Last Update 31 Oct 25

Fair value Decreased 6.67%Analysts have lowered their fair value estimate for Ethan Allen Interiors from $30.00 to $28.00, citing expectations of slower revenue growth and reduced profit margins.

What's in the News

- Ethan Allen opened a new Design Center in Colorado Springs, marking its fourth location in Colorado. The center offers expanded interior design services at 5310 North Nevada Avenue (Key Developments).

- The new Design Center features a gallery showroom and designer workspaces. It offers custom furniture and accents, with 75% of products manufactured in North America (Key Developments).

- Ethan Allen designers are providing full-service interior design at no additional charge, including at-home and virtual appointments as well as 3D room previews (Key Developments).

- As of June 30, 2025, the company has completed the repurchase of 15,160,095 shares, representing 44.78%, for $450.43 million under its ongoing buyback program (Key Developments).

Valuation Changes

- Fair Value Estimate: Lowered from $30.00 to $28.00, reflecting analyst adjustments.

- Discount Rate: Increased slightly from 8.63% to 8.68%.

- Revenue Growth: Reduced from 1.94% to 1.61%, signaling more conservative expectations.

- Net Profit Margin: Decreased from 7.83% to 6.22%, indicating expectations of thinner profitability.

- Future P/E Ratio: Increased from 18.85x to 23.59x, suggesting a higher valuation relative to future earnings.

Key Takeaways

- Heavy reliance on traditional showrooms and North American markets increases vulnerability to digital disruption and regional economic changes.

- Margin growth is limited by high fixed costs and rising competition from online and budget retailers, straining pricing power and long-term sales.

- Strong operational efficiency, financial stability, and product customization have increased profitability and resilience, enabling Ethan Allen to adapt to shifting consumer trends and maintain long-term growth.

Catalysts

About Ethan Allen Interiors- Operates as an interior design company, and manufacturer and retailer of home furnishings in the United States and internationally.

- Investors appear to be pricing in ongoing pressure from the continued shift of furniture sales to e-commerce and direct-to-consumer channels, which threatens Ethan Allen's more traditional, showroom-dependent operating model and could lead to slower revenue growth relative to industry peers with stronger digital-first capabilities.

- The market expects that the company's concentrated focus on North American manufacturing and sales exposes it to regional macroeconomic volatility and limits diversification, potentially resulting in more pronounced swings in revenue and earnings, particularly during U.S. economic slowdowns.

- Ethan Allen's strong gross and operating margins-helped by significant cost control and technology-led efficiency gains-may have limited further upside as fixed costs remain high due to its capital-intensive retail footprint, suggesting margin expansion from current levels is unlikely and could reverse if sales weaken.

- There are concerns that an aging demographic in developed markets, particularly among Ethan Allen's core higher-income segments, may result in less demand for large-ticket premium furniture as downsizing and reduced home spending accelerate, ultimately capping medium

- to long-term revenue growth.

- Increased competitive pressure from online and value-oriented furniture retailers is likely to constrain the company's pricing power and may force greater promotional activity to maintain market share, which could compress net margins and limit future earnings growth.

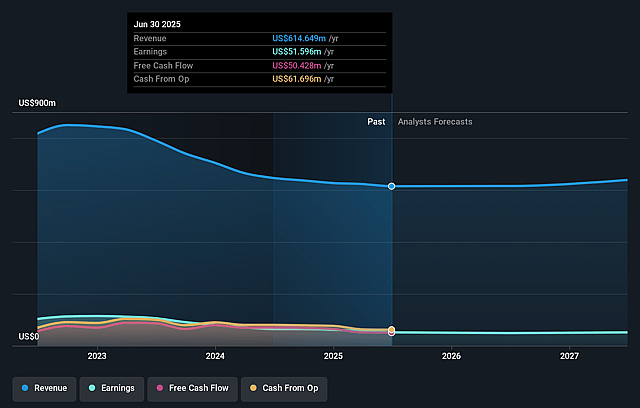

Ethan Allen Interiors Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ethan Allen Interiors's revenue will grow by 1.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.4% today to 7.8% in 3 years time.

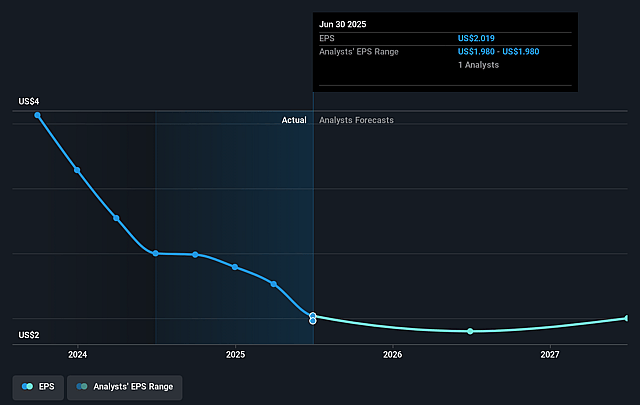

- Analysts expect earnings to reach $51.0 million (and earnings per share of $1.99) by about September 2028, down from $51.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.9x on those 2028 earnings, up from 14.5x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.63%, as per the Simply Wall St company report.

Ethan Allen Interiors Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ethan Allen's vertically integrated business model, with 80% of manufacturing in North America, has limited the impact of tariffs and global supply chain disruptions, supporting strong gross margins and operating margins that are likely to sustain earnings stability in the long term.

- The company's significant reduction in headcount and operating costs, along with its ongoing investment in technology and digital marketing, has improved operational efficiency and allowed for maintained or increased net margins even in a challenging demand environment, potentially supporting continued profitability.

- Customization now constitutes 80% of the product mix (up from 20% fifteen years ago), reducing excess inventory and clearance needs; this shift cushions gross margins and boosts cash flow resilience, counteracting pressures from fluctuating demand.

- Ethan Allen's robust balance sheet-with $196 million in cash, zero debt, and sustained cash generation-provides financial flexibility for reinvestment or increased shareholder returns, limiting downside risks to net income and supporting dividend sustainability.

- Recent improvements in retail order growth (+1.6% year-over-year in a tough quarter), combined with proactive store relocations and renovations, point to an adaptive business model that is capitalizing on changing consumer trends and positioning for long-term revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.0 for Ethan Allen Interiors based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $651.0 million, earnings will come to $51.0 million, and it would be trading on a PE ratio of 18.9x, assuming you use a discount rate of 8.6%.

- Given the current share price of $29.35, the analyst price target of $30.0 is 2.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.