Narratives are currently in beta

Key Takeaways

- MPLX is set to benefit from rising natural gas demand and expanded processing in major basins, supporting future revenue and earnings growth.

- New pipeline projects and operational improvements promise enhanced connectivity, reduced costs, and increased profitability across key assets.

- Reliance on macroeconomic factors and heavy capital spending could impact MPLX's revenues, earnings, and strategic growth due to external and internal uncertainties.

Catalysts

About MPLX- Owns and operates midstream energy infrastructure and logistics assets primarily in the United States.

- MPLX is positioned to capitalize on growing natural gas demand driven by grid electrification, onshoring, near-shoring, and data center development, which is expected to drive future revenue growth.

- Expansion of natural gas and NGL processing capacity in key basins (like the Marcellus, Utica, and Permian) will enhance throughput and operational scale, likely leading to higher earnings and cash flow over time.

- New pipeline projects like Blackcomb and Rio Bravo are set to connect supply from the Permian Basin to Gulf Coast markets and are projected to be serviceable by the second half of 2026, potentially boosting future revenue.

- MPLX is increasing its ownership and capacity in assets like the BANGL pipeline, which is expected to reach 250,000 barrels per day in the first quarter of 2025, supporting growth in NGL distribution revenue.

- Continuous operational improvements, such as energy efficiency initiatives at facilities like the Bluestone plant, are expected to lower operating costs, positively impacting net margins and overall profitability.

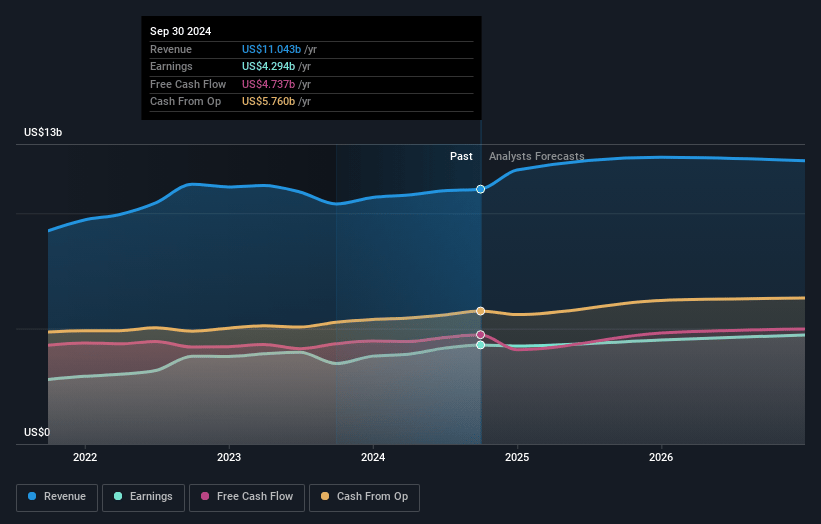

MPLX Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MPLX's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 38.9% today to 37.3% in 3 years time.

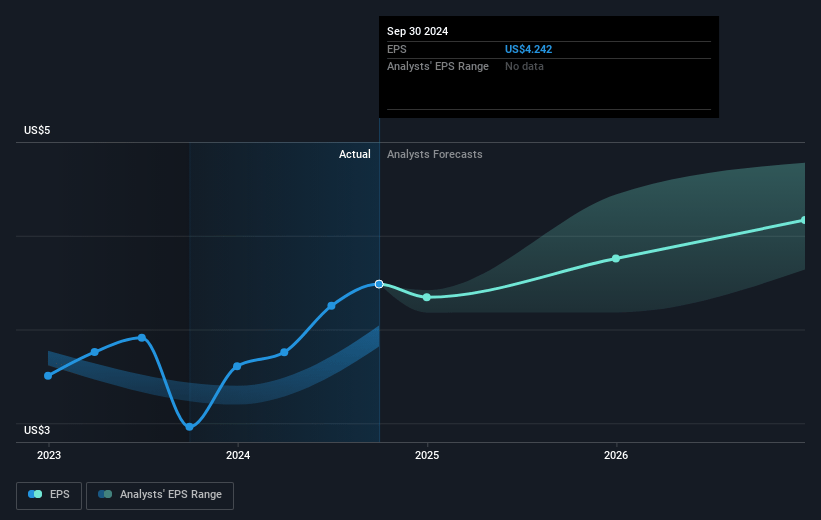

- Analysts expect earnings to reach $4.8 billion (and earnings per share of $4.74) by about January 2028, up from $4.3 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.8x on those 2028 earnings, up from 12.2x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 0.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.94%, as per the Simply Wall St company report.

MPLX Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on macroeconomic factors such as global demand for hydrocarbons and U.S. refining competitiveness introduces exposure to fluctuations in energy prices and geopolitical events that could impact revenues and net margins.

- The heavy capital spending, which is expected to reach over $1 billion for the year, poses a risk of overextension if projected growth does not materialize, potentially affecting net earnings and cash flow.

- The retirement of $1.65 billion in senior notes by February 2025 could strain MPLX’s cash reserves and liquidity position, impacting its ability to capitalize on future growth opportunities or deliver consistent earnings.

- Regulatory hurdles, such as the vacated FERC authorization for the Rio Bravo pipeline, could delay or derail infrastructure projects, impacting throughput volumes and, consequently, revenues.

- The dependency on the performance and strategic decisions of Marathon Petroleum Corporation may limit MPLX’s operational autonomy, influencing its ability to pursue optimal growth paths and affecting overall strategic earnings potential.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $51.94 for MPLX based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $58.0, and the most bearish reporting a price target of just $44.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $12.8 billion, earnings will come to $4.8 billion, and it would be trading on a PE ratio of 13.8x, assuming you use a discount rate of 7.9%.

- Given the current share price of $51.56, the analyst's price target of $51.94 is 0.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives