Key Takeaways

- Strategic shift to high-quality loans and asset diversification is expected to enhance net margins and stabilize earnings.

- Exploiting market opportunities in maturing real estate debt and CRE CLO market return could expand portfolios and reduce financing costs.

- Uncertainty in borrower behavior, REO challenges, competition, and office loan exposure could negatively impact liquidity, margins, and long-term earnings stability.

Catalysts

About Franklin BSP Realty Trust- A real estate finance company, originates, acquires, and manages a portfolio of commercial real estate debt investments secured by properties located in the United States and internationally.

- The company has shifted to originating higher-quality loans with low loan-to-value (LTV) ratios post-interest rate hikes, which are expected to be more profitable and less risky. This emphasis on high-quality borrowers and robust loan metrics is likely to positively impact net margins and earnings.

- FBRT is actively utilizing available liquidity and proceeds from resolving non-performing loans to invest in new assets, leading to potential increases in distributable earnings by $0.25 to $0.30 per share annually. This deployment of capital should enhance revenue and improve net margins by optimizing the asset mix.

- The strategy to reduce and liquidate its REO portfolio with a focus on multifamily assets indicates a potential for improved net margins and stabilized earnings. Successful liquidation at or above debt basis minimizes losses and recycles capital into high-performing assets.

- There is a significant opportunity in originating new loans due to a supply constraint from traditional credit providers amid $3.4 trillion of maturing commercial real estate debt over the next three years, which could drive revenue and expand the loan portfolio.

- The planned return to the CRE CLO market in 2025 is anticipated to secure attractive financing rates, enhancing leverage efficiency, reducing costs of funds, and potentially boosting earnings through lower financing costs.

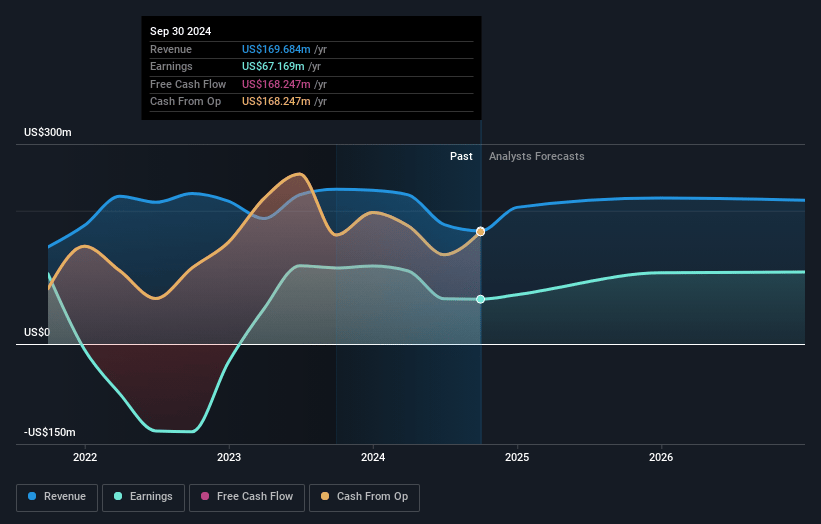

Franklin BSP Realty Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Franklin BSP Realty Trust's revenue will grow by 12.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 38.4% today to 58.7% in 3 years time.

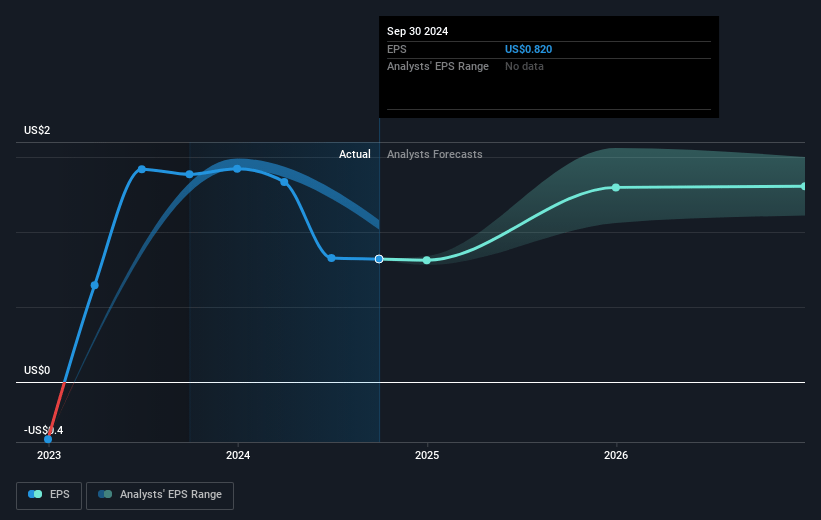

- Analysts expect earnings to reach $144.8 million (and earnings per share of $1.73) by about March 2028, up from $67.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.2x on those 2028 earnings, down from 16.3x today. This future PE is lower than the current PE for the US Mortgage REITs industry at 12.4x.

- Analysts expect the number of shares outstanding to grow by 0.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.32%, as per the Simply Wall St company report.

Franklin BSP Realty Trust Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The uncertainty of borrower behavior poses a challenge in managing cash flow and could impact the ability to predict and manage repayments, affecting liquidity and earnings.

- Significant REO (real estate owned) and non-accrual loans are forecast to impact earnings in the short term, causing potential earnings volatility and pressure on net margins.

- Although there is a high volume of commercial real estate loan maturities, excessive competition could compress loan spreads, potentially reducing net margins on new originations.

- Continued exposure to office loans, particularly problematic legacy loans, can lead to asset write-downs and liquidity constraints, impacting long-term asset valuations and earnings stability.

- Elevated other expenses due to preparing properties for sale may offset potential earnings from asset sales, impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.333 for Franklin BSP Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $246.8 million, earnings will come to $144.8 million, and it would be trading on a PE ratio of 11.2x, assuming you use a discount rate of 8.3%.

- Given the current share price of $13.3, the analyst price target of $15.33 is 13.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives