Key Takeaways

- Strategic investments and operational improvements aim to boost capacity, efficiency, and margins while supporting revenue growth through increased demand for at-home meal solutions.

- Expanding into major retailers with new products is set to drive future revenue, leveraging the trend toward deli-prepared foods amid inflationary pressures.

- Reliance on major retailers and commodity price volatility poses risks to margins and profitability, amidst expansion and increased marketing expenses.

Catalysts

About Mama's Creations- Manufactures and markets fresh deli-prepared foods primarily in the United States.

- Strategic CapEx investments at the Farmingdale facility have doubled chicken capacity and are expected to reduce labor hours, resulting in enhanced revenue generation and gross margin improvement.

- Mama's Creations is capitalizing on a shift in consumer behavior toward deli-prepared foods, combined with inflationary pressures on restaurant pricing, which increases the demand for at-home meal solutions and supports revenue growth.

- In-house trimming of chicken is expected to support over half of the company's needs, resulting in significant cost savings and future gross margin expansion.

- Expansion into major retailers like Walmart, Costco, Albertsons, and Amazon Fresh with new product launches and increased distribution is expected to drive future revenue growth.

- The company's focus on operational improvements, including ERP rollout, warehouse management systems, and developing a robust leadership team, is expected to enhance net margins through efficiency gains and operational discipline.

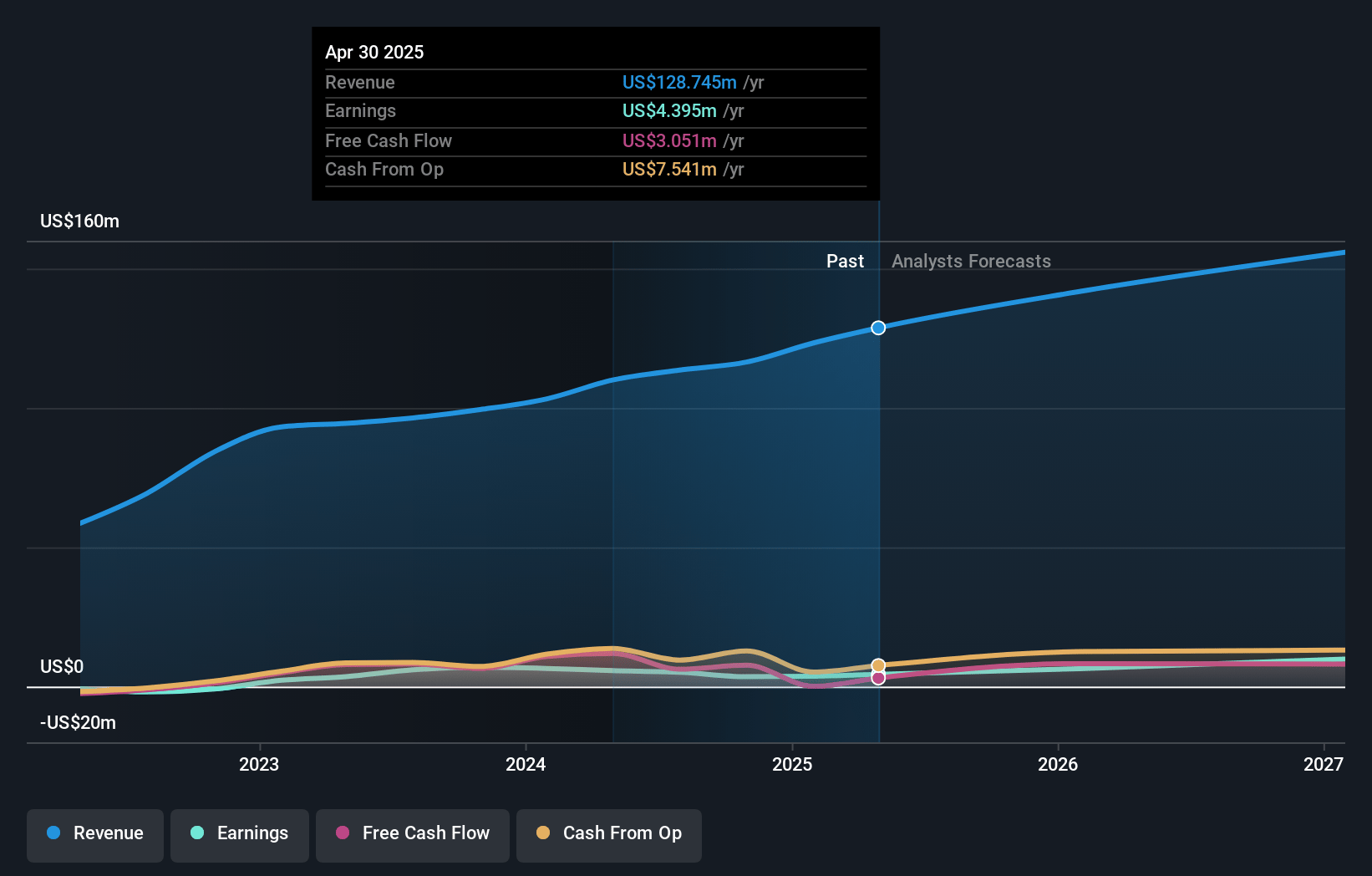

Mama's Creations Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Mama's Creations's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.0% today to 8.9% in 3 years time.

