Key Takeaways

- Expansion in Latin America and growth through third-party financing options are expected to drive future revenue by enhancing customer access and flexibility.

- Strong customer loyalty programs and increased demand for luxury items are anticipated to boost merchandise sales, supporting earnings growth.

- Increasing financial pressures from wages, refinancing, and an acquisition could compress margins and impact EZCORP's growth and net earnings.

Catalysts

About EZCORP- Provides pawn services in the United States and Latin America.

- The addition of four new de novo stores in Latin America is expected to support earnings growth through increased revenue via expanded physical presence.

- Continued expansion of the third-party buy now, pay later program and the launch of a longer-term layaway option are anticipated to spur future revenue growth by attracting more customers seeking flexible financing options.

- Strong engagement with the EZ+ Rewards program is likely to enhance customer loyalty and drive future earnings by increasing repeat customer transactions, which accounted for 77% of all transactions in the quarter.

- Rising demand for affordable luxury items, evidenced by a 50% increase in Max Pawn's luxury e-commerce sales, especially through eBay sales, is projected to boost future merchandise sales revenue.

- The company's focus on both organic growth through de novo stores and inorganic growth through strategic acquisitions is positioned to enhance revenue and potentially increase net margins as scale efficiencies are realized over time.

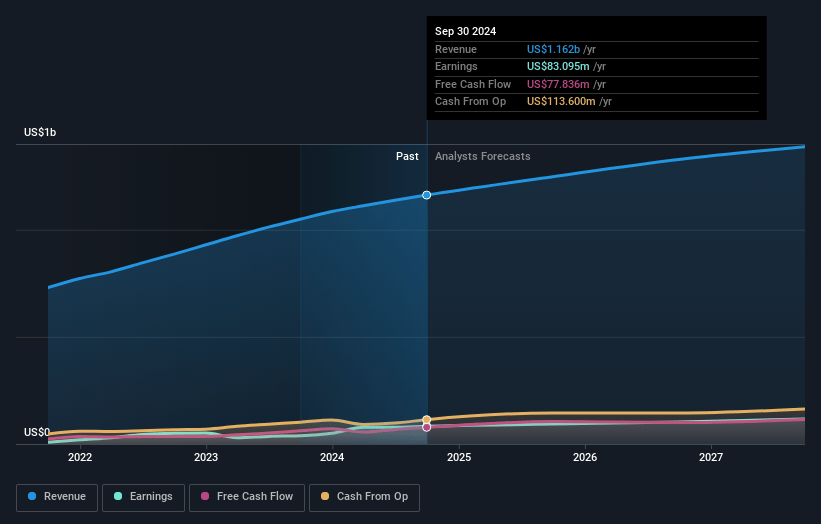

EZCORP Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming EZCORP's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.2% today to 8.8% in 3 years time.

- Analysts expect earnings to reach $124.3 million (and earnings per share of $1.61) by about March 2028, up from $85.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.5x on those 2028 earnings, up from 8.5x today. This future PE is lower than the current PE for the US Consumer Finance industry at 10.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.74%, as per the Simply Wall St company report.

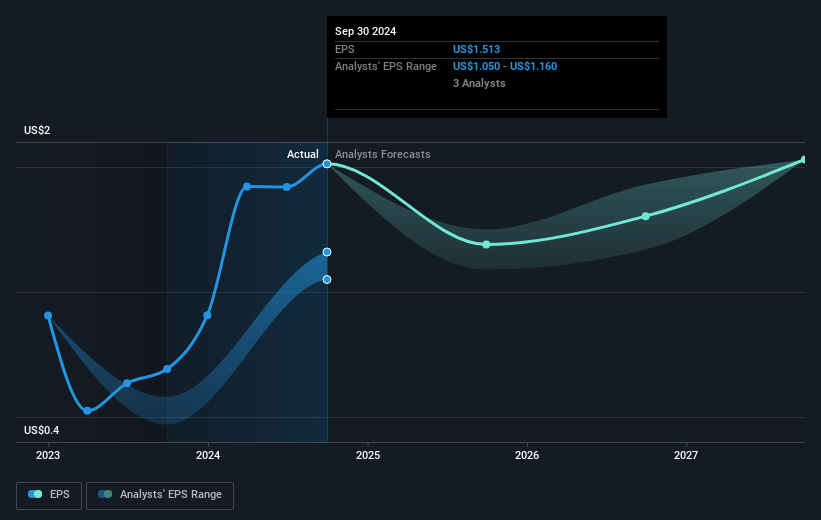

EZCORP Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's merchandise margin has dipped below 35% for the first time in several years, reflecting increased promotional activity and customer negotiation, which may pressure future margins.

- Plans to refinance $103 million of convertible notes due in May 2025 could expose the company to unfavorable financing terms or increased interest expenses, impacting net earnings.

- Wage increases of 6.5% to 12% in Latin America have affected salary expenses for 63% of team members, potentially compressing margins and affecting net earnings.

- Increasing wage demands and economic pressures may limit the company's ability to maintain its growth trajectory and could negatively impact operational costs and net margins.

- The pending acquisition of Auto Dinero and uncertainty around its completion may affect strategic expansion plans and the company's ability to grow its revenue and earnings in new markets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $17.0 for EZCORP based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $14.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.4 billion, earnings will come to $124.3 million, and it would be trading on a PE ratio of 9.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $13.18, the analyst price target of $17.0 is 22.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives