Narratives are currently in beta

Key Takeaways

- Strategic expansion into breakfast and digital sales aims to elevate revenue, profitability, and market presence.

- Global expansion and AI-driven efficiencies are targeted to boost operating margins and strengthen financial growth.

- Strategic closures and economic pressures may hinder revenue growth and long-term profitability due to limited margin expansion and consumer demand volatility.

Catalysts

About Wendy's- Operates as a quick-service restaurant company in the United States and internationally.

- Wendy’s is accelerating its focus on the breakfast daypart, which is experiencing mid-single-digit growth and is expected to continue outpacing other dayparts, providing a significant opportunity for incremental revenue and profitability.

- The company is enhancing its digital operations, with global digital sales increasing by almost 40% year-over-year, suggesting continued growth in digital sales could significantly boost revenue and improve net margins due to potential efficiencies and higher average checks.

- Wendy’s plans to open 250 to 300 new restaurants annually, focusing on international expansion, particularly in high-growth areas like Canada and Latin America. This expansion is expected to boost system-wide sales and potentially drive higher operating margins due to scale efficiencies.

- The initiative to close underperforming restaurants and replace them with new locations in better trade areas is anticipated to bolster average unit volumes (AUVs) and improve overall system profitability, supporting net income growth.

- Wendy’s plans to expand its use of AI voice-enabled ordering in drive-thrus, enhancing operational efficiencies by reducing labor costs, which can improve net margins and support earnings growth.

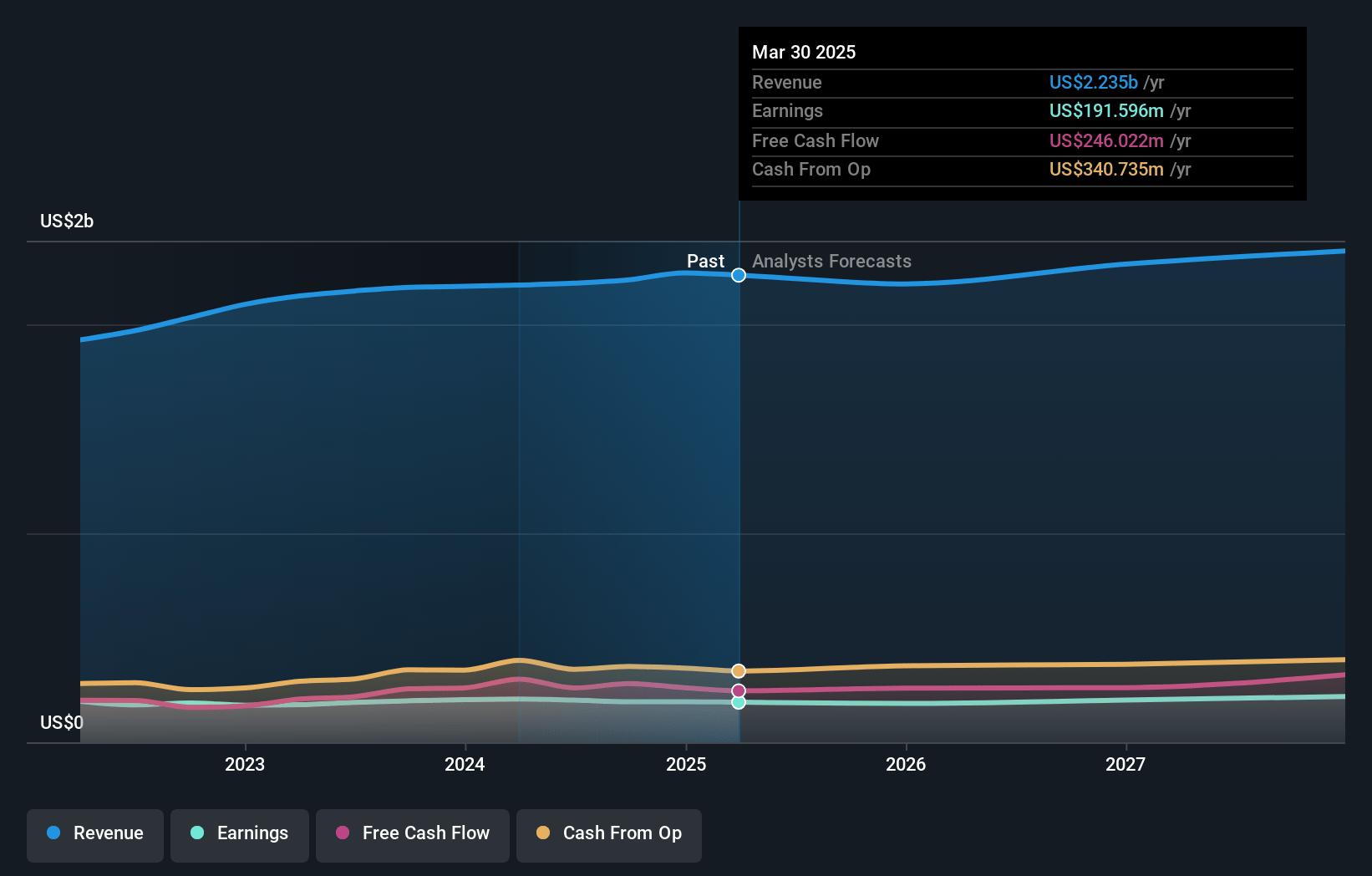

Wendy's Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Wendy's's revenue will grow by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.8% today to 10.0% in 3 years time.

- Analysts expect earnings to reach $241.9 million (and earnings per share of $1.29) by about November 2027, up from $193.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.9x on those 2027 earnings, up from 20.8x today. This future PE is lower than the current PE for the US Hospitality industry at 23.4x.

- Analysts expect the number of shares outstanding to decline by 2.72% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 9.6%, as per the Simply Wall St company report.

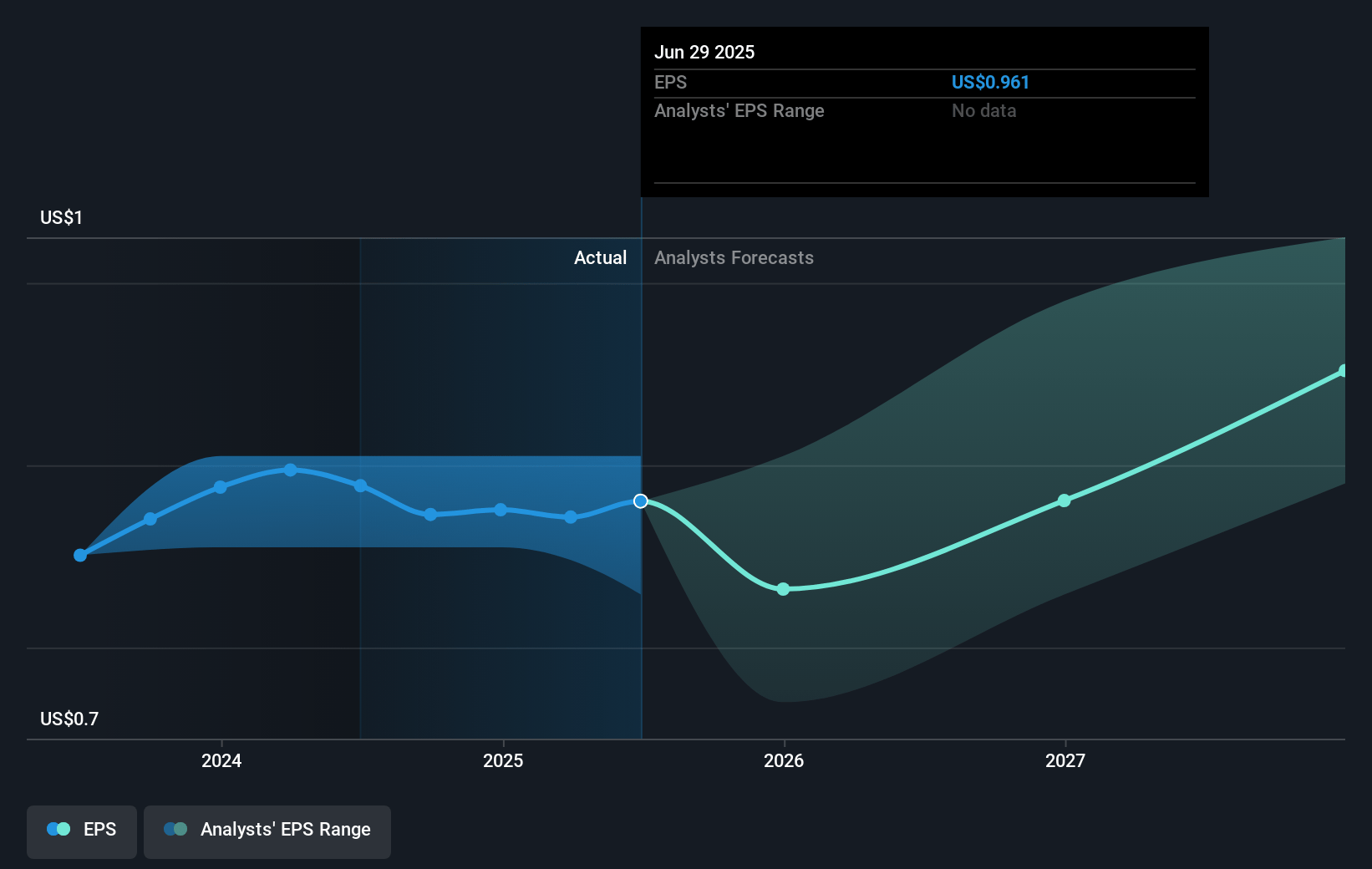

Wendy's Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The strategic decision to close outdated and underperforming restaurants, which have AUVs of $1.1 million and operating margins below the system average, may lead to flat net unit growth in 2024, affecting long-term revenue growth.

- Despite sales growth in certain areas, there is pressure from labor rate inflation and a decline in customer count, which could limit improvements in net margins.

- The company's adjusted EBITDA decreased by 2.9%, influenced by increased investment in breakfast and rising general and administrative expenses, indicating potential risks to overall earnings growth.

- The company is maintaining U.S. company restaurant margins at a narrow range of 15% to 16%, suggesting limited room for margin expansion, which could restrict long-term profitability improvements.

- Challenging macroeconomic conditions and the softer category environment in Q3 point to potential volatility in consumer demand, which could impact future revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $20.54 for Wendy's based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $29.0, and the most bearish reporting a price target of just $17.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $2.4 billion, earnings will come to $241.9 million, and it would be trading on a PE ratio of 20.9x, assuming you use a discount rate of 9.6%.

- Given the current share price of $19.77, the analyst's price target of $20.54 is 3.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives