Key Takeaways

- Strategic acquisitions and loyalty program growth can drive revenue, enhance net margins, and improve customer retention for Hyatt Hotels.

- Adopting an asset-light model and record pipeline expansion aim to boost net margins and revenue with reduced capital expenses.

- Hyatt's financial stability is at risk due to acquisition-related debt, asset sales execution, franchise disruptions, and economic instability affecting revenue and earnings growth.

Catalysts

About Hyatt Hotels- Operates as a hospitality company in the United States and internationally.

- The acquisition of Playa Hotels & Resorts is expected to provide long-term management agreements and expand distribution channels through ALG Vacations and Unlimited Vacation Club, potentially driving revenue growth and enhancing net margins.

- The commitment to maintain an asset-light model by identifying third-party buyers for Playa's owned properties and other properties, aiming for 90% asset-light earnings by 2027, could improve net margins and earnings due to reduced capital expenses.

- The expansion of the hotel pipeline to a record high of 138,000 rooms demonstrates potential for increased revenue from new openings, with significant growth expected in organic net rooms by 2025.

- Business transient and group segments are showing strong demand, with group rooms revenue expected to increase by 7% in 2025, which could enhance both revenue and net margins as these segments are high-value customers.

- Record growth in loyalty membership through the World of Hyatt program, with innovative brand strategies and customer engagement, may lead to higher revenue through increased customer retention and spend.

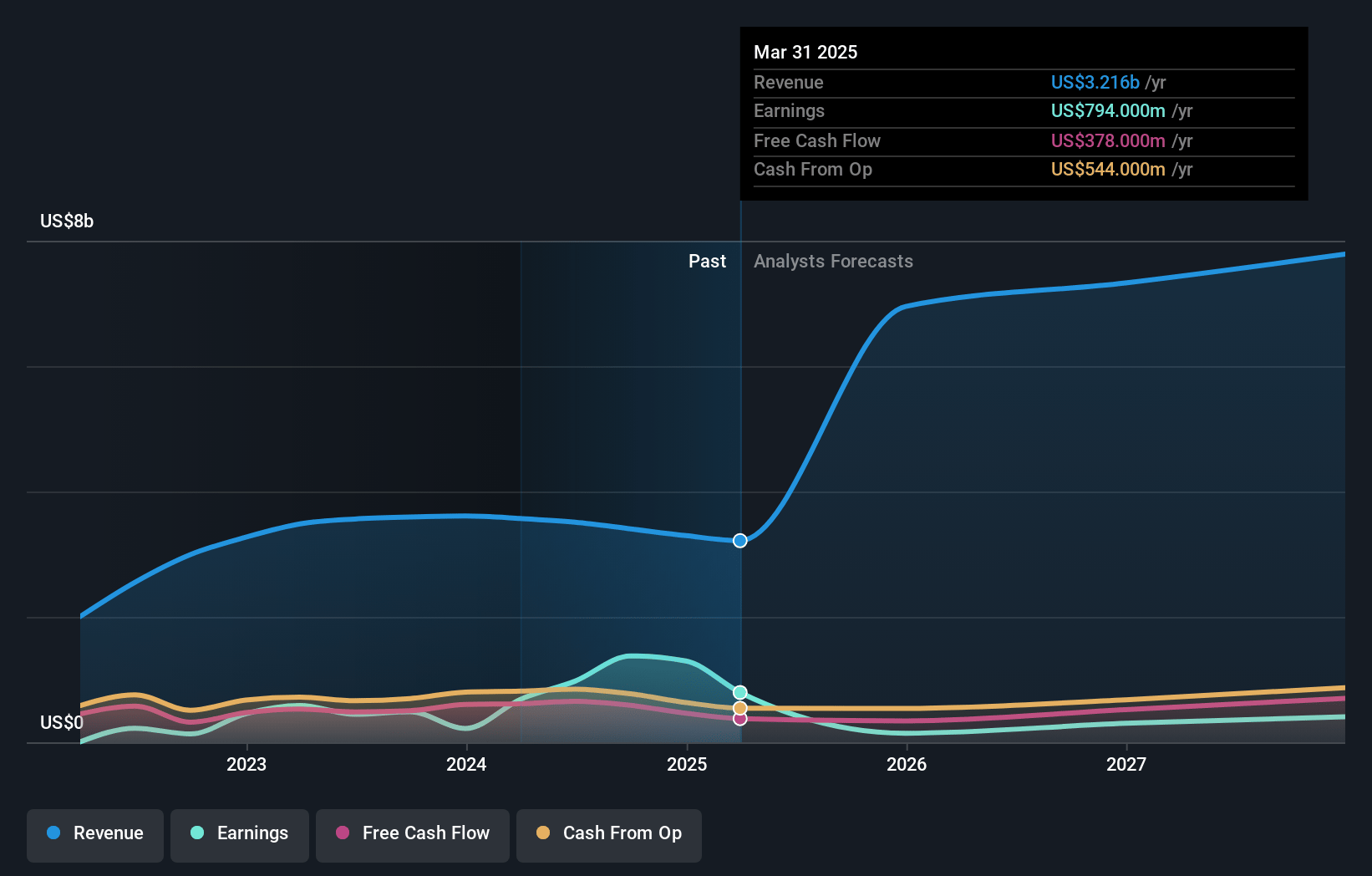

Hyatt Hotels Future Earnings and Revenue Growth

Assumptions

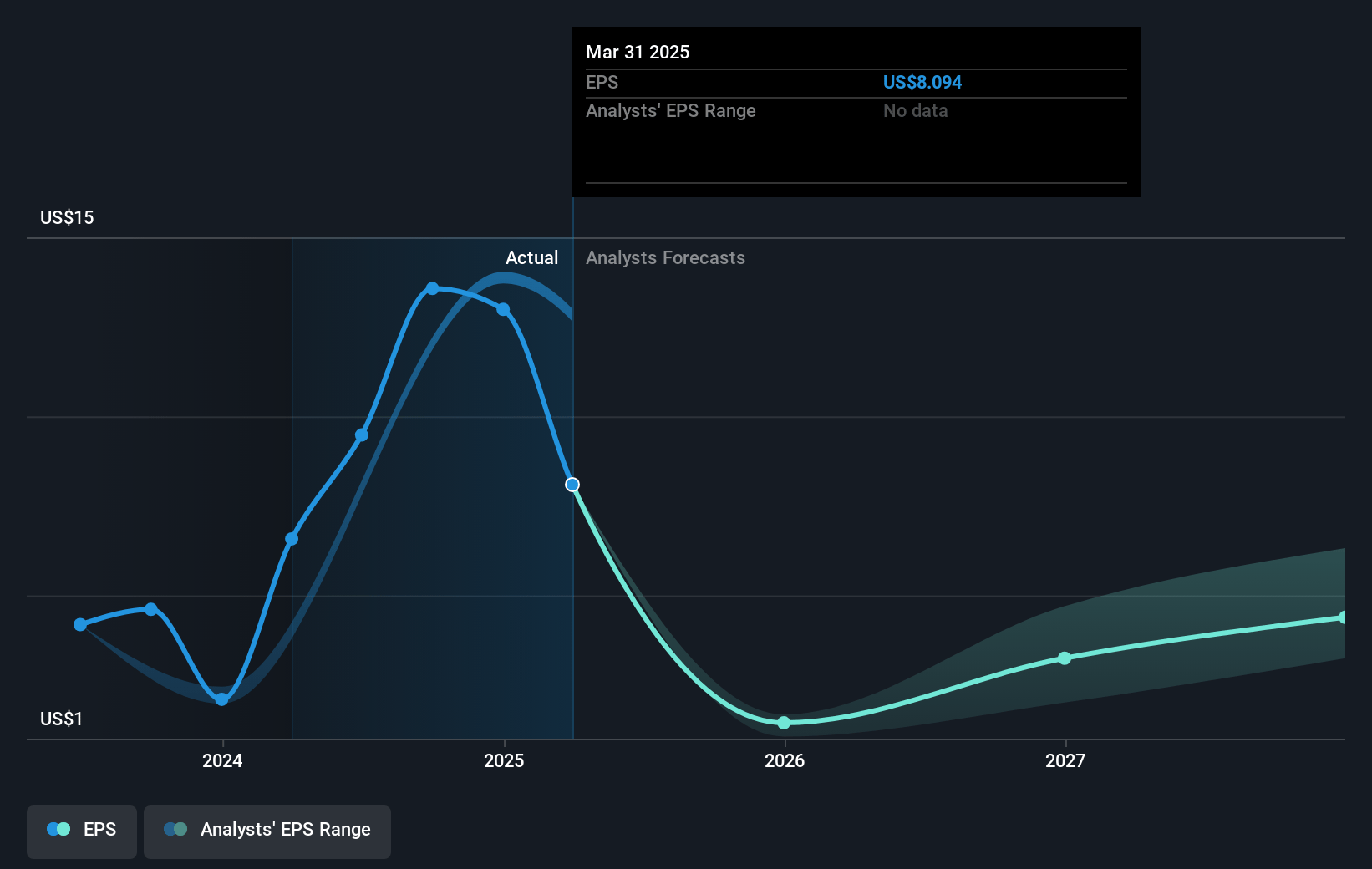

How have these above catalysts been quantified?- Analysts are assuming Hyatt Hotels's revenue will grow by 33.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 39.3% today to 6.2% in 3 years time.

- Analysts expect earnings to reach $488.3 million (and earnings per share of $5.89) by about April 2028, down from $1.3 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.8x on those 2028 earnings, up from 9.0x today. This future PE is greater than the current PE for the US Hospitality industry at 23.2x.

- Analysts expect the number of shares outstanding to decline by 4.97% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.52%, as per the Simply Wall St company report.

Hyatt Hotels Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Hyatt's acquisition of Playa Hotels & Resorts involves significant new debt financing and will require effective asset sales to maintain their investment-grade profile, which could impact the company's net margins and earnings if not executed as planned.

- The expectation to realize at least $2 billion from asset sales, including existing Hyatt assets and Playa's properties, introduces execution risk that might affect revenue and earnings if targets are not achieved by 2027.

- Potential insolvency-related disruptions with franchise agreements, like the issues with the Lindner Group in Germany, present attrition risks that could negatively impact Hyatt's net rooms growth and associated revenues.

- Economic and geopolitical instability, reflected by events like wildfires in Los Angeles and other global crises, could lead to downturns in travel demand, thereby impacting Hyatt's revenue and net margins.

- Hyatt's business strategy, aiming for a 90% asset-light earnings mix, may be challenged by market conditions and competitive pressures, affecting the overall earnings growth and projected financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $157.419 for Hyatt Hotels based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $201.0, and the most bearish reporting a price target of just $127.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $7.8 billion, earnings will come to $488.3 million, and it would be trading on a PE ratio of 33.8x, assuming you use a discount rate of 8.5%.

- Given the current share price of $121.78, the analyst price target of $157.42 is 22.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.