Key Takeaways

- Expansion into sustainability-focused sectors and rural infrastructure is broadening business opportunities and supporting ongoing revenue and earnings growth.

- Investments in technology and legislative support are strengthening risk management and loan growth, contributing to improved profitability and market positioning.

- Rising regulatory, credit, and operating risks threaten revenue growth, profitability, and asset quality, while dependency on government policy leaves business practices vulnerable to external shifts.

Catalysts

About Federal Agricultural Mortgage- Provides a secondary market for various loans made to borrowers in the United States.

- Expansion into renewable energy, broadband, and infrastructure finance is driving significant new business volume and higher spreads, positioning Farmer Mac to benefit from increasing demand for financing related to sustainability and rural connectivity initiatives, which should support revenue and earnings growth going forward.

- Accelerating capital needs in agriculture and rural infrastructure, driven by farm consolidation and increased mechanization, are creating a larger addressable market for Farmer Mac's core and new product offerings, underpinning long-term loan growth and greater net interest income.

- Ongoing advancements in data analytics and underwriting technology investments are improving credit risk management and operating efficiency, which-combined with proactive expense management-should support stable or expanding net margins over time.

- Federal legislative support, such as the passage of HR1 with provisions supporting tax benefits for agricultural lending and renewable energy projects, is enhancing Farmer Mac's revenue opportunities and reducing long-term credit risks, thus potentially improving earnings stability.

- The company continues to maintain access to low-cost funding via its government-sponsored enterprise status, which gives it a structural advantage in offering competitively priced loans, supporting loan growth and profitability, especially as agricultural lending needs increase due to population and food demand trends.

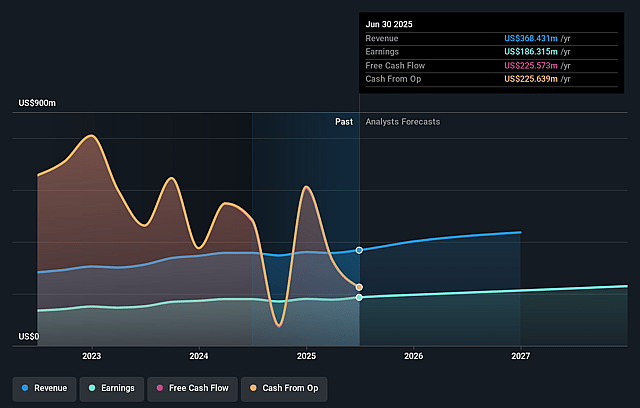

Federal Agricultural Mortgage Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Federal Agricultural Mortgage's revenue will grow by 11.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 50.6% today to 46.5% in 3 years time.

- Analysts expect earnings to reach $239.2 million (and earnings per share of $20.92) by about August 2028, up from $186.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.7x on those 2028 earnings, up from 10.9x today. This future PE is lower than the current PE for the US Diversified Financial industry at 16.0x.

- Analysts expect the number of shares outstanding to grow by 0.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.32%, as per the Simply Wall St company report.

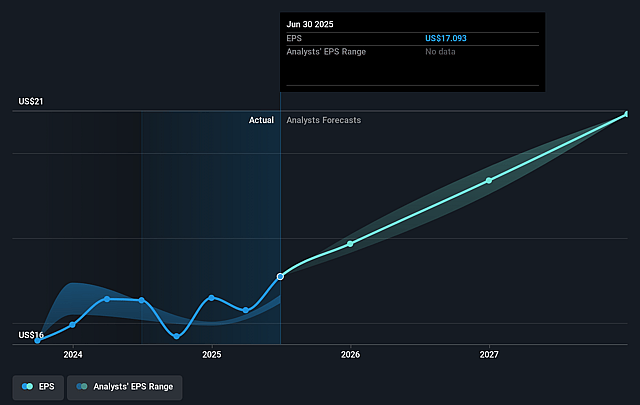

Federal Agricultural Mortgage Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The phaseout of renewable energy tax credits and increased regulatory and permitting uncertainty for renewable projects-particularly after recent executive orders-may reduce transaction volume and fee income in Farmer Mac's growing renewable energy segment, negatively impacting revenue diversification and future earnings growth.

- Accelerating credit losses and increased CECL-derived allowances in new segments like broadband and infrastructure finance-highlighted by recent downgrades and charge-offs-suggest portfolio risk is rising, which could drive up provisions for loan losses and reduce net margins and profitability over time.

- Persistent volatility from trade policy shifts and new tariffs, alongside unpredictable government relief and subsidy programs, introduces uncertainty for core Farm & Ranch borrower health, potentially reducing loan demand and increasing default risks, which could impair both revenue and asset quality.

- Rising operating expenses from technology investments, higher headcount, and transaction-related legal fees, if not offset by commensurate revenue growth, may erode Farmer Mac's efficiency ratio and compress net margins, limiting long-term earnings expansion.

- Dependence on favorable government-sponsored enterprise (GSE) status and potential changes to policies or capital requirements (as seen with HR1 and ongoing regulatory adjustments) expose Farmer Mac to political and regulatory risk, which could increase compliance costs or hinder business practices, pressuring both revenue generation and net income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $226.0 for Federal Agricultural Mortgage based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $514.9 million, earnings will come to $239.2 million, and it would be trading on a PE ratio of 14.7x, assuming you use a discount rate of 12.3%.

- Given the current share price of $185.22, the analyst price target of $226.0 is 18.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.