Key Takeaways

- Increased oil demand and favorable policy shifts in China and the U.S. are set to uplift DHT’s earnings and revenue.

- Strategic investments and low leverage bolster operational efficiency, financial stability, and potential net margin improvement.

- Geopolitical uncertainty, market volatility, and China's economic unpredictability pose significant risks to DHT Holdings' revenue and earnings stability.

Catalysts

About DHT Holdings- Through its subsidiaries, owns and operates crude oil tankers primarily in Monaco, Singapore, and Norway.

- DHT Holdings anticipates increased oil demand from China due to potential economic stimuli and policy changes, likely leading to stronger freight rates and increased revenues.

- Potential U.S. policy changes, such as tightening Iranian sanctions and pro-drilling policies, may increase demand for compliant VLCCs, positively impacting DHT’s earnings.

- Ongoing fleet investment, including newbuildings and exhaust gas cleaning systems, could enhance operational efficiency and net margins in the future.

- The company's strategy to build more fixed income through time charters aims to provide more predictable earnings, improving financial stability and EPS.

- DHT's low leverage and robust liquidity provide flexibility for strategic investments or opportunistic fleet sales, potentially enhancing net margins and shareholder returns through efficient capital allocation.

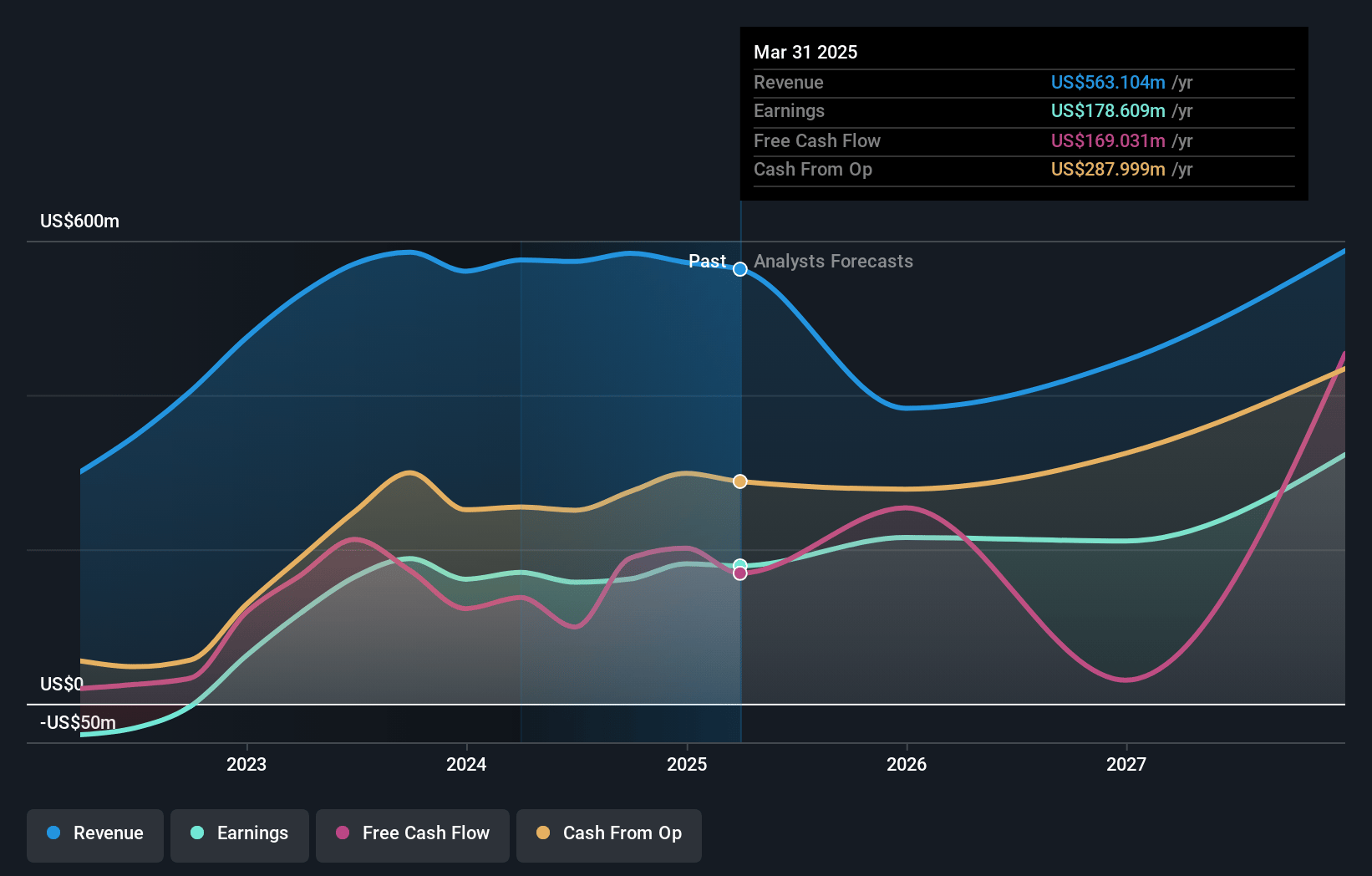

DHT Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DHT Holdings's revenue will grow by 3.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 27.7% today to 55.6% in 3 years time.

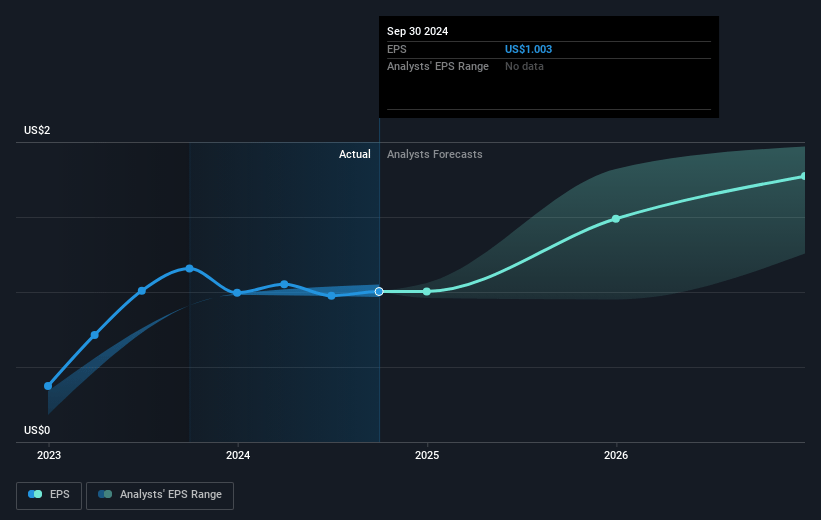

- Analysts expect earnings to reach $355.1 million (and earnings per share of $2.15) by about January 2028, up from $161.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $491 million in earnings, and the most bearish expecting $176 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.8x on those 2028 earnings, down from 11.0x today. This future PE is lower than the current PE for the US Oil and Gas industry at 11.9x.

- Analysts expect the number of shares outstanding to grow by 0.72% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.47%, as per the Simply Wall St company report.

DHT Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Limited activity in the secondhand sale and purchase market and uncertainty over ship values could reflect negatively on investor sentiment, potentially impacting revenue from asset sales and market valuation.

- Fluctuations in time charter rates due to market softness can lead to unpredictable earnings, as bid-ask spreads widen, which may affect net margins.

- The geopolitical uncertainty, notably regarding the Iran sanctions, could change oil flows and impact shipping demand unpredictably, thus potentially affecting revenue.

- China’s economy has not met growth projections, which, if not addressed successfully, could lead to lesser oil demand and fewer shipping opportunities, directly impacting revenue and earnings.

- The lack of transparency in China's crude oil inventory and the unpredictability of stimulus measures could lead to misjudgments in market demand, potentially affecting the company’s earnings projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.58 for DHT Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $16.0, and the most bearish reporting a price target of just $11.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $638.4 million, earnings will come to $355.1 million, and it would be trading on a PE ratio of 7.8x, assuming you use a discount rate of 7.5%.

- Given the current share price of $11.04, the analyst's price target of $13.58 is 18.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives