Narratives are currently in beta

Key Takeaways

- Strong performance in Marine Transportation and Sulfur Services segments contributes to stable cash flow and potential revenue and earnings growth.

- Decreased capital expenditures post-ELSA project and strategic buyout negotiations could enhance free cash flow, shareholder value, and EPS growth.

- Increased expenses and weak market conditions undermine net margins, future revenues, and cash flow, while pending transactions raise financial complexity and leverage concerns.

Catalysts

About Martin Midstream Partners- Provides terminalling, processing, storage, and packaging services for petroleum products and by-products primarily in the United States.

- The transportation segment, particularly the Marine Transportation business, has shown strong performance with adjusted EBITDA exceeding guidance due to higher-than-expected inland day rates. Continued tightness in the inland market suggests stable cash flow in the future, which could positively impact revenue.

- The Sulfur Services segment exceeded guidance in the third quarter due to a significant increase in sulfur volumes from Gulf Coast refinery customers. This increased production volume is expected to remain elevated, potentially boosting future revenue and earnings.

- The ELSA project, which Martin Midstream is involved in, will start generating reservation fees beginning October 1st, contributing to stable cash flow. Longer-term, as the project progresses to commercial sales, it has the potential to improve overall revenue and earnings.

- Capital expenditures are projected to decrease in 2025, following significant investment in the ELSA project in 2024. This reduction in capital spending could lead to improved free cash flow, positively impacting net margins and financial stability.

- Strategic negotiations through MRMC for a potential buyout offer are set to deliver an improved value per unit compared to the initial proposal, which could lead to favorable conditions for enhancing shareholder value and potential EPS growth post-transaction completion.

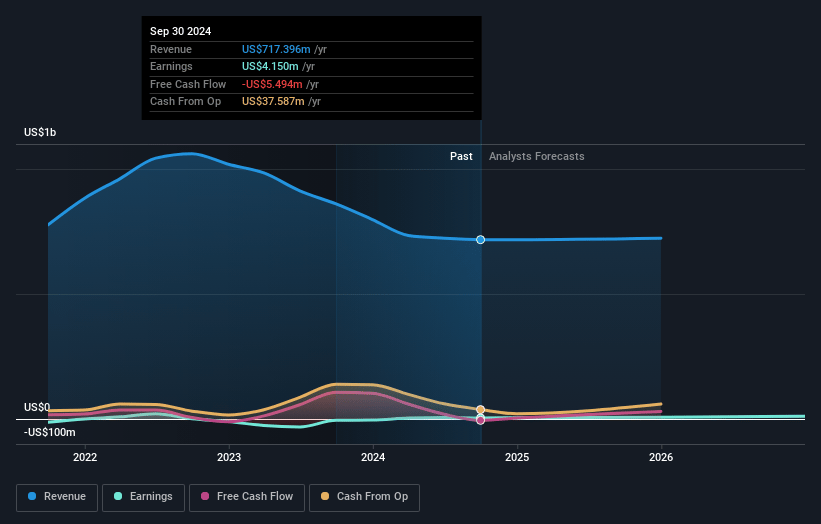

Martin Midstream Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Martin Midstream Partners's revenue will decrease by 0.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.6% today to 2.0% in 3 years time.

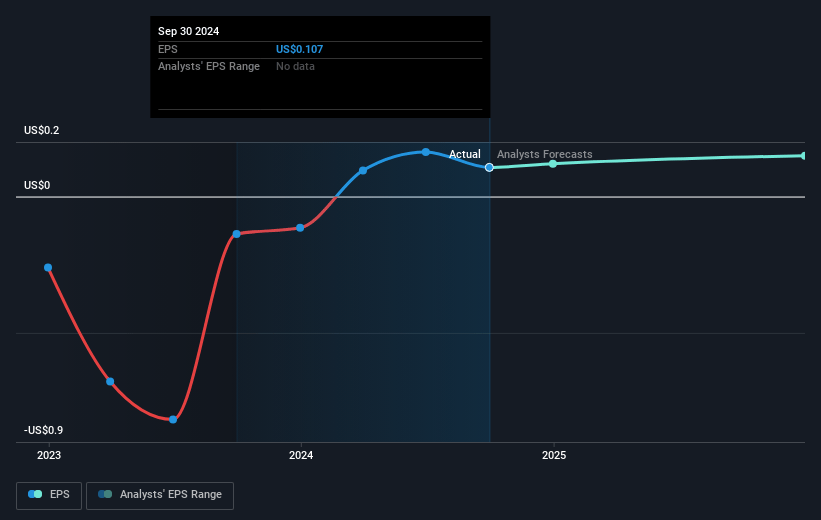

- Analysts expect earnings to reach $14.9 million (and earnings per share of $0.23) by about November 2027, up from $4.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.8x on those 2027 earnings, down from 37.2x today. This future PE is greater than the current PE for the US Oil and Gas industry at 10.4x.

- Analysts expect the number of shares outstanding to grow by 17.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.86%, as per the Simply Wall St company report.

Martin Midstream Partners Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The increased expenses related to long-term incentive plans tied to the fair market value of common units negatively impacted third quarter earnings guidance, indicating potential volatility in net margins and earnings.

- The weak performance in the Specialty Products segment, driven by lower demand due to a slowing U.S. economy, may result in reduced revenues and softer cash flow projections for the future.

- The disruption from Hurricane Milton, although relatively minor, entails additional capital expenditure ranging from $0.5 million to $1 million, which could potentially affect net margins and cash flow availability.

- The pending transaction with Martin Resource Management Corporation and the associated financing may introduce a debt burden or financial complexities that could impact future profitability or leverage ratios.

- Delays in the ELSA joint venture sales program are likely to defer expected revenue increases, impacting future earnings projections and potentially affecting long-term revenue growth expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.0 for Martin Midstream Partners based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $730.8 million, earnings will come to $14.9 million, and it would be trading on a PE ratio of 23.8x, assuming you use a discount rate of 10.9%.

- Given the current share price of $3.96, the analyst's price target of $4.0 is 1.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives