve net margins.

- Molson Coors has announced share repurchases, already executing 40% of their 5-year program in just the first 5 quarters. This strategy is expected to drive significant EPS growth due to a reduced share count, enhancing earnings.

- A strategic shift towards non-alcoholic beverages and partnerships with leading brands like Fever-Tree positions Molson Coors to capture more market segments amid evolving consumer preferences, potentially boosting revenue growth and earnings.

- The company plans to leverage onshore production of Peroni to improve consistency, expand pack sizes, and realize cost savings, which will be reinvested to drive distribution, scale, and ultimately enhance margins and earnings.

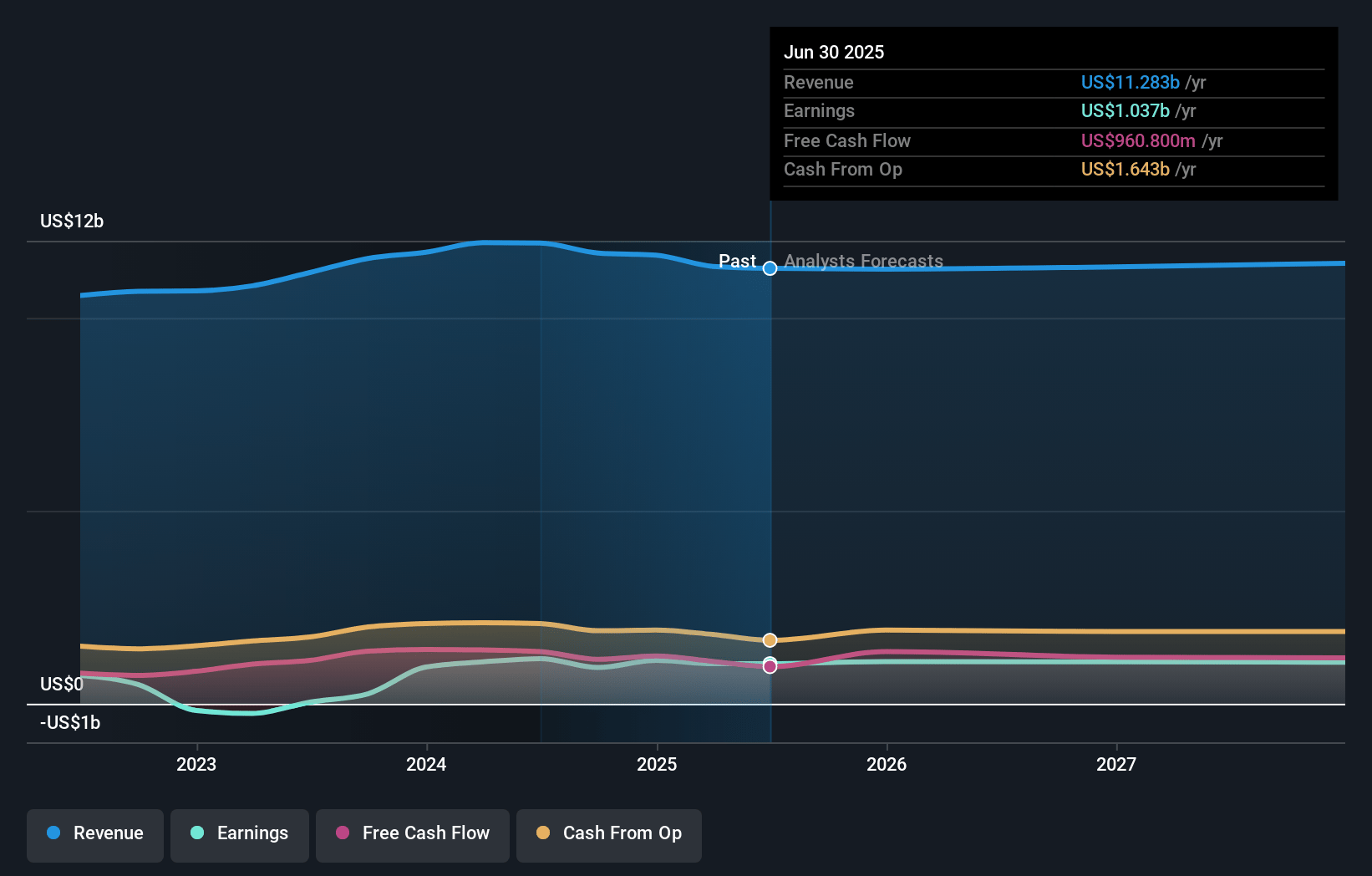

Molson Coors Beverage Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Molson Coors Beverage's revenue will decrease by 0.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.7% today to 10.5% in 3 years time.

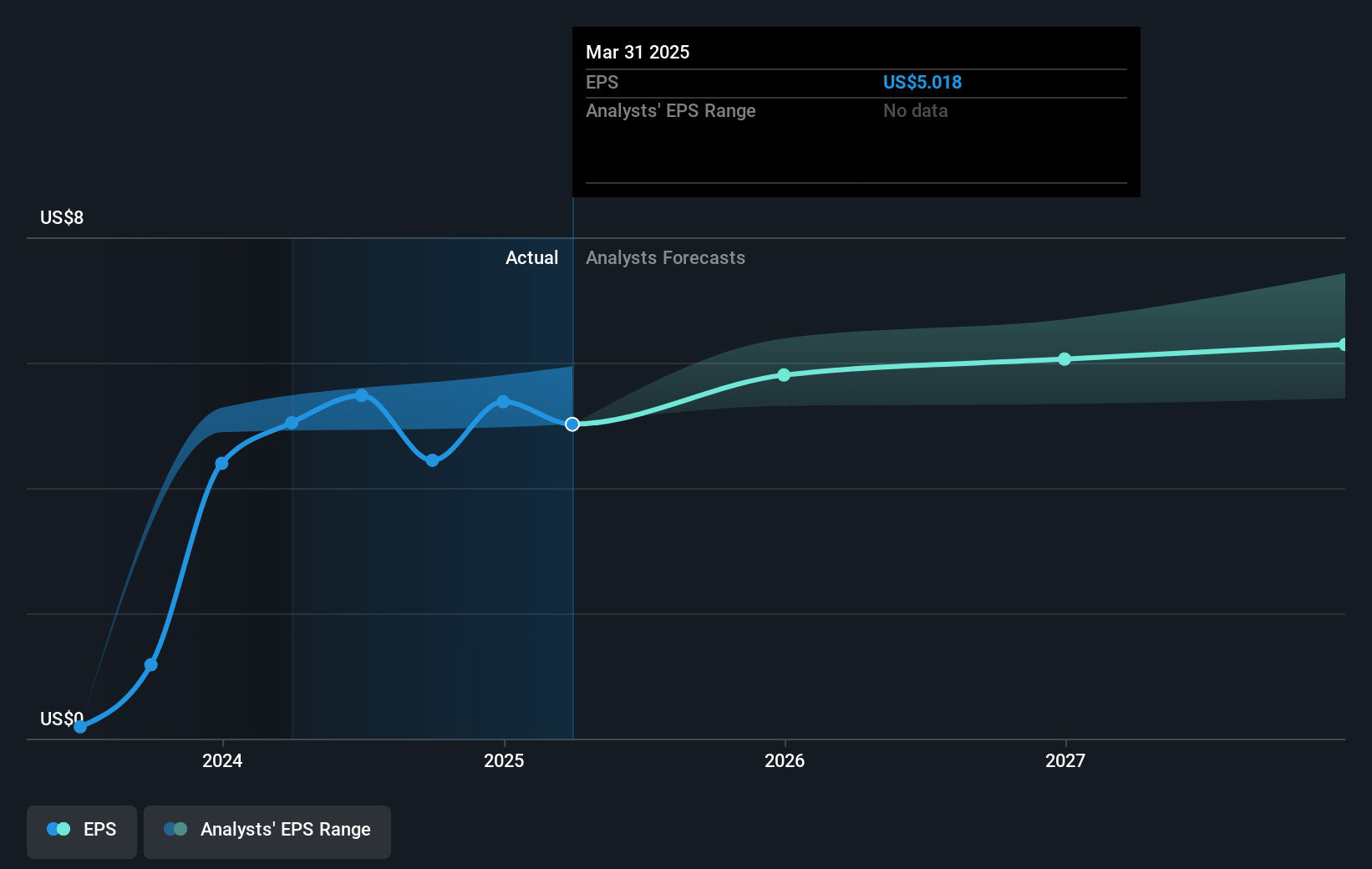

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $6.71) by about May 2028, up from $1.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.4 billion in earnings, and the most bearish expecting $1.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.4x on those 2028 earnings, up from 10.3x today. This future PE is lower than the current PE for the US Beverage industry at 29.7x.

- Analysts expect the number of shares outstanding to decline by 4.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Molson Coors Beverage Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's U.S. net sales revenue declined by 1.9% in the fourth quarter, and U.S. brand volume was down 3%, indicating potential challenges in maintaining or growing its market share and revenues in its largest market.

- The competitive landscape in the U.K. and a softer industry in Central and Eastern Europe impacted volumes, which might continue to exert pressure on revenues and margins in these regions.

- The exit from low-margin contract brewing agreements, while potentially beneficial in the long term, currently poses a volume headwind, reflecting a negative impact on its short-term revenue and financial volume.

- The company anticipates U.S. financial volume will face a headwind due to the loss of PEPs and Labatt contract brewing volumes, impacting overall short-term revenue and financial volume.

- Although there is no immediate tariff impact forecasted, potential global supply chain disruptions or geopolitical tensions could impact input costs and margins, given the complex nature of its international operations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $66.753 for Molson Coors Beverage based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $86.9, and the most bearish reporting a price target of just $54.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $11.9 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 11.4x, assuming you use a discount rate of 6.2%.

- Given the current share price of $56.9, the analyst price target of $66.75 is 14.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.