Narratives are currently in beta

Key Takeaways

- Strategic acquisitions and technology partnerships are anticipated to increase operational efficiency and digital capabilities, enhancing margins and improving decision-making processes.

- Shareholder-focused capital allocation, including buybacks and dividends, aims to boost earnings per share and deliver shareholder returns amidst margin expansion efforts.

- Market softening, regional delays, and pricing discipline constrain revenue growth, posing challenges to achieving significant top-line growth amidst competitive pressures.

Catalysts

About Weatherford International- An energy services company, provides equipment and services for the drilling, evaluation, completion, production, and intervention of oil, geothermal, and natural gas wells worldwide.

- Weatherford International has made advancements in new technology adoption and market penetration, securing noteworthy contracts, such as a 3-year procurement agreement with Aramco, which could drive future revenue growth by expanding their share in key markets.

- Integration of acquisitions like Datagration is expected to enhance digital capabilities and improve operational efficiencies, potentially boosting net margins by streamlining data integration and decision-making processes.

- Weatherford’s capital allocation strategy, including a $500 million share buyback and a new quarterly dividend of $0.25 per share, could support earnings per share (EPS) growth by reducing share count and providing shareholder returns.

- The company's maintained focus on price discipline and expanding margins, despite revenue headwinds, indicates potential for continued margin improvement, enhancing overall net margins and supporting long-term value creation.

- Leveraging differentiating technologies in mature field rejuvenation and production optimization offers opportunities for incremental revenue growth, even in a flat-to-moderate growth market, by improving production efficiency in existing operations.

