Key Takeaways

- Expanding international projects, disciplined capital allocation, and operational advances support strong long-term growth in revenue, cash flow, and shareholder value.

- Strategic positioning in key markets and industry trends enhances resilience, profitability, and the potential for accelerated earnings and net income.

- Industry-wide shift to renewables, aging assets, operational risks, price volatility, and rising ESG costs threaten Murphy Oil’s long-term profitability and revenue stability.

Catalysts

About Murphy Oil- Operates as an oil and gas exploration and production company in the United States, Canada, and internationally.

- Murphy’s rapidly advancing international project pipeline, highlighted by the Hai Su Vang oil discovery in Vietnam and upcoming exploration/appraisal wells in both Vietnam and Côte d'Ivoire, points to significant potential reserve additions and production growth through the late 2020s. These resource expansions would directly support higher long-term revenue and drive bullish projections for expanding free cash flow.

- The company is positioned to benefit from growing demand for natural gas and oil in Canada and Asia, where the Tupper Montney asset is increasingly protected from price volatility and is set to leverage future Canadian LNG exports. This aligns Murphy’s asset mix with rising global energy consumption, improving revenue resilience and supporting sustainable earnings growth.

- Ongoing investments and technological improvements in high-margin Gulf of Mexico and onshore US assets, including seismic reprocessing and well completion optimization, are enhancing capital efficiency and increasing lateral lengths and recoveries per well. These operational advancements reduce development costs and structurally boost net margins and returns on invested capital.

- Murphy’s disciplined capital allocation—marked by significant debt reduction, an expanding dividend, and a commitment to substantial share buybacks from free cash flow—will magnify future earnings per share. With nearly 80% of 2024’s adjusted free cash flow directed to share repurchases and a much lower debt burden, shareholder value is set to accelerate as cash generation rises.

- Global underinvestment in upstream oil and gas and continued strong industry consolidation should support higher commodity prices and improved capital efficiencies for nimble, mid-cap operators like Murphy. This industry dynamic will amplify profitability, especially as Murphy brings high-return, oil-weighted projects online internationally and in the Gulf of Mexico, leading to a step-change in net income and cash flow.

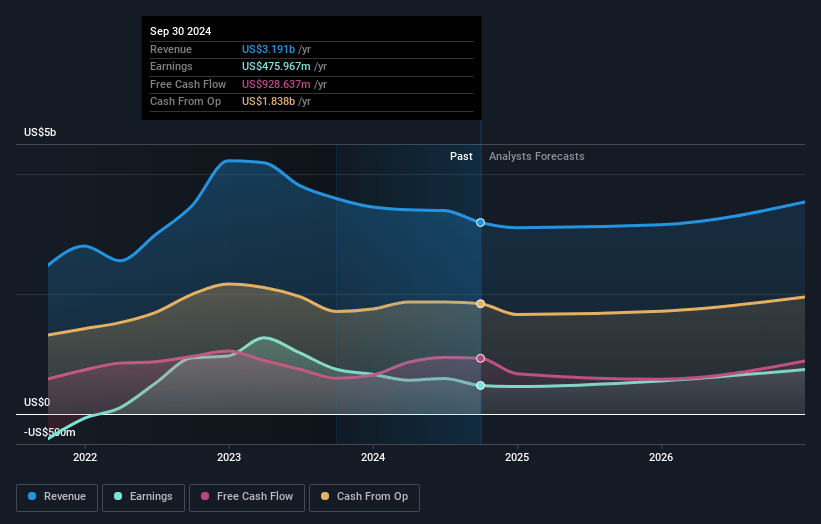

Murphy Oil Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Murphy Oil compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Murphy Oil's revenue will grow by 2.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 13.6% today to 19.3% in 3 years time.

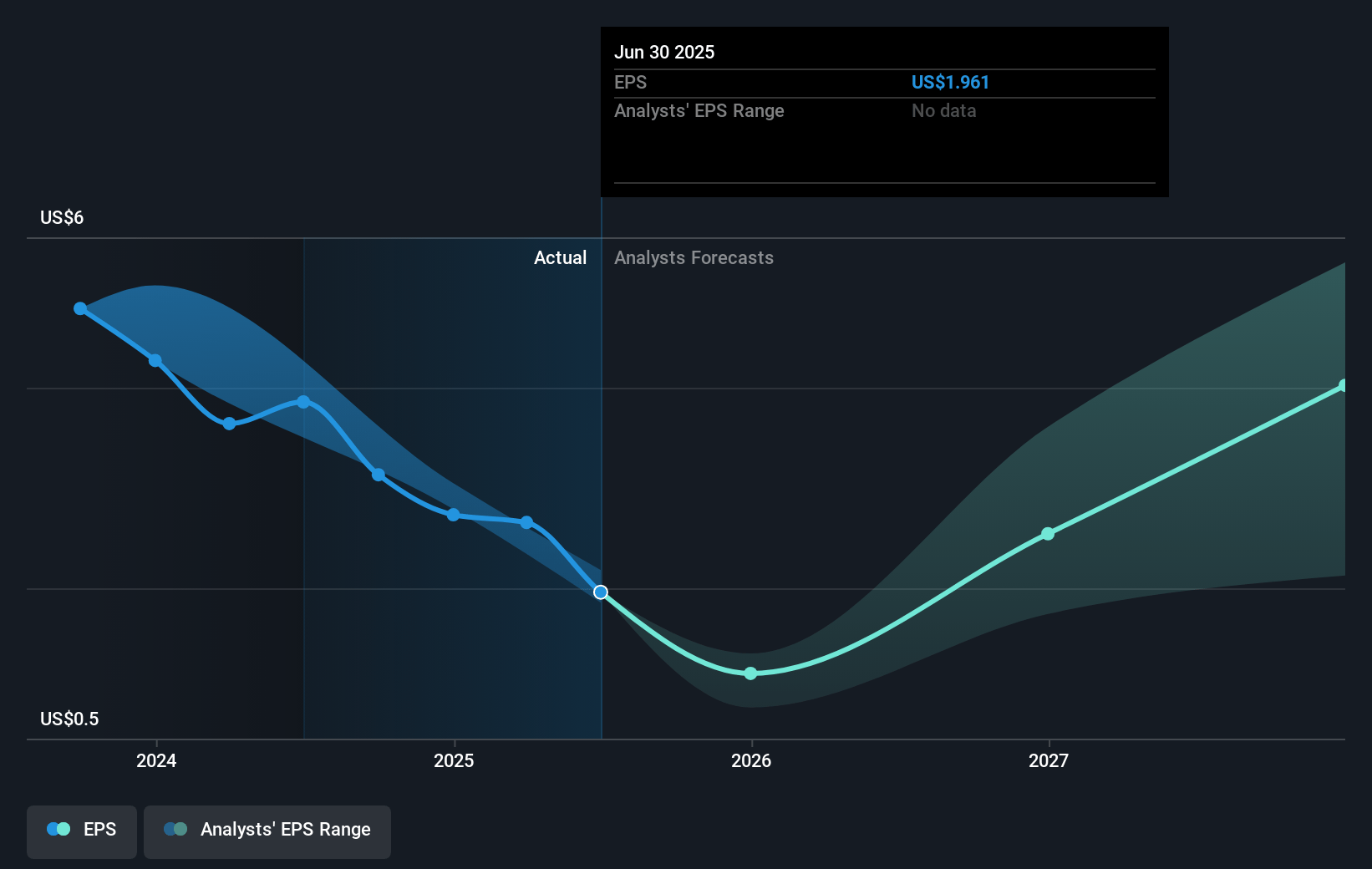

- The bullish analysts expect earnings to reach $627.0 million (and earnings per share of $6.69) by about April 2028, up from $410.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 10.7x on those 2028 earnings, up from 7.4x today. This future PE is lower than the current PE for the US Oil and Gas industry at 11.8x.

- Analysts expect the number of shares outstanding to decline by 4.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.77%, as per the Simply Wall St company report.

Murphy Oil Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Long-term global shift towards renewables and aggressive decarbonization targets are set to erode oil demand, making Murphy Oil’s core hydrocarbon business increasingly vulnerable to lower long-term revenues.

- Murphy Oil’s maturing asset base, including reliance on older fields in the Gulf of Mexico and Canada, necessitates ongoing high capital expenditure, with decline risks accentuated by recent mechanical issues and underperforming new well completions, ultimately pressuring production volumes and hurting revenue stability.

- Offshore and deepwater projects in Murphy’s pipeline carry higher capital intensity, potential for cost overruns, and delays, as evidenced by recent workover and rig delays; this creates risk for lower net margins and less predictable earnings.

- Elevated exposure to commodity price volatility, exacerbated by OPEC+ policy shifts, geopolitics, and increased North American supply, continues to challenge long-term earnings visibility and Murphy’s ability to plan capital allocation, potentially curtailing free cash flow available for shareholder returns.

- Heightening ESG standards, regulatory constraints (such as potential carbon taxes), and increasing compliance costs could drive up operating and financing costs, compressing profitability and exacerbating risks to sustained net income growth for Murphy Oil.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Murphy Oil is $43.06, which represents two standard deviations above the consensus price target of $29.5. This valuation is based on what can be assumed as the expectations of Murphy Oil's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $45.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $3.3 billion, earnings will come to $627.0 million, and it would be trading on a PE ratio of 10.7x, assuming you use a discount rate of 7.8%.

- Given the current share price of $21.22, the bullish analyst price target of $43.06 is 50.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NYSE:MUR. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.