Narratives are currently in beta

Key Takeaways

- Merger integration challenges and production delays may hinder growth and impact future earnings and margins.

- Export market volatility and regulatory challenges could affect revenue growth, cash flow, and long-term coal demand.

- Strong operational efficiency and strategic international growth position CONSOL Energy for potential revenue and margin improvement, supported by synergies from a proposed merger.

Catalysts

About CONSOL Energy- Produces and sells bituminous coal in the United States and internationally.

- The proposed merger with Arch Resources and the planned formation of Core Natural Resources could face integration challenges or synergy realizations that may affect future growth. This could impact future earnings if the expected synergies are not realized or if integration costs are higher than anticipated.

- Production delays at the Itmann mining complex, due to equipment delivery issues and adverse geological conditions, could hinder future production growth and impact revenue and margins if these issues persist or worsen.

- Export markets, particularly in India and Asia, are facing pricing volatility due to prolonged monsoon seasons and lower pet coke prices. This uncertainty could affect future revenue growth and margins if CONSOL cannot secure favorable pricing contracts.

- Potential regulatory or environmental challenges related to the Global Water Treatment Trust Fund and other legacy liabilities may divert capital and impact future cash flow and margins if the liabilities increase or become more expensive to manage.

- The closure of coal plants and transition towards clean energy could create risks for long-term domestic coal demand, impacting future contracted positions and potentially leading to revenue fluctuations and margin compression.

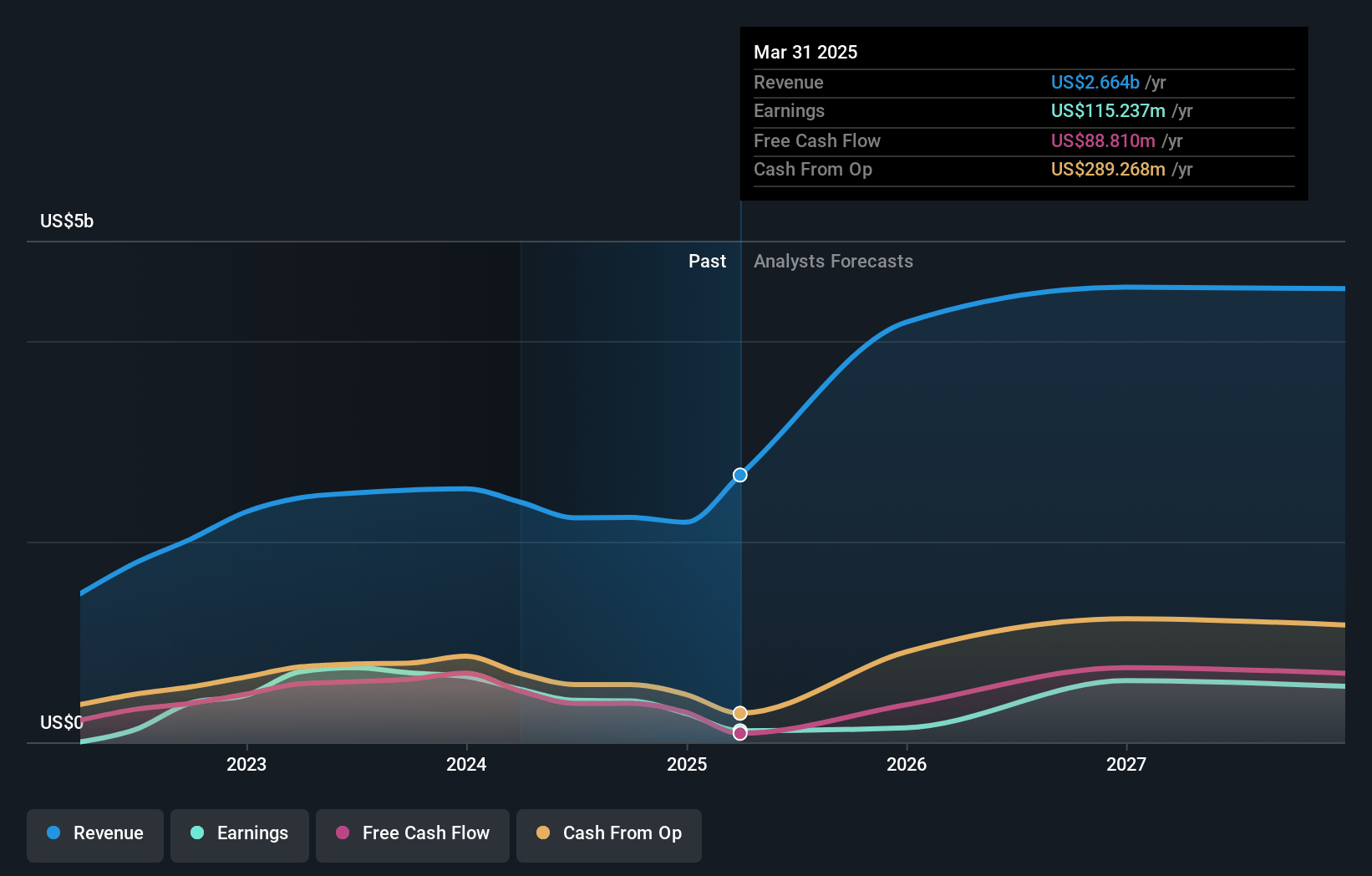

CONSOL Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CONSOL Energy's revenue will decrease by -1.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 18.4% today to 17.6% in 3 years time.

