Key Takeaways

- Elevated cocoa prices and hedging uncertainties may hinder Hershey's profitability and revenue growth if costs are not managed effectively.

- Health trends and competitive pressures in international markets could challenge Hershey's traditional product sales and margin growth.

- Hershey's strategic hedging, pricing, and diversification efforts stabilize costs and supply, while innovation and market leadership drive revenue and margin growth.

Catalysts

About Hershey- Engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally.

- The elevated cocoa prices present a significant challenge for Hershey as they plan for 2026, which could pressure Hershey's ability to grow revenue and net margins if these costs are not mitigated effectively.

- Hershey's forecast includes reliance on a conservative elasticity assumption of negative one, indicating potential difficulty in achieving expected sales targets without significant pricing power, which could negatively impact revenue growth.

- Increased competitive activities in international markets, particularly in Brazil and Mexico, along with pressures from tighter competitive activity, may limit revenue growth prospects and compress margins as Hershey might have to increase spending to maintain market shares.

- The ongoing shift towards healthier consumer preferences combined with the potential emerging impact of health-focused drugs like GLP-1s could shift consumer consumption patterns away from Hershey’s traditional product categories, impacting revenue and long-term growth prospects.

- Uncertainty remains around input costs and the timing and effectiveness of Hershey’s hedging strategies for cocoa, as unexpected fluctuations in these costs could adversely impact profitability and lead to variability in earnings.

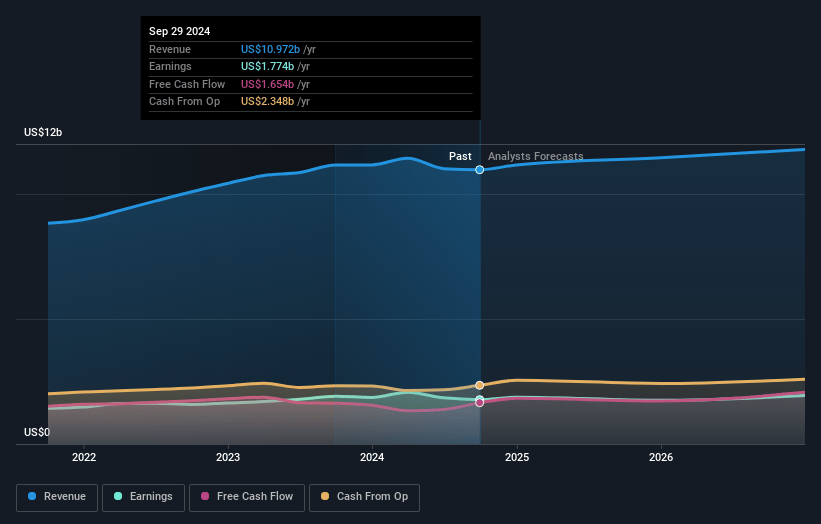

Hershey Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Hershey compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Hershey's revenue will grow by 1.1% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 19.8% today to 12.5% in 3 years time.

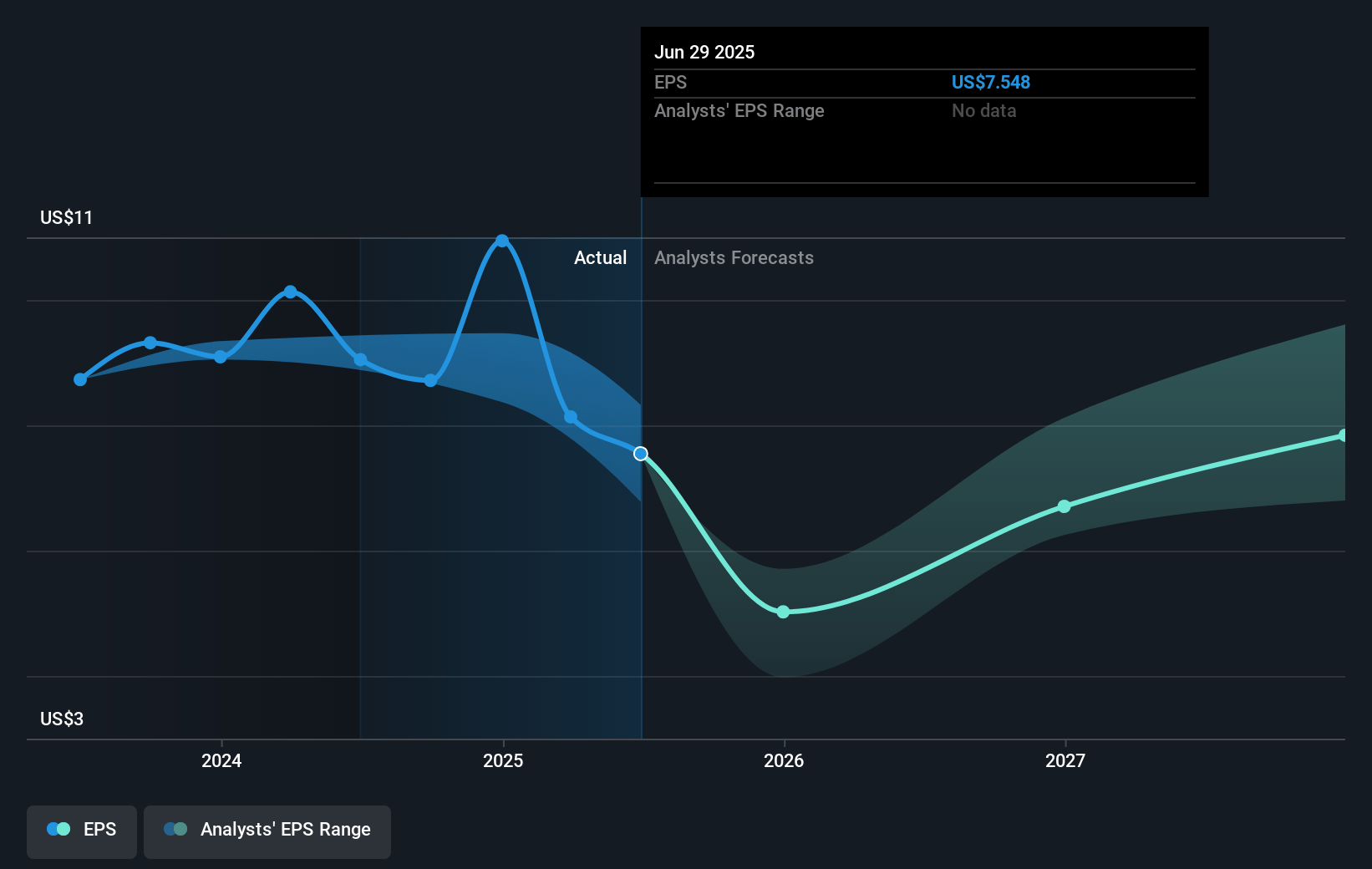

- The bearish analysts expect earnings to reach $1.4 billion (and earnings per share of $6.83) by about April 2028, down from $2.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 24.1x on those 2028 earnings, up from 15.2x today. This future PE is greater than the current PE for the US Food industry at 17.4x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Hershey Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Hershey's hedging strategy on commodities like cocoa helps mitigate price volatility, potentially stabilizing cost of goods and preserving net margins.

- Strategic pricing actions and elasticity management provide confidence in being able to take price increases without significantly hurting volume, supporting revenue growth and preserving earnings.

- The diversification of cocoa supply across multiple geographies provides resilience against supply chain disruptions, contributing to stable revenue and profit margins.

- Continued investment in innovation, especially in the sweets and non-chocolate segments, aids incremental revenue growth and revenue from newly developing consumer trends.

- Hershey's market leadership and effective competition strategies enable it to capture incremental market share, potentially leading to improved sales and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Hershey is $142.95, which represents one standard deviation below the consensus price target of $165.34. This valuation is based on what can be assumed as the expectations of Hershey's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $211.56, and the most bearish reporting a price target of just $120.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $11.6 billion, earnings will come to $1.4 billion, and it would be trading on a PE ratio of 24.1x, assuming you use a discount rate of 6.2%.

- Given the current share price of $166.6, the bearish analyst price target of $142.95 is 16.5% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:HSY. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.