Key Takeaways

- Strategic collaborations with Visa and Mastercard for digital payment solutions could enhance relationships with financial institutions and boost payment processing revenue.

- Expanding digital and cloud solutions, coupled with high customer retention, positions Jack Henry for significant growth in revenue and profitability.

- Industry consolidation and hardware revenue decline pose future revenue challenges, while reliance on nonrecurring and compressed margins could affect earnings predictability and growth.

Catalysts

About Jack Henry & Associates- A financial technology company that connects people and financial institutions through technology solutions and payment processing services that reduce the barriers to financial health.

- Jack Henry's strategic collaboration with Visa and Mastercard to offer real-time digital payment solutions could strengthen relationships with banks and credit unions, potentially increasing future deposits and payment processing revenue.

- The continued expansion of the Banno digital platform, particularly its business offerings, demonstrates strong growth potential, with a 20% increase in registered users. This growth could drive future revenue and profitability gains as more clients adopt the platform.

- Jack Henry's focus on cloud solutions, with private cloud offerings growing at double-digit rates and further advancements in its public cloud strategy, positions the company to benefit from increased technology spending by banks and credit unions, potentially boosting future earnings.

- The aggressive push for newer products like the Financial Crimes Defender and Faster Payment Fraud module highlights Jack Henry's investment in high-demand areas, which could lead to higher future growth rates in revenues associated with fraud prevention and payment security.

- A high renewal success rate, especially among larger banks, indicates significant customer retention and the potential for upselling additional services. This could positively impact future revenue stability and expand net margins through reduced churn.

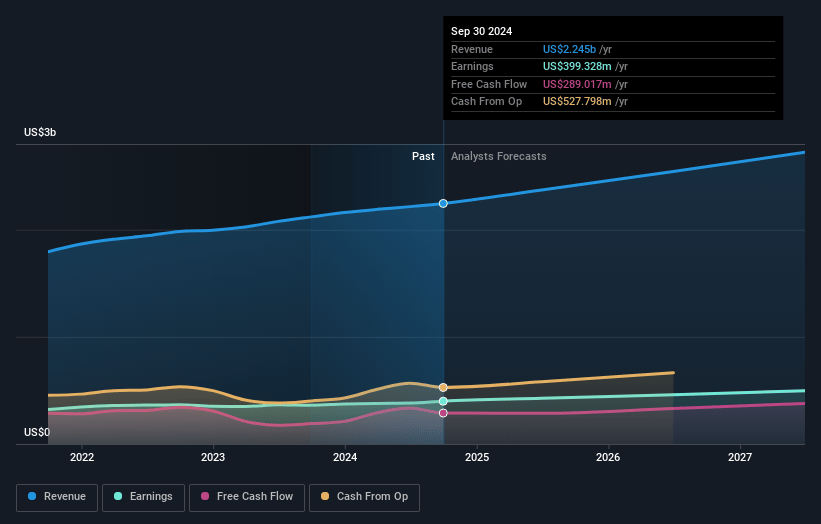

Jack Henry & Associates Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Jack Henry & Associates's revenue will grow by 7.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 17.8% today to 18.8% in 3 years time.

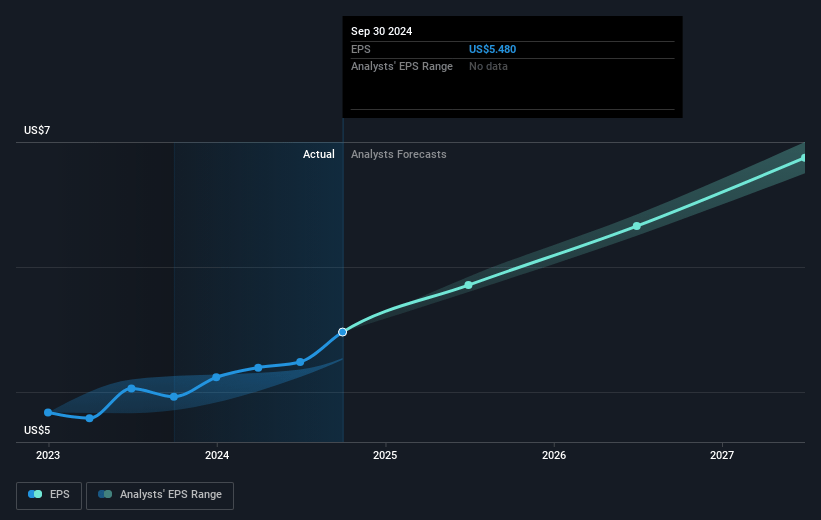

- Analysts expect earnings to reach $526.9 million (and earnings per share of $7.36) by about March 2028, up from $405.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 31.8x on those 2028 earnings, which is the same as it is today today. This future PE is greater than the current PE for the US Diversified Financial industry at 15.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.96%, as per the Simply Wall St company report.

Jack Henry & Associates Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company noted increased industry consolidation, which may have minimal impact in fiscal 2025 but potential for greater impact in fiscal 2026, indicating possible future revenue challenges.

- Hardware revenue was down significantly, described as headwinds for services and support revenue, which may affect overall revenue if not offset by other growth areas.

- A reliance on nonrecurring hardware revenue with low visibility could affect the predictability of earnings and revenue growth.

- References to price compression during renewals highlight potential downward pressure on margins if not adequately countered with additional product sales.

- While there is confidence in back-half revenue acceleration, the dependence on timing and successful completion of installations and product launches could pose execution risks impacting revenue growth prospects.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $190.048 for Jack Henry & Associates based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $212.0, and the most bearish reporting a price target of just $155.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.8 billion, earnings will come to $526.9 million, and it would be trading on a PE ratio of 31.8x, assuming you use a discount rate of 7.0%.

- Given the current share price of $176.7, the analyst price target of $190.05 is 7.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.