Last Update 10 Dec 25

Fair value Increased 0.096%BJ: Record Renewal Momentum And Digital Expansion Will Support Defensive Upside Potential

BJ's Wholesale Club Holdings' analyst price target edged modestly higher, with fair value rising to approximately $109.26 from about $109.16, as analysts balance slightly softer revenue growth expectations against marginally improved profit margins and a more favorable discount rate backdrop.

Analyst Commentary

Analyst views on BJ's Wholesale Club remain mixed, with recent target changes reflecting a balance between solid membership fundamentals and growing concerns about near term execution risks.

Bullish Takeaways

- Bullish analysts highlight BJ's member centric model, pointing to record renewal rates as evidence of a loyal, recurring revenue base that supports premium valuation multiples.

- Robust digital momentum, including roughly 30 percent year over year growth in online sales, is viewed as a key driver of incremental traffic and higher lifetime value, reinforcing the case for sustained earnings growth.

- The stock is described as attractively priced and defensive, with a clear road map for mid single digit revenue growth and high single to low double digit EPS growth, which is cited as supporting upside to intrinsic value over the medium term.

- Some recent target increases, even when ratings remain neutral or in line, are interpreted as a sign that analysts see improved profit leverage and cash generation partially offsetting softer near term comp trends.

Bearish Takeaways

- Bearish analysts emphasize that comparable sales momentum has deteriorated, with recent misses reinforcing concerns that topline growth may remain below prior expectations.

- Holiday performance is viewed as a key risk, as more promotion sensitive consumers could force deeper discounts, pressuring margins and limiting upside to current earnings forecasts.

- There is an expectation that BJ's will need incremental price and wage investments to stabilize market share and improve inventory turnover, which could weigh on near term profitability and is used to justify more conservative price targets.

- Cyclical headwinds and intensifying competitive pressures within the warehouse club channel are cited as reasons to temper valuation expansion, keeping some analysts neutral despite the longer term growth story.

What's in the News

- Announced plans to open three new clubs in December in Springfield, Massachusetts, Sumter, South Carolina, and Casselberry, Florida, each with on site gas stations and expanded member services (company press release).

- Detailed broader expansion plans, including new locations in Mesquite, Texas, Foley, Alabama, and a relocation of the Rotterdam, New York, club, as part of a pipeline of 25 to 30 new clubs slated for fiscal 2025 and 2026 (company press release).

- Opened a new club in Sevierville, Tennessee, the company’s fifth in the state, alongside a new gas station and a community partnership with Second Harvest Food Bank of East Tennessee supported by a $75,000 grant (company press release).

- Completed a share repurchase tranche totaling 1,335,000 shares, or about 1.01% of shares outstanding, for $134.74 million under a buyback program announced in November 2024 (company filing).

- Narrowed full year fiscal 2025 earnings guidance while reiterating expectations for 2.0% to 3.0% comparable club sales growth excluding gasoline, citing solid year to date performance in a volatile environment (company guidance update).

Valuation Changes

- Fair Value: Risen slightly to approximately $109.26 from about $109.16, reflecting a modest upward revision in intrinsic value estimates.

- Discount Rate: Declined marginally to roughly 7.23% from about 7.26%, signaling a slightly more favorable risk and rate environment in valuation models.

- Revenue Growth: Eased modestly to around 6.15% from roughly 6.36%, indicating slightly softer top line expectations.

- Net Profit Margin: Improved slightly to about 2.79% from approximately 2.76%, suggesting a small uplift in projected profitability.

- Future P/E: Edged lower to roughly 24.23x from about 24.50x, pointing to a marginally less aggressive multiple on forward earnings.

Key Takeaways

- Accelerated membership and footprint expansion in new markets strengthens recurring income and supports long-term revenue and margin growth.

- Growing digital adoption and enhanced merchandising increase customer loyalty, shopping frequency, and operational efficiency amidst value-focused consumer trends.

- Macroeconomic pressures, shifting consumer behavior, and rising costs threaten revenue growth, margins, and long-term relevance, while demographic trends could structurally challenge BJ's bulk-buying business model.

Catalysts

About BJ's Wholesale Club Holdings- Operates membership warehouse clubs on the eastern half of the United States.

- Accelerating membership growth, particularly in higher-tier memberships and underpenetrated secondary markets, is likely to boost recurring revenues and expand BJ's addressable market, providing a strong base for future earnings growth.

- Expansion of BJ's physical footprint, with 25–30 new clubs planned over two years, especially in high-growth suburban and Sunbelt markets, supports sustained topline revenue growth and fixed cost leverage, which helps drive margin expansion.

- Robust digital adoption-evidenced by 34% quarterly digital sales growth and broad penetration of digital services like BOPIC and ExpressPay-positions BJ's to capture more shopping occasions and larger baskets as omnichannel shopping continues to rise, supporting both revenue and operating efficiencies.

- Ongoing investments in Fresh 2.0 (perishables, meat, and seafood), private label, and data-driven merchandising are increasing customer loyalty, improving basket size, and lifting gross margin rates, all of which are likely to result in higher long-term net margins.

- The current economic environment, marked by persistent inflation and elevated value-seeking consumer behavior, is driving increased traffic-particularly among lower income households-validating BJ's value proposition and supporting market share gains that should translate into higher revenues and durable earnings resilience.

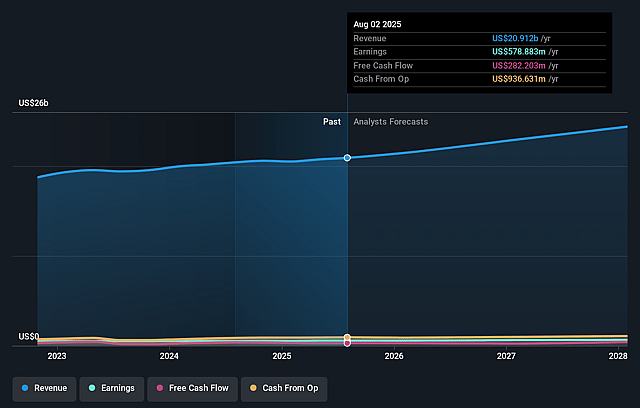

BJ's Wholesale Club Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BJ's Wholesale Club Holdings's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 2.8% today to 2.7% in 3 years time.

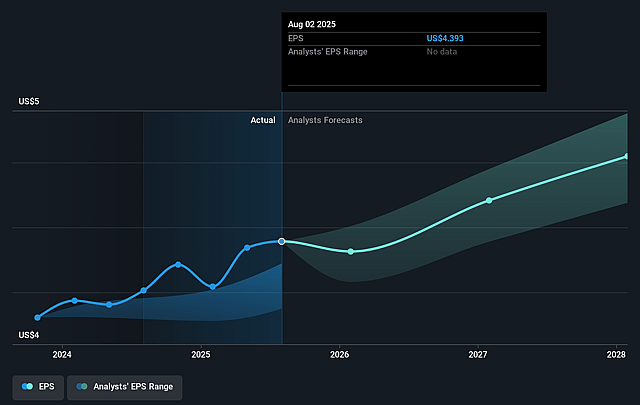

- Analysts expect earnings to reach $683.1 million (and earnings per share of $5.4) by about September 2028, up from $578.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 26.8x on those 2028 earnings, up from 22.2x today. This future PE is greater than the current PE for the US Consumer Retailing industry at 21.7x.

- Analysts expect the number of shares outstanding to decline by 0.63% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.08%, as per the Simply Wall St company report.

BJ's Wholesale Club Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is experiencing increased caution in its inventory and order levels, particularly in discretionary general merchandise categories impacted by tariffs, which could constrain revenue growth if consumer sentiment unexpectedly improves, and over-prudence may limit top-line upside.

- Tariff-related macro volatility and ongoing uncertainty about consumer behavior are creating a more dynamic and risk-prone environment; management explicitly stated that these headwinds are likely to limit upside and may require short-term investments (e.g., sharper pricing), which could negatively affect net margins and earnings.

- There is a continued struggle with underperformance in the general merchandise and services division (2.2% comp decline this quarter), with challenges in transforming this business for greater relevance; if this trend persists, it could weigh down average basket size and future revenue growth.

- Long-term margin pressures loom due to increased SG&A expense deleverage from new club openings amid rising labor and operational costs, as well as the potential for intensifying price competition in warehouse retail, which could erode operating margins and overall profitability.

- Secular trends such as demographic shifts toward smaller households and increased sustainability/anti-consumption sentiment among younger generations may reduce consumer demand for bulk-buying over time, creating a structural headwind to membership growth and revenue across BJ's core business model.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $115.632 for BJ's Wholesale Club Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $130.0, and the most bearish reporting a price target of just $70.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $25.2 billion, earnings will come to $683.1 million, and it would be trading on a PE ratio of 26.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $97.53, the analyst price target of $115.63 is 15.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on BJ's Wholesale Club Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.