Key Takeaways

- Strong performance in Forensic and Litigation Consulting, particularly in cybersecurity and sanctions, suggests potential revenue growth as regulatory scrutiny increases globally.

- Strategic talent investment and share repurchases aim to drive efficiencies and enhance shareholder value through EPS growth.

- Regulatory changes, employee departures, and competitive pressures are key challenges for FTI Consulting, potentially impacting revenue, earnings, and operating costs across several segments.

Catalysts

About FTI Consulting- Provides business advisory services to manage change, mitigate risk, and resolve disputes worldwide.

- The strong performance and brand-building work within the Forensic and Litigation Consulting (FLC) division, particularly in cybersecurity, anti-money laundering, and sanctions, suggest a potential for revenue growth as regulatory scrutiny increases globally and especially if policies in Washington bolster demand for these services.

- Despite short-term headwinds in the Economic Consulting segment due to departures, the aggressive investment in new talent and academic affiliations strengthens the long-term growth trajectory and competitive positioning of FTI, potentially improving revenue and earnings in the medium term.

- The restructuring segment is poised for growth as recent tariff-induced stress and high working capital needs may drive an increase in restructuring engagements, potentially boosting segment revenues and margins.

- Strategic Communications has started to regain growth momentum, and its role in complex regulatory and crisis communications, especially amidst geopolitical tensions and cybersecurity issues, positions it for future revenue stability and expansion.

- Continued strategic investments in talent across various high-demand areas, such as digital assets, AI, and healthcare, and the additional $400 million authorized for share repurchases, could drive efficiencies and enhance shareholder value through EPS growth.

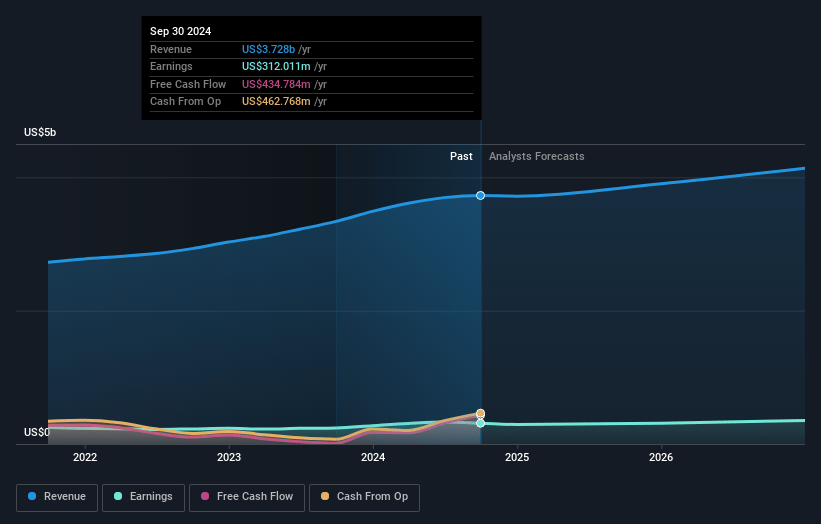

FTI Consulting Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming FTI Consulting's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.1% today to 8.3% in 3 years time.

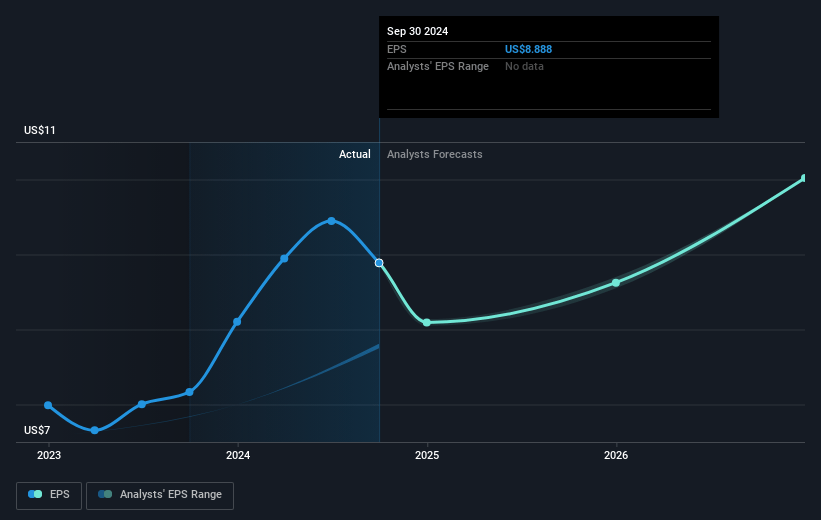

- Analysts expect earnings to reach $348.8 million (and earnings per share of $9.48) by about July 2028, up from $261.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.0x on those 2028 earnings, down from 21.2x today. This future PE is lower than the current PE for the US Professional Services industry at 23.7x.

- Analysts expect the number of shares outstanding to decline by 4.55% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.68%, as per the Simply Wall St company report.

FTI Consulting Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Regulatory shifts, particularly in the U.S. related to policies impacting areas like anti-consumer fraud, anti-money laundering, and export controls, could affect FTI Consulting's Forensic and Litigation Consulting segment, potentially reducing revenue from regulatory-driven projects.

- The economic consulting segment faces challenges due to employee departures and headcount declines, which may lead to a significant revenue and earnings impact, as revenue linked to departing employees may not fully rebound immediately.

- The technology segment is experiencing headwinds in M&A-related services like second requests because of reduced transaction volumes, potentially impacting revenue and earnings if the trend continues.

- Uncertainties in macroeconomic factors, including a possible recession and unpredictability in M&A and restructuring markets, can impact the company's Corporate Finance and Restructuring segment, affecting overall net margins and earnings.

- Increased competition and the need to offer competitive compensation to attract and retain talent, especially in response to recent disruptions, could lead to higher operating costs, putting pressure on net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $178.0 for FTI Consulting based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.2 billion, earnings will come to $348.8 million, and it would be trading on a PE ratio of 18.0x, assuming you use a discount rate of 6.7%.

- Given the current share price of $165.24, the analyst price target of $178.0 is 7.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.