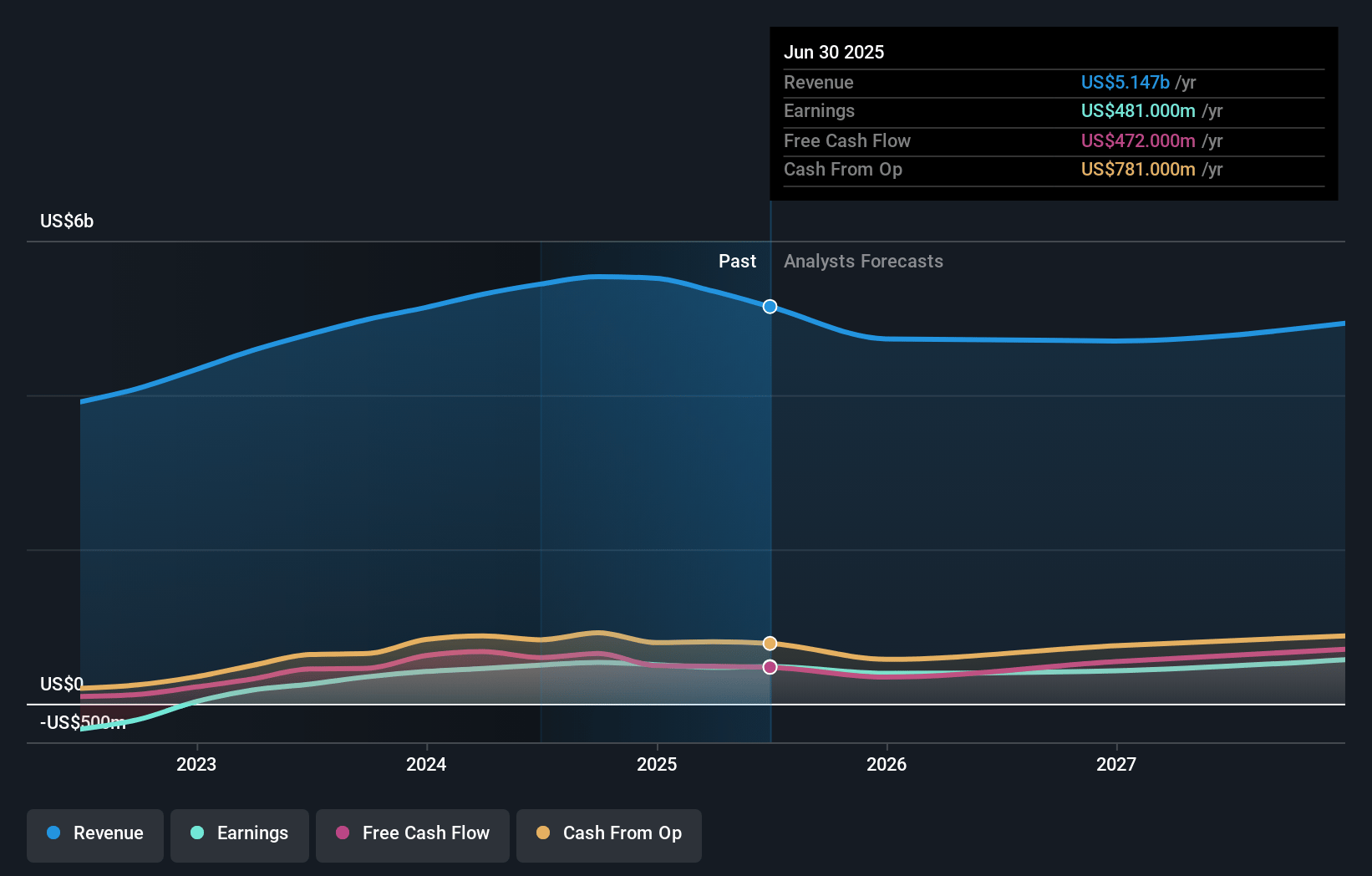

Weatherford International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Weatherford International's revenue will grow by 2.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.6% today to 10.5% in 3 years time.

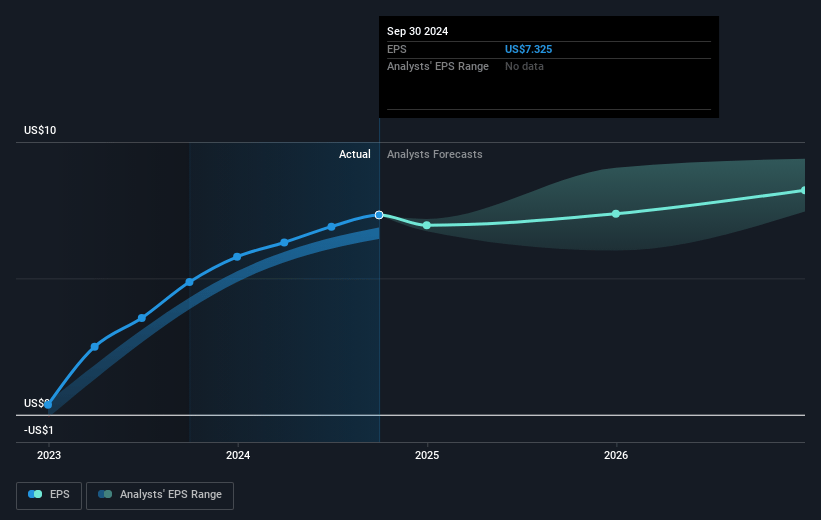

- Analysts expect earnings to reach $622.4 million (and earnings per share of $8.44) by about January 2028, up from $534.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $691 million in earnings, and the most bearish expecting $456 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.7x on those 2028 earnings, up from 9.0x today. This future PE is greater than the current PE for the US Energy Services industry at 14.6x.

- Analysts expect the number of shares outstanding to grow by 0.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.71%, as per the Simply Wall St company report.

Weatherford International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The gradual softening in activity, particularly in short-cycle oil projects and onshore programs, suggests potential constraints on future revenue growth as E&P operators take a more cautious approach.

- Delays and scheduling shifts in key regions like Latin America, the Middle East, and North Africa led to revenue shortfalls and could pose ongoing risks to meeting future earnings expectations.

- The slowing growth in broader international markets indicates potential challenges in maintaining high revenue growth, impacting the company's ability to sustain its current revenue trajectory.

- Despite opportunities to offset revenue shortfalls, a strong focus on pricing discipline may limit top-line growth, potentially constraining revenue and margins in a competitive environment.

- The new phase of the cycle characterized by low growth could result in sustained flat revenues, challenging the ability to achieve significant top-line growth and affecting overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $104.33 for Weatherford International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $84.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.9 billion, earnings will come to $622.4 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 8.7%.

- Given the current share price of $66.19, the analyst's price target of $104.33 is 36.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives