Narratives are currently in beta

Key Takeaways

- Growth strategies include site optimization, game improvements, and acquisitions, which are anticipated to increase revenue and enhance margins.

- Emphasis on capital allocation and operational efficiencies aims to improve cash flow and boost returns on capital and earnings per share.

- Strategic moves, like closing locations and heavy CapEx investment, indicate challenges in maintaining growth, compounded by uncertainties in new market and technology efficiencies.

Catalysts

About Accel Entertainment- Operates as a distributed gaming operator in the United States.

- The company expects growth in revenue from optimizing its location portfolio by closing underperforming sites and opening promising new ones, which will improve the revenue per location and enhance net margins.

- The pending acquisition of Fairmont Park, including a partnership with FanDuel for sports betting, is expected to drive significant future revenue, especially with the planned development of a casino that will expand earnings.

- The introduction of ticket in, ticket out (TITO) is anticipated to increase operational efficiency and enhance customer experience, potentially boosting revenue and net margins by attracting more players.

- Strategic product shifts in existing markets, such as replacing lower-performing games with higher-performing ones, aim to increase hold per day, improving both revenue and net margins.

- A strong capital allocation strategy, including share repurchases, and decreasing capital expenditures towards $40 million, will likely improve cash flow and provide higher returns on invested capital, impacting EPS positively.

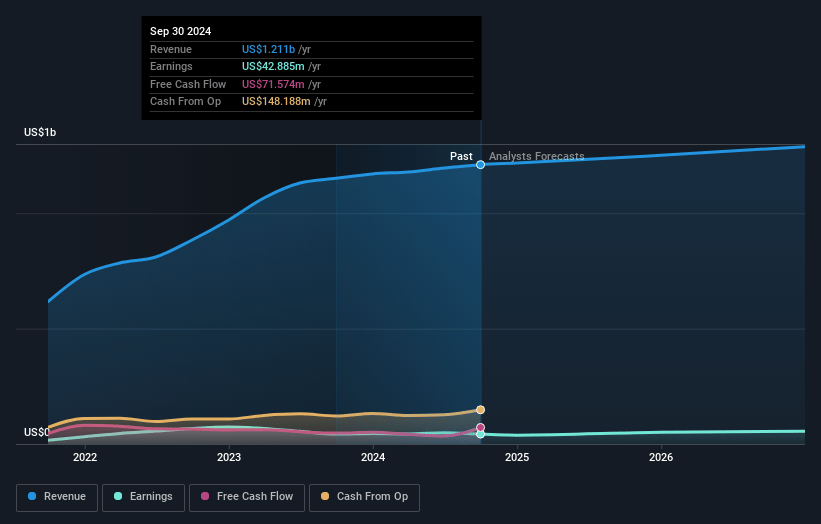

Accel Entertainment Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Accel Entertainment's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.5% today to 4.8% in 3 years time.

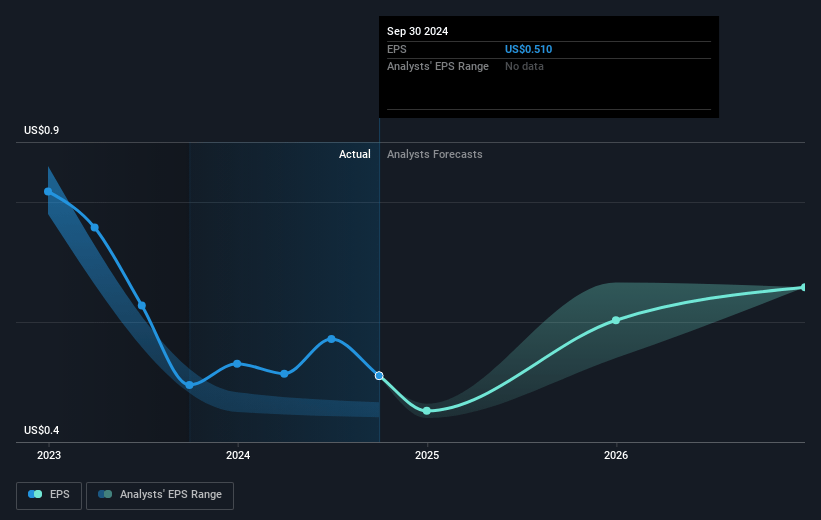

- Analysts expect earnings to reach $62.7 million (and earnings per share of $0.74) by about November 2027, up from $42.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.3x on those 2027 earnings, up from 21.9x today. This future PE is greater than the current PE for the US Hospitality industry at 24.4x.

- Analysts expect the number of shares outstanding to grow by 0.82% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.78%, as per the Simply Wall St company report.

Accel Entertainment Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's decision to close underperforming locations in Illinois, driven by factors like recent tax increases and inflation in wages, suggests potential challenges in maintaining revenue growth and margins.

- The projected financial information presented is for illustrative purposes only, and the company emphasizes that actual results may differ materially, introducing uncertainty in future earnings expectations.

- While investments in technologies like TITO could positively impact operations, the timeline and effectiveness of such regulatory changes remain uncertain and could affect both revenue generation and efficiency improvements.

- The company's heavy investment in CapEx, particularly in Illinois, may not immediately result in higher returns as anticipated, impacting near-term free cash flow and overall capital returns.

- During strategic expansion, there is a risk that the anticipated synergies and returns from acquisitions, like the Fairmont project, and opportunities in new markets may not fully materialize, potentially affecting long-term profitability and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $14.67 for Accel Entertainment based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.3 billion, earnings will come to $62.7 million, and it would be trading on a PE ratio of 25.3x, assuming you use a discount rate of 8.8%.

- Given the current share price of $11.42, the analyst's price target of $14.67 is 22.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives