Narratives are currently in beta

Key Takeaways

- Rising power demand and increased U.S. LNG exports could boost natural gas prices, positively impacting PHX Minerals' revenue.

- Proactive debt management and strong well pipeline may sustain long-term growth and enhance net margins.

- PHX Minerals faces challenges from a bearish natural gas market, external volatility, and production decreases, which could pressure future revenue and margins.

Catalysts

About PHX Minerals- Operates as a natural gas and oil mineral company in the United States.

- The anticipated increase in U.S. LNG export capacity, projected to double by 2028, could boost natural gas prices, which would positively impact PHX Minerals' revenue as they are primarily natural gas-focused.

- The increasing power demand driven by AI and data centers is expected to add approximately 7 Bcf per day of natural gas demand by 2030, potentially increasing natural gas prices and PHX's revenue.

- The substantial pipeline of wells in progress and continued drilling activity on PHX's mineral assets could lead to sustainable future growth in royalty volumes, positively impacting revenue and earnings.

- Ongoing efforts to manage debt and maintain a strong financial position, combined with proactive hedging strategies, could enhance net margins by minimizing exposure to adverse market conditions.

- Expected regulatory changes and favorable election outcomes could lead to increased U.S. GDP growth, benefiting demand for energy and potentially improving PHX Minerals' revenue prospects.

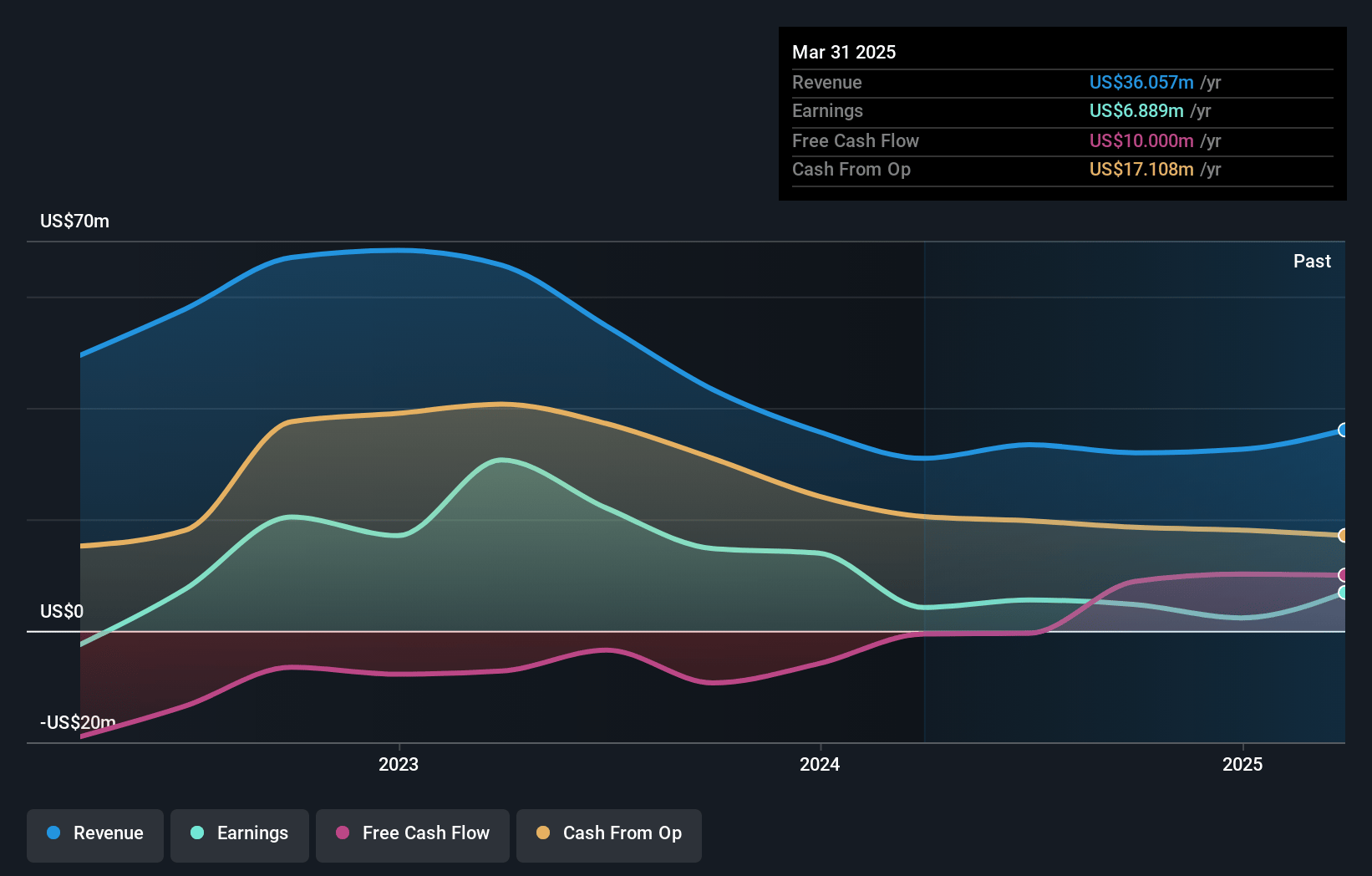

PHX Minerals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming PHX Minerals's revenue will grow by 32.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.8% today to 44.4% in 3 years time.

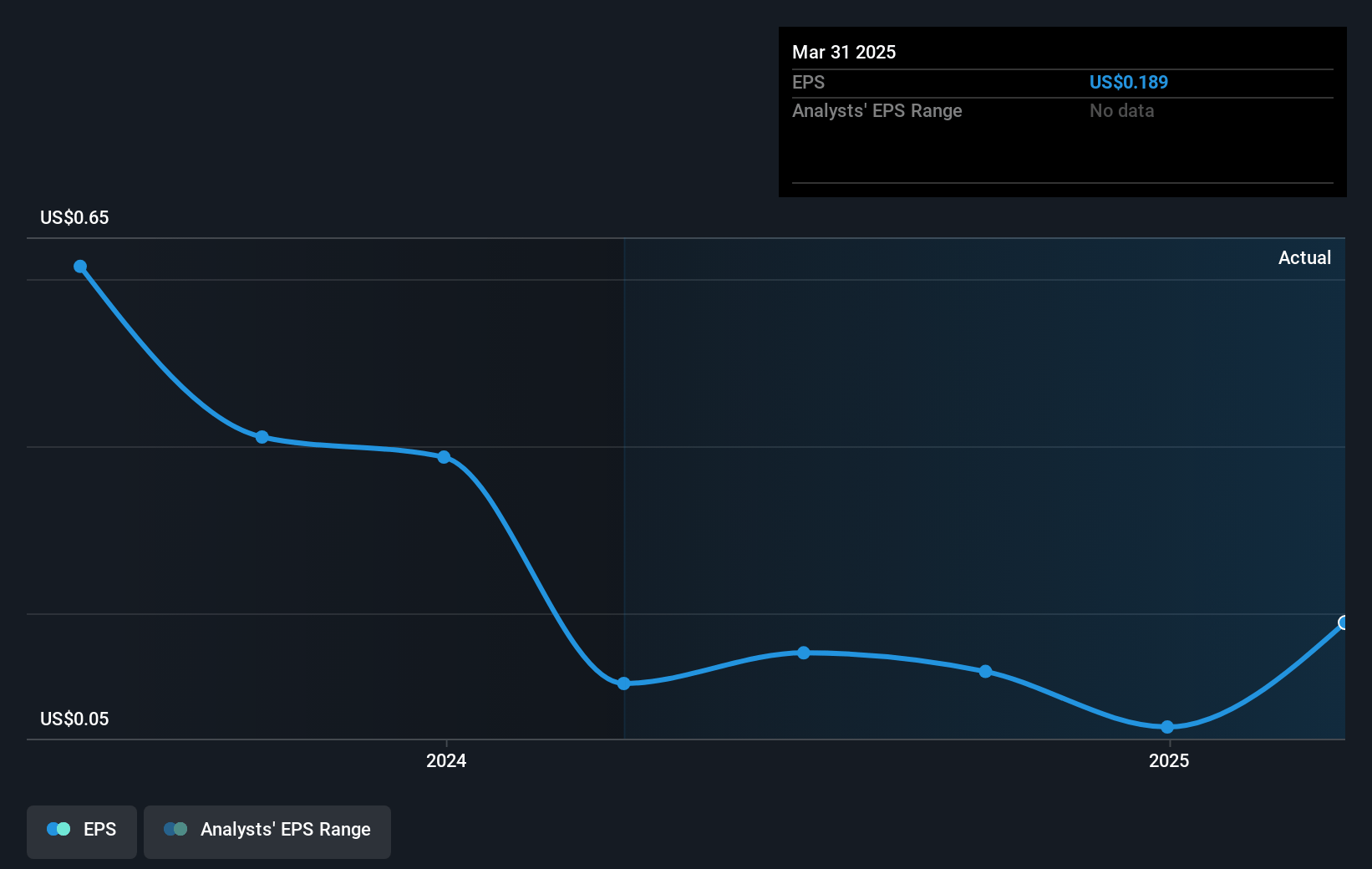

- Analysts expect earnings to reach $32.6 million (and earnings per share of $0.87) by about January 2028, up from $4.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 6.7x on those 2028 earnings, down from 31.0x today. This future PE is lower than the current PE for the US Oil and Gas industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

PHX Minerals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- PHX Minerals is heavily reliant on natural gas, which has experienced a bearish supply-demand macro environment, leading to lower realized prices and potentially impacting future cash flows and revenue.

- The company faces uncertainty from external factors such as weather and political changes that can affect natural gas demand and supply, posing risks to their earnings stability.

- The decrease in production volumes by 20% from the previous quarter and reliance on external operators for well development introduces volatility in revenue and net margins.

- The dampened market conditions in the Haynesville area and variable production activity pose challenges to meeting growth projections and future earnings expectations.

- PHX’s earnings are susceptible to fluctuations in commodity prices and the effectiveness of its hedging strategy, which may not always offer adequate protection against price drops, thus affecting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.75 for PHX Minerals based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $73.5 million, earnings will come to $32.6 million, and it would be trading on a PE ratio of 6.7x, assuming you use a discount rate of 7.4%.

- Given the current share price of $3.91, the analyst's price target of $4.75 is 17.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives