Key Takeaways

- Regulatory support and international expansion strategies are key opportunities for Coinbase to boost market share and revenue growth, especially through new legislation and high-growth regions.

- Diversifying crypto use into daily transactions and stablecoin payments could expand the user base and enhance subscription and services revenue, improving net margins.

- Increased competition and regulatory changes could challenge Coinbase's revenue and margin stability in volatile and evolving crypto markets.

Catalysts

About Coinbase Global- Operates platform for crypto assets in the United States and internationally.

- Regulatory tailwinds in the US are providing a significant opportunity for Coinbase to expand its market share and optimize its revenue streams. With the most pro-crypto Congress in history and potential new legislation on stable coins and market structures, this increases the potential for transaction volumes and earnings growth in the future.

- Coinbase's international expansion strategy is expected to continue driving revenue growth by replicating its successful market entry playbook in new, high-growth regions. The goal of achieving contribution margin positive in new markets will likely enhance net margins as well.

- The company's focus on developing crypto beyond trading into a utility for daily transactions, especially in stablecoin payments and applications, aims to drive substantial earnings through an expanded user base and diversified revenue streams.

- A stretch goal to make USDC the top dollar stablecoin, supported by network effects and compliance, posits growth in the company's subscription and services revenue. Expanding the market cap and use cases of USDC could have a positive impact on total revenue.

- Enhancing consultancy resources and policy efforts to support long-term crypto legislation suggests a strategic alignment to protect the company's financial interests and safeguard against future regulatory risks, potentially stabilizing net margin against unforeseen adverse developments.

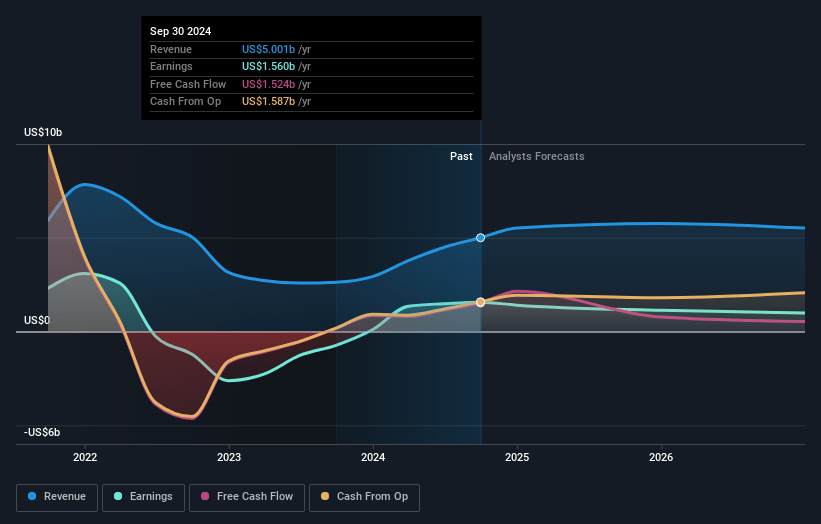

Coinbase Global Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Coinbase Global compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Coinbase Global's revenue will decrease by 0.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 41.0% today to 18.5% in 3 years time.

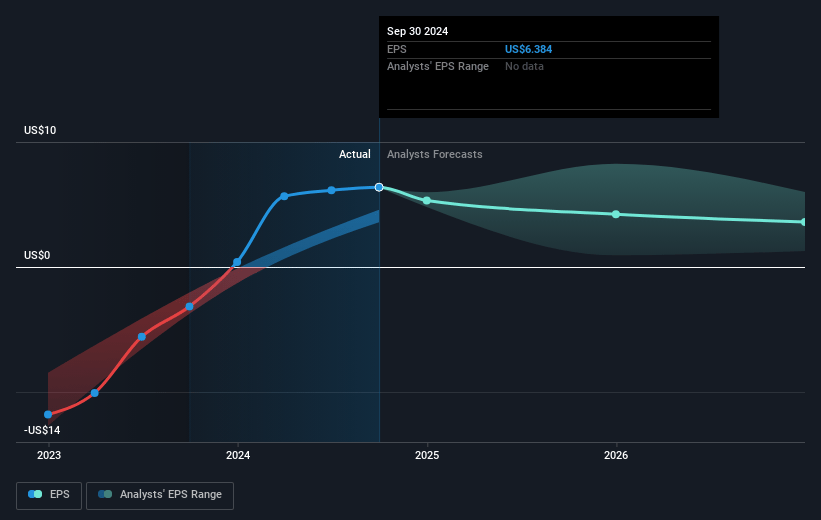

- The bearish analysts expect earnings to reach $1.1 billion (and earnings per share of $3.97) by about April 2028, down from $2.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 63.0x on those 2028 earnings, up from 17.3x today. This future PE is greater than the current PE for the US Capital Markets industry at 24.5x.

- Analysts expect the number of shares outstanding to grow by 3.38% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.28%, as per the Simply Wall St company report.

Coinbase Global Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The competitive landscape for derivatives trading seems intense, with an emphasis on keeping fees lower to build liquidity, which might impact Coinbase's long-term net margins.

- Regulatory changes such as SAB 122 could impact investor perceptions of Coinbase's balance sheet strength, potentially affecting market valuation and earnings.

- As international derivatives markets offer lower fees, this might lead to reduced revenue per transaction even if trade volume increases.

- The rise in competition from traditional finance platforms offering crypto trading solutions could pose a significant risk to Coinbase’s revenue from trading.

- With volatile crypto markets, Coinbase faces the challenge of maintaining profitable transaction revenues amidst fluctuations in trading volume and customer activity.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Coinbase Global is $208.7, which represents one standard deviation below the consensus price target of $287.19. This valuation is based on what can be assumed as the expectations of Coinbase Global's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $400.0, and the most bearish reporting a price target of just $169.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $6.2 billion, earnings will come to $1.1 billion, and it would be trading on a PE ratio of 63.0x, assuming you use a discount rate of 7.3%.

- Given the current share price of $175.57, the bearish analyst price target of $208.7 is 15.9% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:COIN. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.