Narratives are currently in beta

Key Takeaways

- Significant infrastructure additions and strategic market access enhance revenue growth and stabilize earnings amid natural gas price volatility.

- Early leverage target achievement paves way for buybacks, boosting EPS and enhancing shareholder value.

- Revenue growth could be volatile due to deferral of completion activities, dependency on international demand, and potential changes in completion crew activity.

Catalysts

About Antero Midstream- Owns, operates, and develops midstream energy assets in the Appalachian Basin.

- The completion of the Torreys Peak compressor station in 2025, adding 160 million cubic feet a day of capacity, is expected to increase throughput and positively impact future revenue growth.

- Unconstrained access to international markets for propane exports allows Antero Resources to capture significant premiums, supporting free cash flow and potentially stabilizing earnings despite volatile natural gas prices.

- Accelerated capital expenditures due to favorable weather conditions in Q3 2024 suggest a significant decrease in capital spending in Q4 2024, which is expected to increase free cash flow and contribute to debt reduction, thereby impacting net margins and financial leverage.

- Ongoing free cash flow generation, as evidenced by the ability to internally finance both organic capital programs and acquisitions, indicates potential for future EBITDA and earnings growth, as well as additional capital returns to shareholders.

- Achieving the leverage target of less than 3x a year ahead of schedule allows for the potential initiation of buybacks, which could significantly improve EPS and reflect favorably in shareholder value.

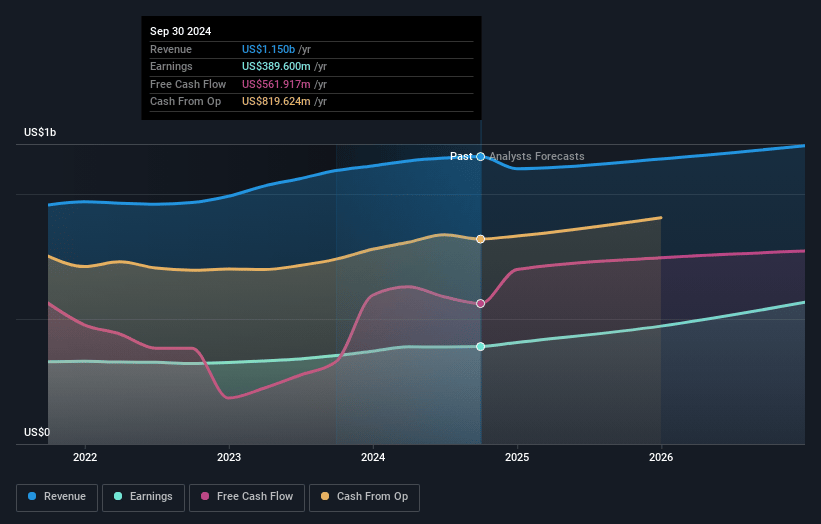

Antero Midstream Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Antero Midstream's revenue will decrease by 0.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 33.9% today to 47.3% in 3 years time.

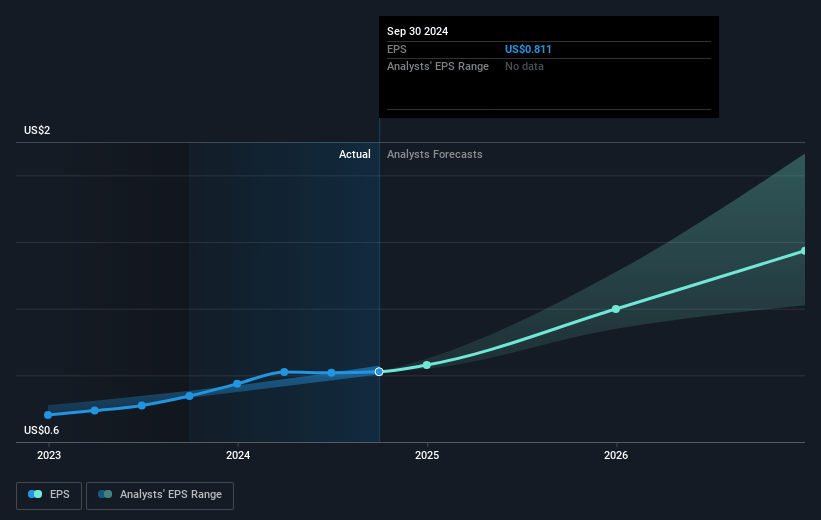

- Analysts expect earnings to reach $552.8 million (and earnings per share of $1.11) by about January 2028, up from $389.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $657.4 million in earnings, and the most bearish expecting $476.8 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, down from 19.5x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.9x.

- Analysts expect the number of shares outstanding to grow by 1.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.9%, as per the Simply Wall St company report.

Antero Midstream Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The deferral of completion activities and the dropping of a completion crew and rig could affect Antero Midstream's revenue growth expectations, contributing to volatility in its earnings.

- There is a dependency on strong international demand and export constraints along the Gulf Coast to sustain propane premiums, which could impact revenue if these conditions change.

- Uncertainty regarding the timing of proceeds from the Veolia case introduces unpredictability in financial planning and potential stress in managing leverage targets and debt reduction.

- Potential changes in completion crew activity, as articulated, could lead to fluctuations in water delivery volumes, directly impacting revenue and EBITDA.

- The considerable investment in capital expenditures and its alignment with scheduled financial outcomes may pressurize free cash flow if projected conditions do not meet expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.36 for Antero Midstream based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $552.8 million, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 7.9%.

- Given the current share price of $15.81, the analyst's price target of $15.36 is 2.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives