Key Takeaways

- Expansion of loan portfolios and use of securitizations are key to driving revenue growth and enhancing earnings through attractive pricing and reduced funding costs.

- Refinancing higher-cost debt to lower-cost alternatives is expected to improve earnings and net margins by lowering interest expenses.

- Rising interest rates and credit issues in non-QM loans and consumer credit could hurt Ellington Financial's earnings and revenue streams.

Catalysts

About Ellington Financial- Through its subsidiary, Ellington Financial Operating Partnership LLC, acquires and manages mortgage-related, consumer-related, corporate-related, and other financial assets in the United States.

- Ellington Financial's expansion of its loan portfolios and sourcing channels, particularly through proprietary loan origination businesses and joint venture investments, is expected to drive future revenue growth by increasing high-quality loan acquisition at attractive pricing.

- The strategic use of securitizations, such as non-QM and reverse mortgage deals, is likely to enhance earnings by securing non-recourse, non-mark-to-market long-term financing, reducing funding costs, and retaining high-yielding tranches.

- Improvement in warehouse financing terms and the addition of financing counterparties provide ample borrowing capacity, potentially lowering borrowing costs and positively impacting net interest margin.

- Refinancing of higher-cost debt and preferred stock, replaced with lower-cost debt, should be immediately accretive to earnings and improve net margins by reducing interest expenses.

- Continued strong performance and growth in the Longbridge reverse mortgage segment, particularly proprietary products, are expected to contribute to revenue and earnings growth, supported by large market share and strong origination capabilities.

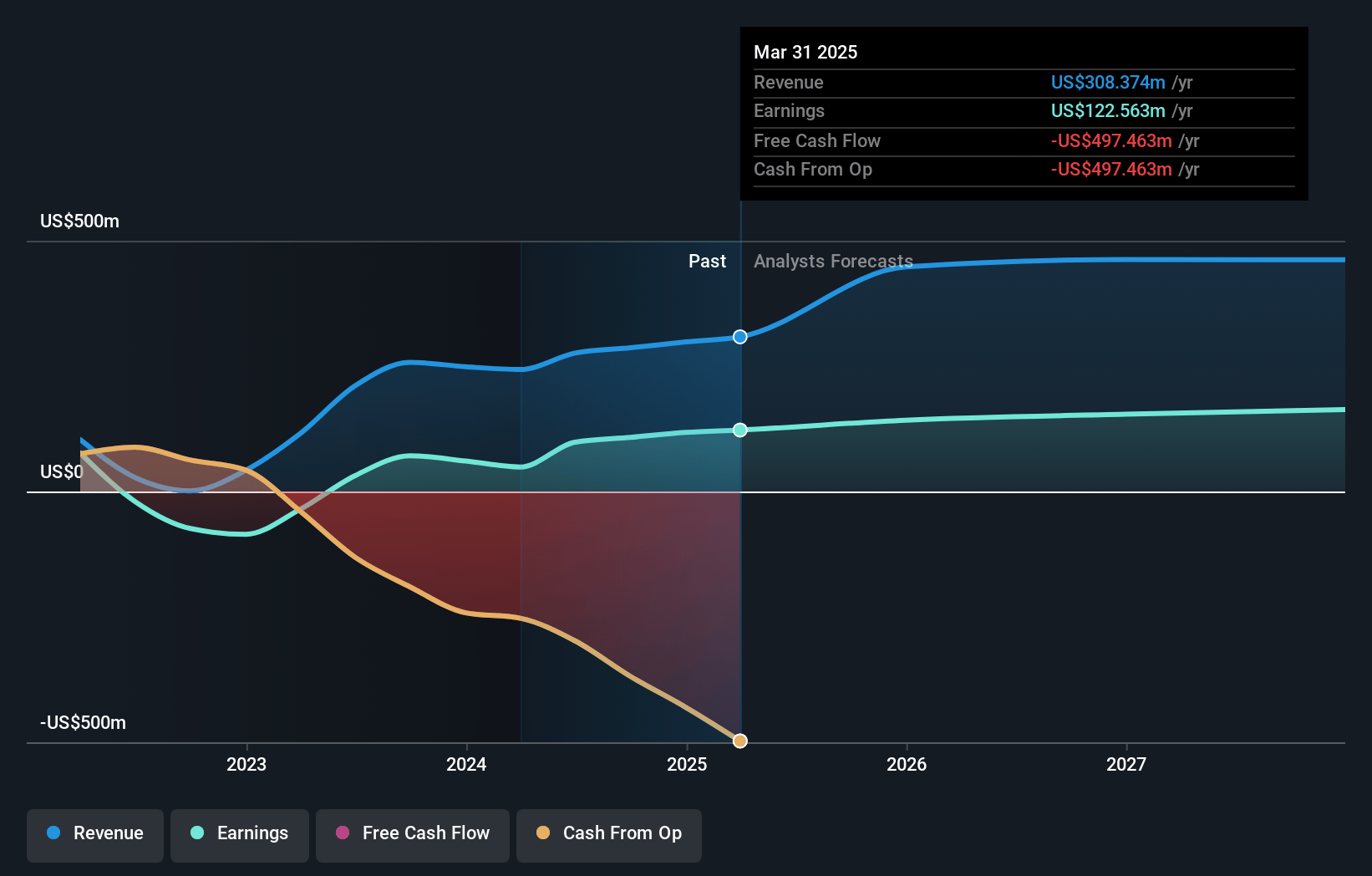

Ellington Financial Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ellington Financial's revenue will grow by 15.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 38.9% today to 35.0% in 3 years time.