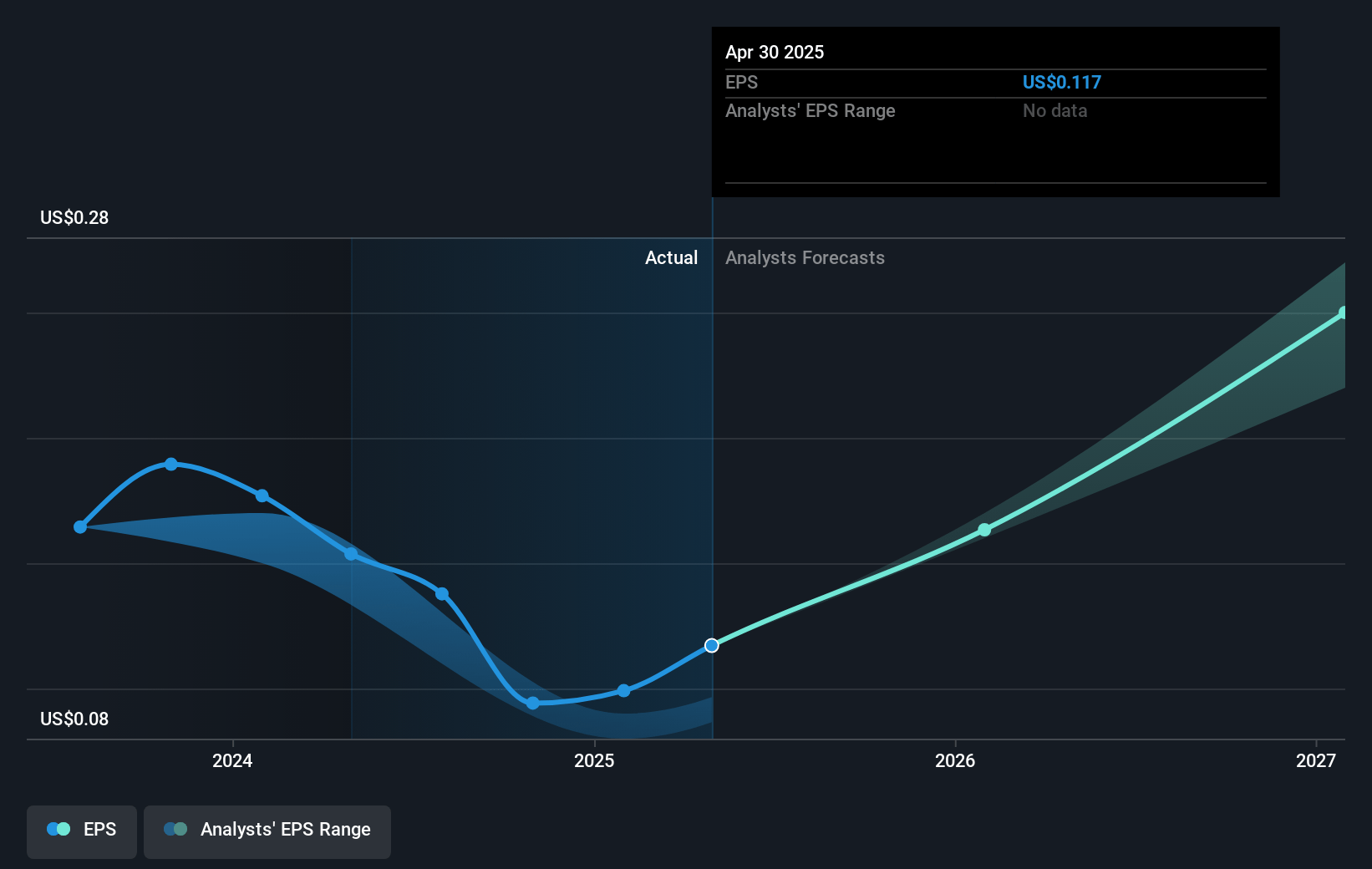

- Analysts expect earnings to reach $15.2 million (and earnings per share of $0.39) by about April 2028, up from $3.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.9x on those 2028 earnings, down from 64.1x today. This future PE is greater than the current PE for the US Food industry at 17.4x.

- Analysts expect the number of shares outstanding to grow by 0.89% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Mama's Creations Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Mama's Creations faces risks from commodity price fluctuations, particularly in chicken and beef, which could pressure gross margins if prices rise further. This may impact net margins and earnings if pricing adjustments are not timely or adequate.

- The company's significant reliance on a few major retailers like Walmart and Costco poses a risk, as any changes in these relationships or purchasing volumes could adversely affect revenue and profitability.

- Despite the strategic procurement contracts in place, over half of protein needs are still subject to spot market volatility, which could lead to increased costs and impact gross margins and earnings if commodity prices rise unexpectedly.

- The company's increased marketing and trade promotion expenses, while aimed at driving growth, might not yield expected returns if consumer demand does not materialize as anticipated, potentially affecting net income and overall financial performance.

- The ongoing expansion of facilities like East Rutherford, with potential exposure to tariffs and supply chain disruptions, could lead to increased costs or delays, impacting future cash flows and capital expenditures.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $11.0 for Mama's Creations based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $9.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $170.5 million, earnings will come to $15.2 million, and it would be trading on a PE ratio of 32.9x, assuming you use a discount rate of 6.2%.

- Given the current share price of $6.33, the analyst price target of $11.0 is 42.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.