Key Takeaways

- Strategic shift to higher-value portfolio aims to boost earnings by concentrating on core growth areas after divesting certain business units.

- Strong backlog and end-market demand drive potential revenue growth, while operational efficiencies may improve margins and shareholder returns.

- The strategic reliance on critical sectors and exposure to international markets pose risks to revenue stability amid potential U.S. federal spending changes and tax rate increases.

Catalysts

About Jacobs Solutions- Provides consulting, technical, engineering, scientific, and project delivery services for the government and private sectors in the United States, Europe, Canada, India, Asia, Australia, New Zealand, the Middle East, and Africa.

- The strategic shift to a simpler, higher-value, and higher-margin portfolio following the separation of the Critical Mission Solutions and Cyber & Intelligence businesses is expected to enhance overall earnings by focusing on core business areas with strong secular growth tailwinds.

- The increase in consolidated backlog by 23% year-on-year with a strong 1.67x book-to-bill ratio suggests confidence in future revenue growth as it indicates a robust pipeline of secured contracts potentially impacting revenue positively.

- Continued demand and growth in key end markets such as Water and Environmental, Life Sciences and Advanced Manufacturing, and Critical Infrastructure signal potential revenue growth due to increased spending in areas like recycled water infrastructure and semiconductors.

- The focus on operating efficiencies and a global delivery model may lead to improved net margins, as the company plans on leveraging cost controls and process improvements for margin expansion.

- The company's strong balance sheet and available cash flow for share repurchases and dividend growth indicate a focus on returning value to shareholders, which can potentially increase earnings per share over time.

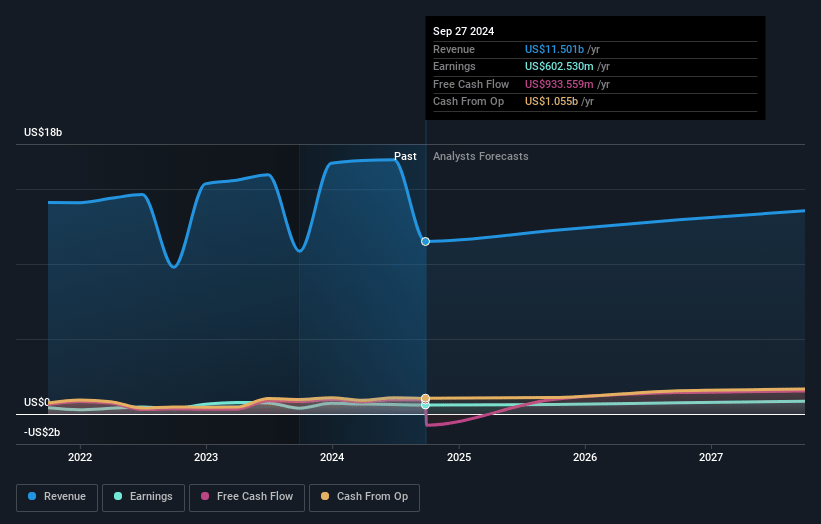

Jacobs Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Jacobs Solutions's revenue will grow by 5.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.2% today to 6.2% in 3 years time.

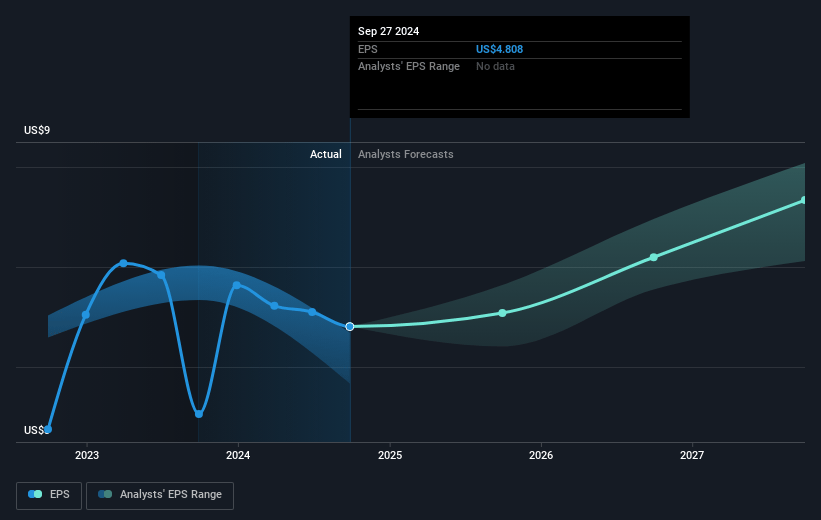

- Analysts expect earnings to reach $842.9 million (and earnings per share of $7.33) by about January 2028, up from $602.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $963.0 million in earnings, and the most bearish expecting $724 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.2x on those 2028 earnings, down from 28.3x today. This future PE is greater than the current PE for the US Professional Services industry at 25.1x.

- Analysts expect the number of shares outstanding to decline by 2.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.56%, as per the Simply Wall St company report.

Jacobs Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The recent separation transaction involving Critical Mission Solutions and Cyber & Intelligence businesses could lead to short-term restructuring costs and integration challenges, potentially impacting net margins and disrupting earnings stability.

- The company is facing uncertainties related to potential changes in U.S. federal spending, driven by political shifts and election outcomes, which could affect critical infrastructure projects and future revenue streams.

- Exposure to international markets like the U.K. and the Middle East involves risks due to economic fluctuations and budgetary constraints, potentially impacting revenue growth and financial results in these regions.

- The strategic reliance on significant bookings in Water and Environmental and Life Sciences could create dependencies on specific market sectors; any downturn in these sectors could lead to revenue volatility and impact margins.

- An increase in projected tax rates compared to previous years could dampen earnings growth and lead to lower net margins, affecting the overall financial health and profit outlook.

```

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $152.8 for Jacobs Solutions based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $176.0, and the most bearish reporting a price target of just $124.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $13.5 billion, earnings will come to $842.9 million, and it would be trading on a PE ratio of 25.2x, assuming you use a discount rate of 6.6%.

- Given the current share price of $137.39, the analyst's price target of $152.8 is 10.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives