Last Update07 May 25Fair value Decreased 20%

Key Takeaways

- Reduction in capital expenditure in the Permian Basin may hinder revenue growth, affecting drilling and development plans.

- Delays in Suriname oil project revenue and flat production forecasts could challenge near-term earnings and growth potential.

- Portfolio enhancements and strategic acquisitions in key regions and strong cost reduction initiatives are expected to stabilize production and boost APA's financial performance and shareholder value.

Catalysts

About APA- An independent energy company, explores for, develops, and produces natural gas, crude oil, and natural gas liquids.

- APA's aggressive capital expenditure reduction in the Permian Basin may impact revenue growth due to a more limited drilling program, with development capital for 2025 expected to see over a 20% reduction.

- The company's dependence on improving cost structures to drive free cash flow could be overly optimistic, potentially affecting net margins if these savings do not materialize as expected given the targeted $350 million in savings by 2027.

- The delay in significant revenue contribution from the Suriname oil project, with first oil not expected until 2028, could mean that near-term earnings will rely heavily on existing assets and current commodity prices.

- Flat production projections in both the Permian and Egypt during 2025 to 2027, coupled with potential declines in Egypt, suggest future earnings may not grow as expected without new discoveries or price increases.

- Share buybacks, while providing short-term shareholder returns, may limit APA's ability to reduce debt further and strengthen the balance sheet, potentially impacting the long-term financial stability and earnings potential of the company.

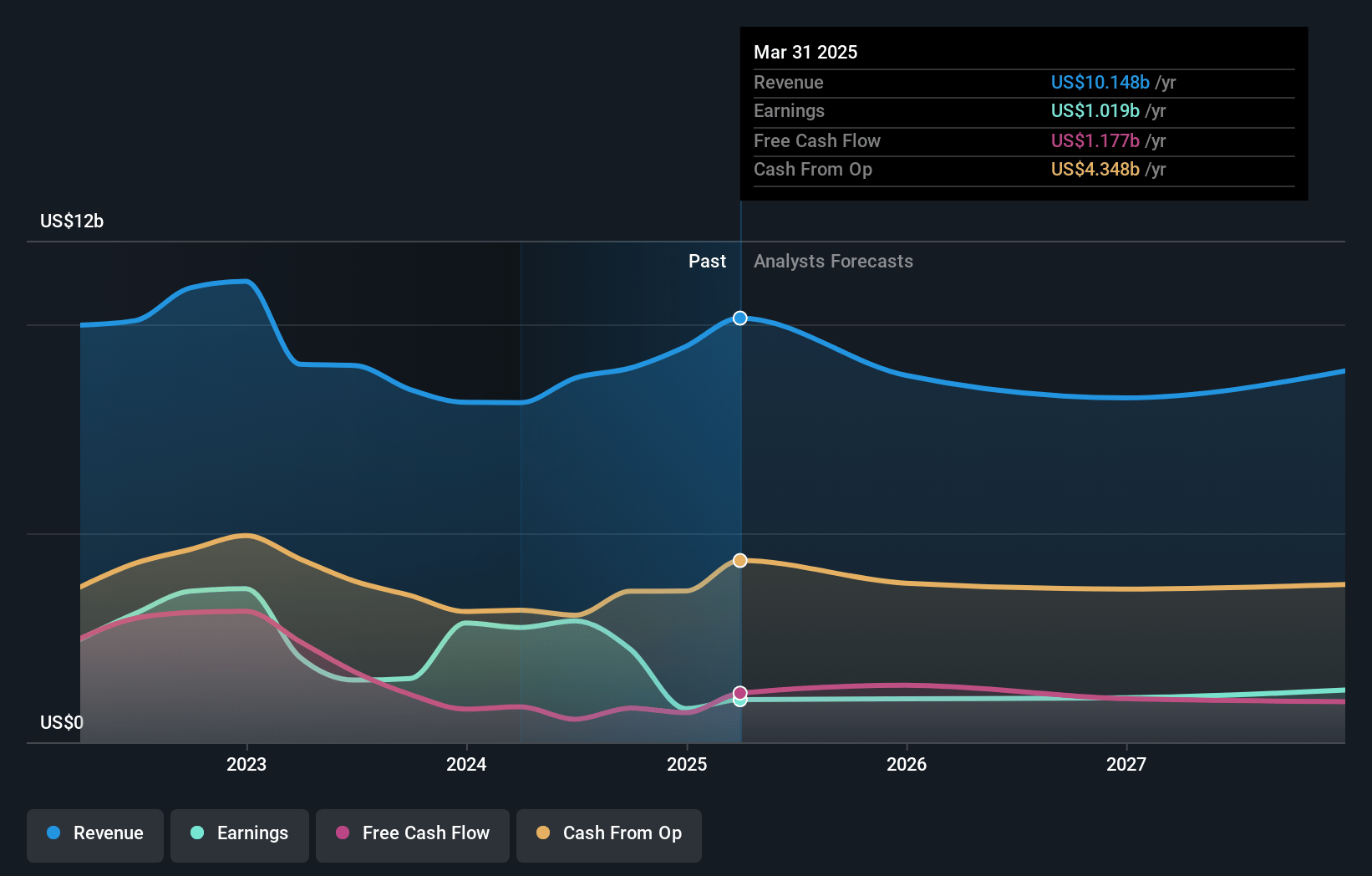

APA Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on APA compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming APA's revenue will decrease by 9.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 8.5% today to 8.2% in 3 years time.

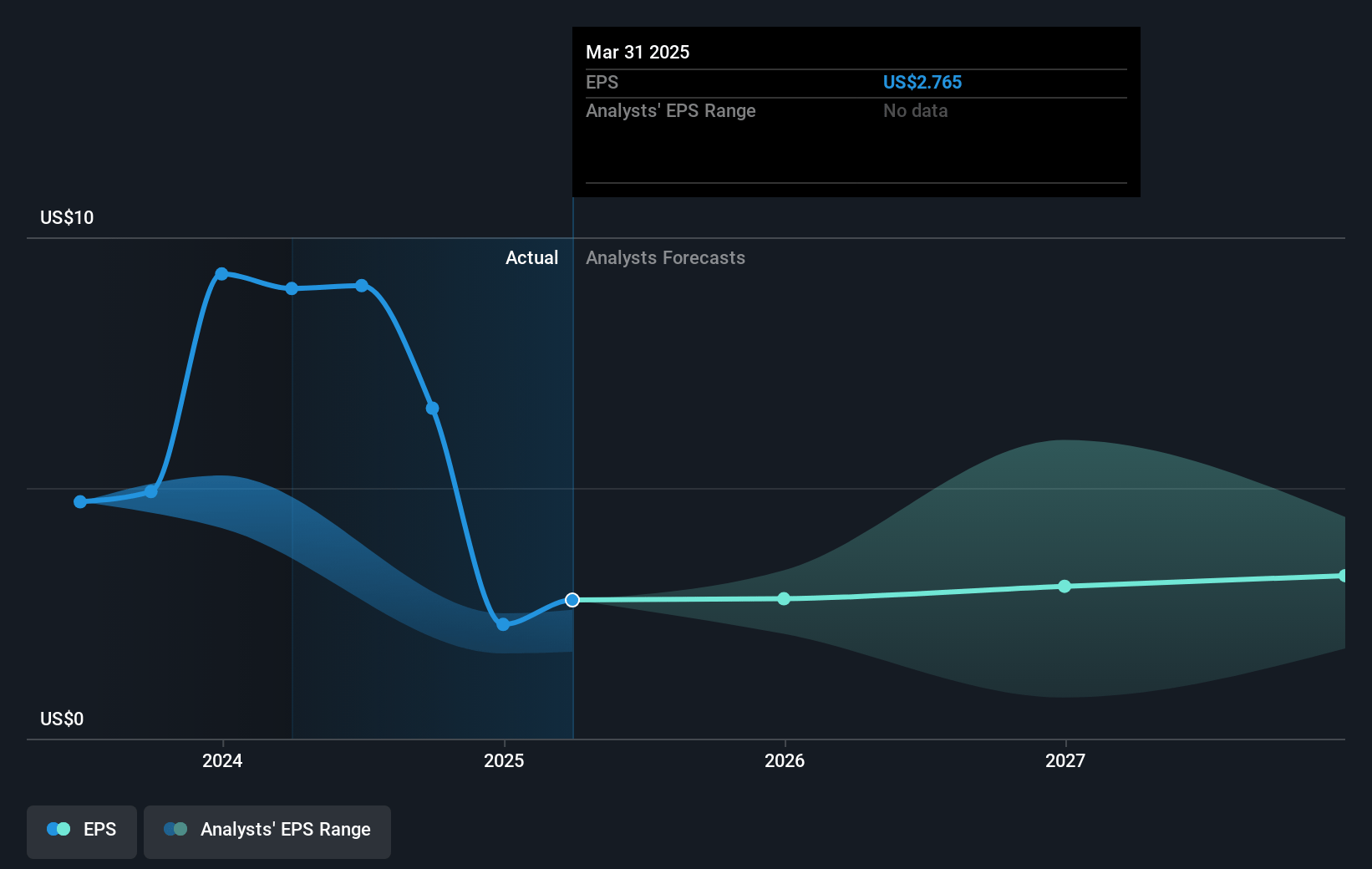

- The bearish analysts expect earnings to reach $587.1 million (and earnings per share of $1.65) by about May 2028, down from $804.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.4x on those 2028 earnings, up from 7.1x today. This future PE is lower than the current PE for the US Oil and Gas industry at 11.3x.

- Analysts expect the number of shares outstanding to decline by 1.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.66%, as per the Simply Wall St company report.

APA Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- APA Corporation's strategic enhancement of its portfolio, particularly in the Permian Basin and the Western Desert of Egypt, can lead to more predictable and steady production, thus potentially increasing revenues and stabilizing earnings.

- The acquisition of Callon and the sale of noncore assets have refined APA's position in the Permian Basin, likely leading to competitive returns and improved profit margins due to reduced well costs.

- Successful exploration initiatives, such as the final investment decision in Suriname for the GranMorgu project and promising developments in Egypt’s gas drilling program, could bolster future revenue streams by increasing APA's production profile.

- APA's cost reduction initiatives, targeting $350 million in annual savings by 2027, are expected to enhance free cash flow and profit margins, indicating stronger financial health.

- The company's commitment to a capital return framework, with significant share buybacks and dividends, underscores a focus on shareholder value, potentially supporting the stock price and making it attractive relative to underlying free cash flow growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for APA is $13.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of APA's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $36.0, and the most bearish reporting a price target of just $13.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $7.1 billion, earnings will come to $587.1 million, and it would be trading on a PE ratio of 9.4x, assuming you use a discount rate of 7.7%.

- Given the current share price of $15.73, the bearish analyst price target of $13.0 is 21.0% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives