Key Takeaways

- Expansion in small business services and high-margin subscriptions is expected to drive strong revenue and improve net margins.

- Advanced AI and digital tools in tax preparation may boost customer satisfaction, enhancing revenue and net margins in DIY tax services.

- Rising expenses, flat revenue, and increased competition from Intuit challenge H&R Block's earnings potential and threaten market share and revenue stability.

Catalysts

About H&R Block- Through its subsidiaries, engages in the provision of assisted and do-it-yourself (DIY) tax return preparation services to the general-public primarily in the United States, Canada, and Australia.

- H&R Block's emphasis on expanding its small business services with highly customized client experiences and double-digit growth in bookkeeping and payroll services could drive strong revenue growth.

- The increased adoption of high-margin subscription products within H&R Block's Wave platform, such as Pro-Tier and receipt services, suggests potential for higher net margins.

- The expansion of their mobile banking platform, Spruce, which has seen significant user growth and deposit increases, is likely to contribute to enhanced revenue and earnings through sustained year-round client engagement.

- The use of advanced AI technology and improved digital tools in tax preparation could enhance customer satisfaction and conversion rates, potentially bolstering revenue and net margins in the DIY tax services segment.

- H&R Block’s aggressive share repurchase program could lead to significant reductions in share count, boosting EPS growth even if revenue growth is modest.

H&R Block Future Earnings and Revenue Growth

Assumptions

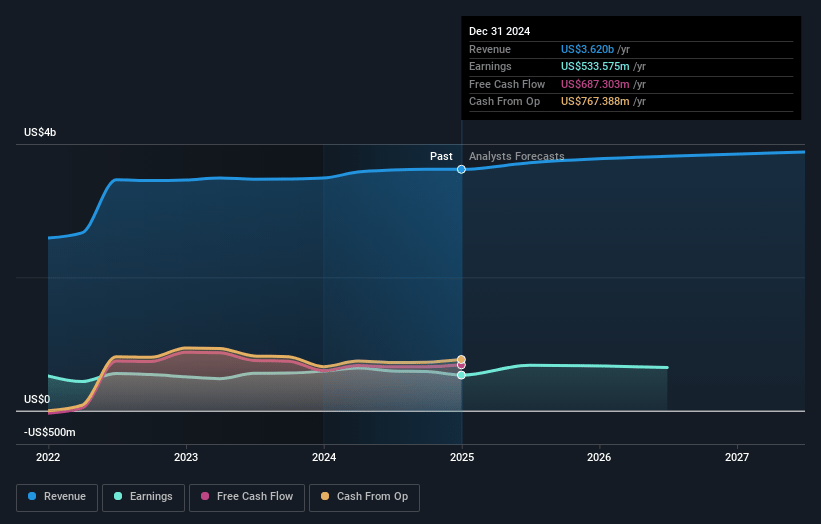

How have these above catalysts been quantified?- Analysts are assuming H&R Block's revenue will grow by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.7% today to 20.2% in 3 years time.

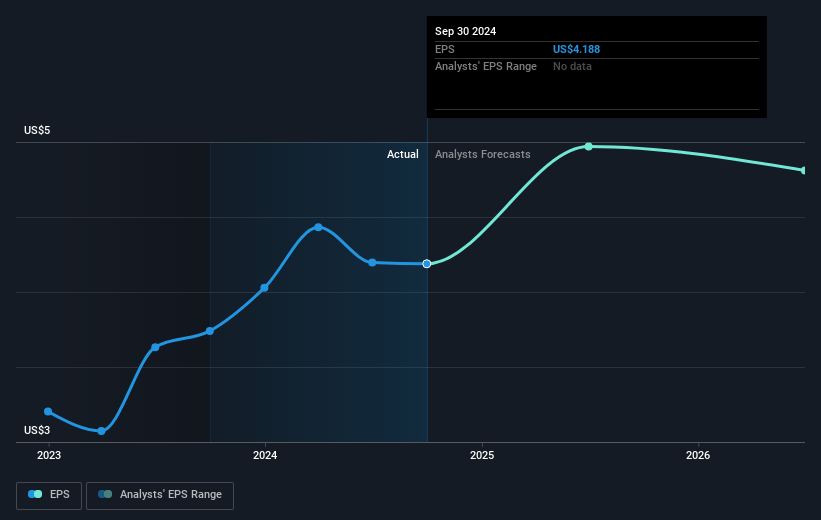

- Analysts expect earnings to reach $800.8 million (and earnings per share of $6.11) by about May 2028, up from $533.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.7x on those 2028 earnings, down from 15.4x today. This future PE is lower than the current PE for the US Consumer Services industry at 19.0x.

- Analysts expect the number of shares outstanding to decline by 4.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.99%, as per the Simply Wall St company report.

H&R Block Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- H&R Block experienced flat total revenue year-over-year in the second quarter, partly due to decreased volume of Emerald Advance loans. This downturn reflects potential challenges in expanding or sustaining new revenue streams. (Revenue)

- The company faced increased operating expenses, including higher tax professional and corporate wages, healthcare costs, and occupancy costs. These rising expenses could pressure net margins if not matched by equivalent revenue growth. (Net Margins)

- H&R Block's pretax loss in the second quarter increased from $283 million to $312 million year-over-year, primarily because of these increased expenses and flat revenues, indicating a potential risk to earnings if such trends continue. (Earnings)

- The competitive landscape is intensifying with the entry of Intuit into the Assisted tax preparation market and its established presence in DIY, potentially impacting H&R Block’s market share and revenue growth in both areas. (Revenue)

- There are uncertainties regarding the IRS and potential regulatory changes, such as the impact of Direct File, which may affect market dynamics and revenue from basic tax preparation services. (Revenue)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $59.5 for H&R Block based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $70.0, and the most bearish reporting a price target of just $49.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.0 billion, earnings will come to $800.8 million, and it would be trading on a PE ratio of 10.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of $61.2, the analyst price target of $59.5 is 2.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.