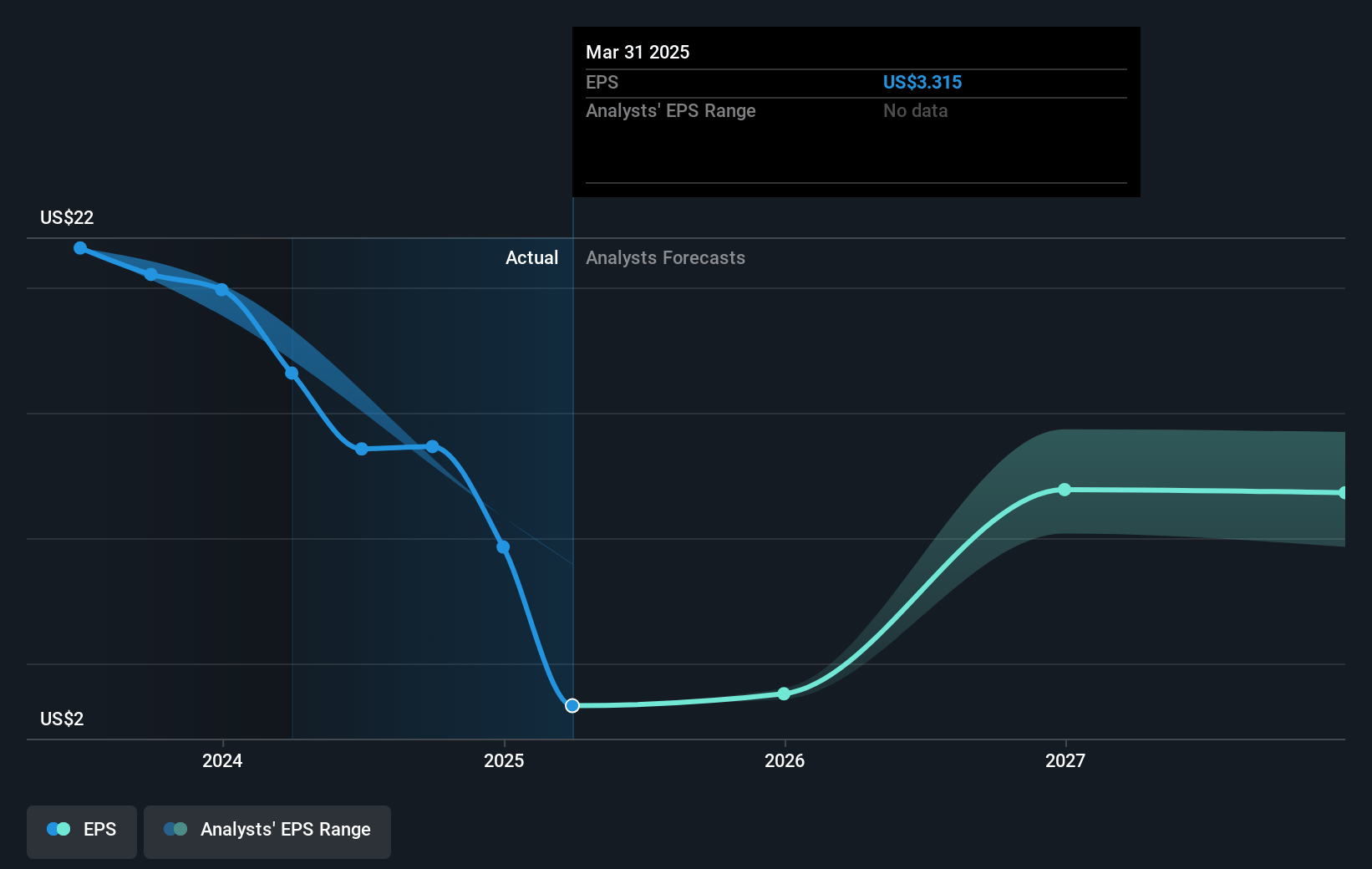

- Analysts expect earnings to reach $372.4 million (and earnings per share of $19.26) by about December 2027, down from $412.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.0x on those 2027 earnings, down from 8.3x today. This future PE is lower than the current PE for the US Oil and Gas industry at 11.1x.

- Analysts expect the number of shares outstanding to decline by 13.02% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.03%, as per the Simply Wall St company report.

CONSOL Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- CONSOL Energy reported its highest-ever third quarter sales and production tonnage, along with record low cash cost of coal sold per ton, indicating strong operational efficiency that could positively impact revenue and net margins.

- The company has experienced improved power demand growth, with domestic players delaying coal plant retirements, which suggests a steady demand outlook that could stabilize or increase future revenues.

- International demand is showing a promising outlook with robust coal sales into new markets like China, particularly the crossover metallurgical market, indicating potential revenue growth.

- The proposed merger with Arch Resources could create synergies and operational efficiencies, possibly improving earnings and margins by leveraging the strengths of both companies.

- Successful liability management initiatives, such as the establishment of a Global Water Treatment Trust Fund, reduce environmental liabilities and free up financial resources, potentially improving the company's financial health and net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $127.33 for CONSOL Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $142.0, and the most bearish reporting a price target of just $105.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $2.1 billion, earnings will come to $372.4 million, and it would be trading on a PE ratio of 8.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of $117.06, the analyst's price target of $127.33 is 8.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives