Key Takeaways

- Data-driven marketing and digital innovations may increase customer acquisition and retention, boosting revenue and sales growth.

- International expansion and effective supply-chain strategies can enhance global growth, improve margins, and stabilize earnings long-term.

- Economic uncertainty, competition, and debt-related expenses challenge Wingstop's revenue growth, profit margins, and earnings despite expansion efforts.

Catalysts

About Wingstop- Wingstop Inc., together with its subsidiaries, franchises and operates restaurants under the Wingstop brand.

- Wingstop is focused on scaling brand awareness, leveraging data-driven marketing, and implementing digital innovations, which could lead to increased customer acquisition and retention, positively impacting revenue and overall sales growth.

- The introduction of a proprietary AI-enabled kitchen operating platform aims to improve service speed and consistency, thereby unlocking unmet demand. This could drive higher average unit volumes (AUVs) and ultimately boost earnings and net margins.

- The successful international expansion strategy, demonstrated by the acquisition of the Wingstop U.K. business, highlights the brand's potential for further growth globally. This could significantly enhance system-wide sales and revenue in the coming years.

- Continued investments in digital transformation, evidenced by the MyWingstop platform, are expected to enhance customer personalization and engagement. Improved customer experience can drive transaction growth, impacting revenue positively.

- An effective supply-chain strategy and focus on unit economics help predict and control food costs, potentially improving net margins and cash flows, supporting the company's long-term growth aspirations and earnings stability.

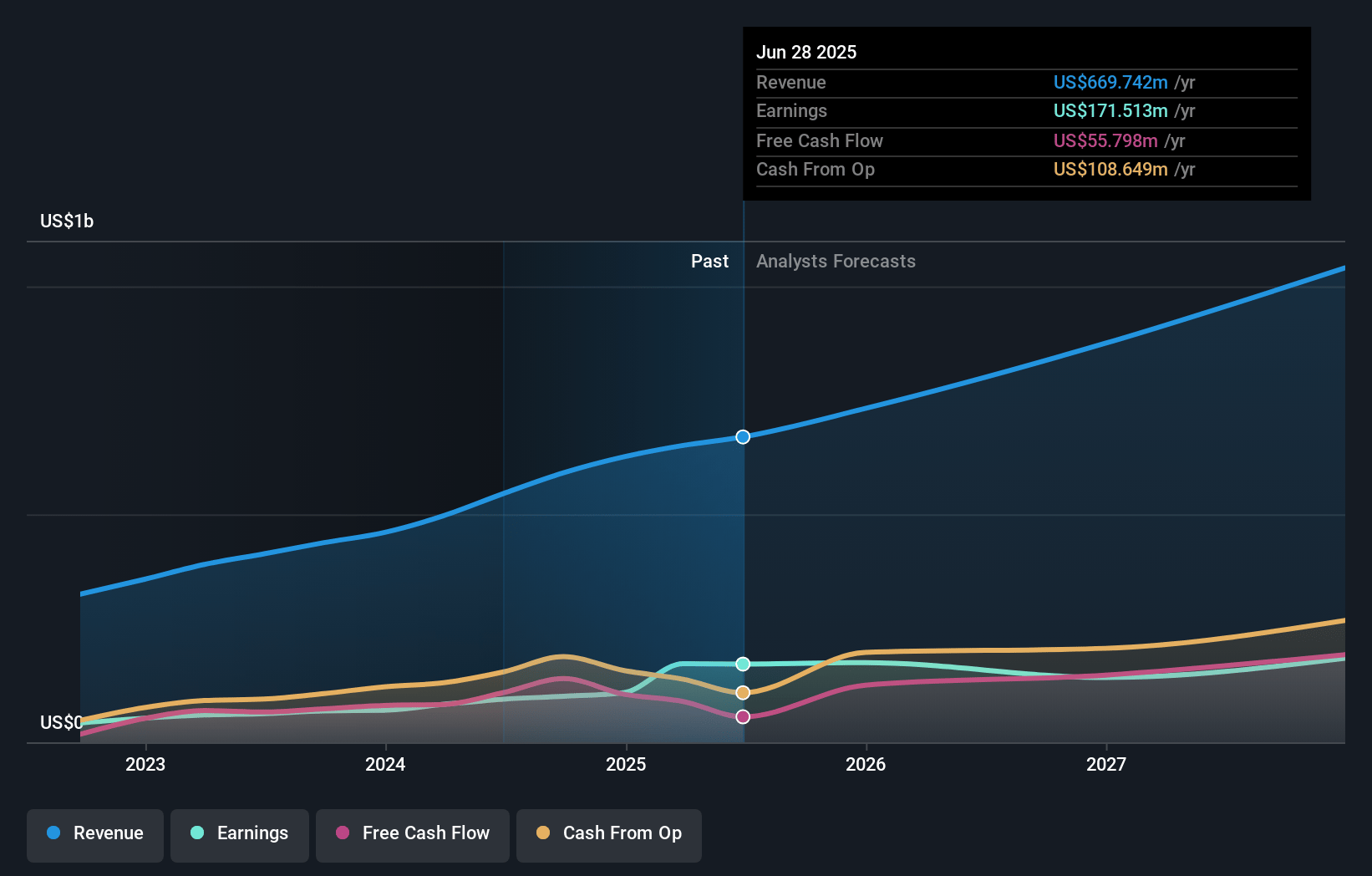

Wingstop Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Wingstop's revenue will grow by 17.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.4% today to 16.8% in 3 years time.

- Analysts expect earnings to reach $171.3 million (and earnings per share of $6.26) by about April 2028, up from $108.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $190.1 million in earnings, and the most bearish expecting $148.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 59.9x on those 2028 earnings, down from 62.3x today. This future PE is greater than the current PE for the US Hospitality industry at 23.2x.

- Analysts expect the number of shares outstanding to decline by 2.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.12%, as per the Simply Wall St company report.

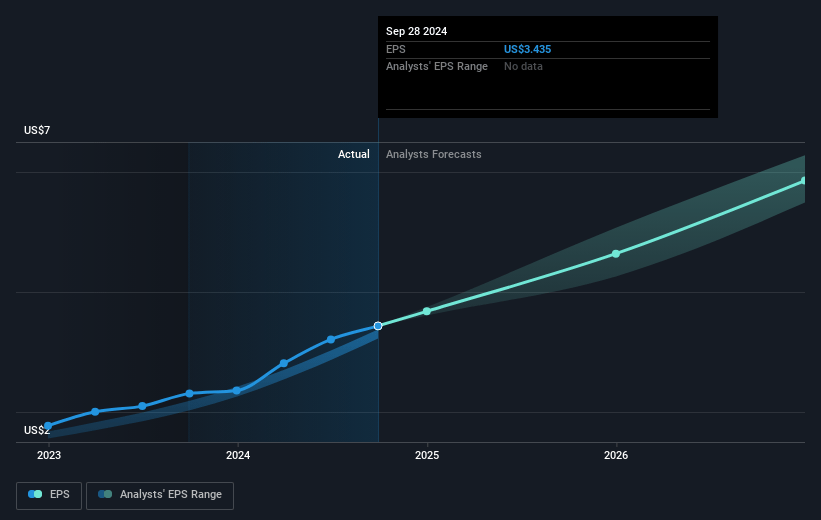

Wingstop Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's same-store sales outlook for 2025 is low to mid-single digits, influenced by challenging laps from previous years. This indicates potential difficulty in maintaining high growth rates, which could impact future revenue and earnings growth.

- Wingstop's accelerated unit growth may lead to cannibalization, potentially moderating same-store sales if not managed carefully, impacting revenue per location and overall sales growth.

- Increased competition and aggressive value promotions in the QSR sector may pressure Wingstop to compete on price, potentially affecting profit margins and revenue if the company needs to adjust its pricing strategy.

- There is economic uncertainty and increased consumer anxiety, which might influence consumer spending behavior adversely, particularly in dining out frequencies, potentially impacting transaction counts and overall revenue.

- Rising interest expense due to recent securitization transaction reduces earnings per share, which could put pressure on net earnings if the additional debt does not translate into proportionate revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $312.505 for Wingstop based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $400.0, and the most bearish reporting a price target of just $181.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.0 billion, earnings will come to $171.3 million, and it would be trading on a PE ratio of 59.9x, assuming you use a discount rate of 8.1%.

- Given the current share price of $236.4, the analyst price target of $312.5 is 24.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.