- Analysts expect earnings to reach $161.5 million (and earnings per share of $1.7) by about May 2028, up from $117.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.9x on those 2028 earnings, up from 10.6x today. This future PE is lower than the current PE for the US Mortgage REITs industry at 13.4x.

- Analysts expect the number of shares outstanding to grow by 6.63% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.69%, as per the Simply Wall St company report.

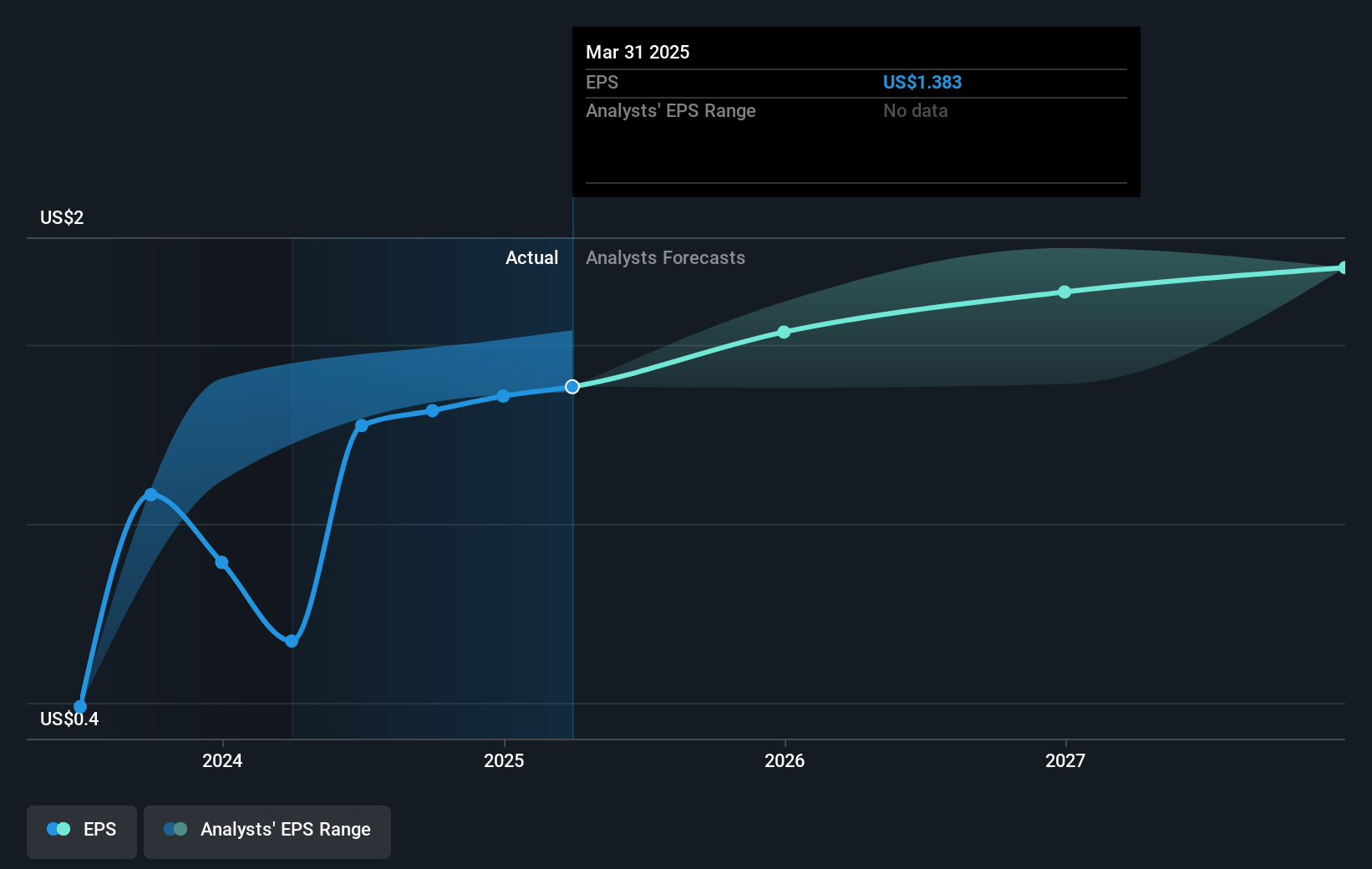

Ellington Financial Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising interest rates and intra-quarter volatility, particularly around the presidential election, caused underperformance of Agency RMBS relative to hedging instruments, which negatively impacted net margins.

- Negative operating income from REO workouts and declining credit performance in some loan portfolios, such as non-QM loans, could adversely affect net earnings.

- An uptick in residential loan delinquencies, especially in the non-QM portfolio due to higher mortgage rates and larger loan sizes, poses a risk to future revenue streams.

- Delays and higher costs in resolving commercial mortgage loans in workout phases could drag earnings and limit reinvestment of capital into growing businesses.

- Weakening consumer credit, which is pervasive across the market, could further increase delinquencies and impact net income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $14.071 for Ellington Financial based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $11.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $462.0 million, earnings will come to $161.5 million, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 8.7%.

- Given the current share price of $13.23, the analyst price target of $14.07 is 6.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.