Key Takeaways

- Legalization of online gaming in more U.S. states could significantly expand DraftKings' market reach and customer base.

- Strategic acquisitions and focus on live betting aim to boost customer engagement, retention, and market share expansion.

- DraftKings faces potential revenue challenges from reliance on promotions, uncertain state expansions, handle growth stagnation, risky international moves, and intense iGaming competition.

Catalysts

About DraftKings- Operates as a digital sports entertainment and gaming company in the United States and internationally.

- An anticipated growth in DraftKings' structural Sportsbook hold percentage and improved product offerings, especially through the acquisition of Simplebet and other firms, suggests potential revenue growth as it enhances customer engagement and betting yields.

- The imminent legalization of online gaming in additional U.S. states could significantly increase DraftKings' market reach, boosting future revenues and expanding their customer base.

- The expansion of DraftKings' digital lottery courier channel, with successful cross-sell strategies exemplified by Jackpocket, indicates potential revenue growth and increased customer acquisition at minimal cost.

- With a focus on live betting, supported by recent technology acquisitions, DraftKings aims to enhance user experience and capture greater market share, potentially increasing revenue through higher customer retention and engagement.

- Plans to explore international markets for online gaming signal a strategic opportunity to diversify and expand revenue streams, capitalizing on DraftKings’ established brand and technological capabilities.

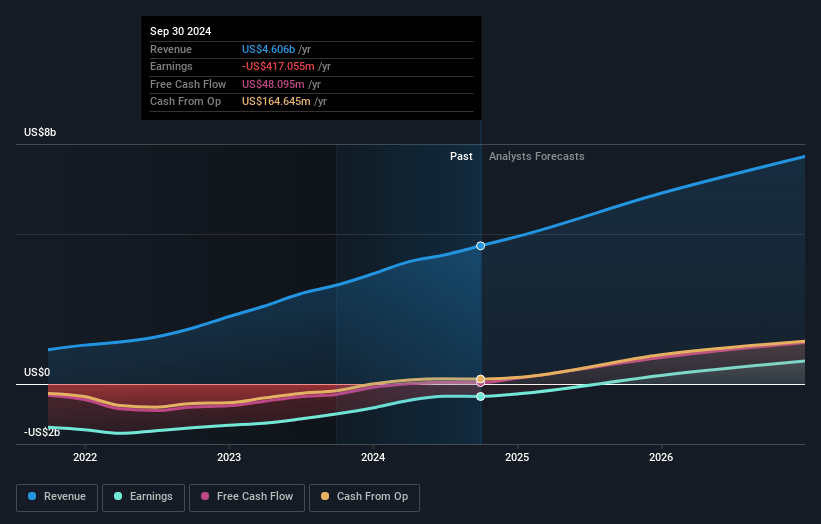

DraftKings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on DraftKings compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming DraftKings's revenue will grow by 25.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -10.6% today to 15.2% in 3 years time.

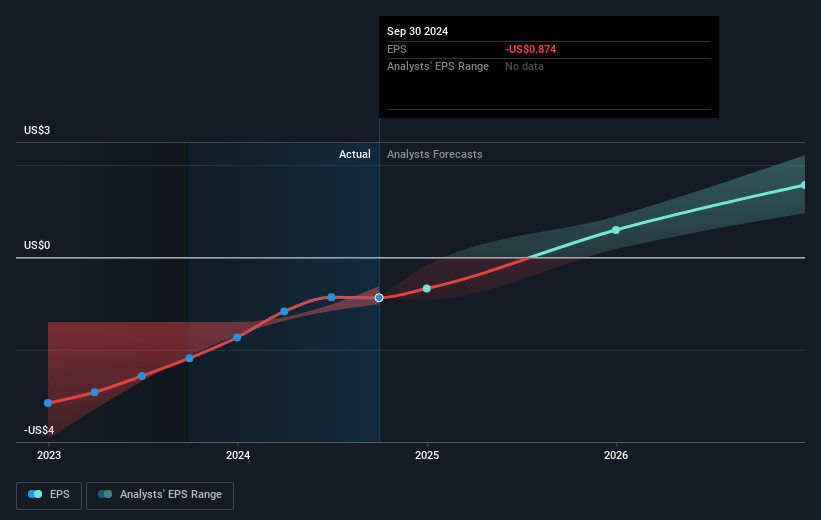

- The bullish analysts expect earnings to reach $1.4 billion (and earnings per share of $2.79) by about April 2028, up from $-507.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 34.9x on those 2028 earnings, up from -33.0x today. This future PE is greater than the current PE for the US Hospitality industry at 22.4x.

- Analysts expect the number of shares outstanding to grow by 2.88% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.71%, as per the Simply Wall St company report.

DraftKings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Although DraftKings is optimistic about reducing promotional intensity, if this reduction doesn't materialize, it could negatively impact net revenues as they rely heavily on promotions to attract and retain customers.

- The uncertainty surrounding new state legalizations could impact DraftKings' forecasted revenue growth, especially if they do not realize anticipated market expansions in states such as Missouri.

- Economists are concerned about a potential plateauing of handle growth, which if not reversed, could impact the anticipated revenue growth rates due to stagnation in market engagement and customer acquisition.

- Investors are wary about DraftKings' exploration of international expansion, which could introduce significant risk and divert capital from potentially more lucrative and established markets in the U.S., thereby impacting earnings.

- The competitive market environment, particularly the promotional landscape in iGaming, could undermine profit margins and affect their long-term guidance if rival companies increase promotional activities aggressively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for DraftKings is $72.92, which represents two standard deviations above the consensus price target of $55.57. This valuation is based on what can be assumed as the expectations of DraftKings's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $35.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $9.4 billion, earnings will come to $1.4 billion, and it would be trading on a PE ratio of 34.9x, assuming you use a discount rate of 7.7%.

- Given the current share price of $33.47, the bullish analyst price target of $72.92 is 54.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NasdaqGS:DKNG. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.