Narratives are currently in beta

Key Takeaways

- The new incinerator and HEPACO acquisition are poised to relieve capacity issues and boost revenue through expanded capabilities and efficiencies.

- Strategic pricing adjustments and cost reduction measures aim to stabilize margins, enhance cash flow, and foster earnings growth.

- Weaker performance in key segments, increased costs, and integration challenges may pressure margins and cash flow without strategic management and offsetting growth.

Catalysts

About Clean Harbors- Provides environmental and industrial services in the United States and internationally.

- The completion and launch of the new state-of-the-art incinerator in Kimball, Nebraska will help to alleviate capacity constraints and meet the increased demand for hazardous waste disposal, potentially driving revenue and improving margins as the facility ramps up in the next 12 to 18 months.

- The acquisition and integration of HEPACO are expected to enhance Clean Harbors’ field services capabilities and create synergy opportunities, which could enhance revenue and drive margin improvement through economies of scale.

- The company’s efforts to adjust the pricing model in its re-refinery business, particularly in response to the volatile base oil market, aim to stabilize margins and improve cash flow efficiency moving forward.

- The anticipated regulation of PFAS provides an opportunity for Clean Harbors to benefit from increased demand for incineration and landfill solutions, potentially leading to revenue growth as the regulatory environment becomes more stringent.

- The emphasis on cost reduction strategies, including idling the California re-refinery and optimizing production costs, is expected to improve net margins and support stronger earnings growth in the future.

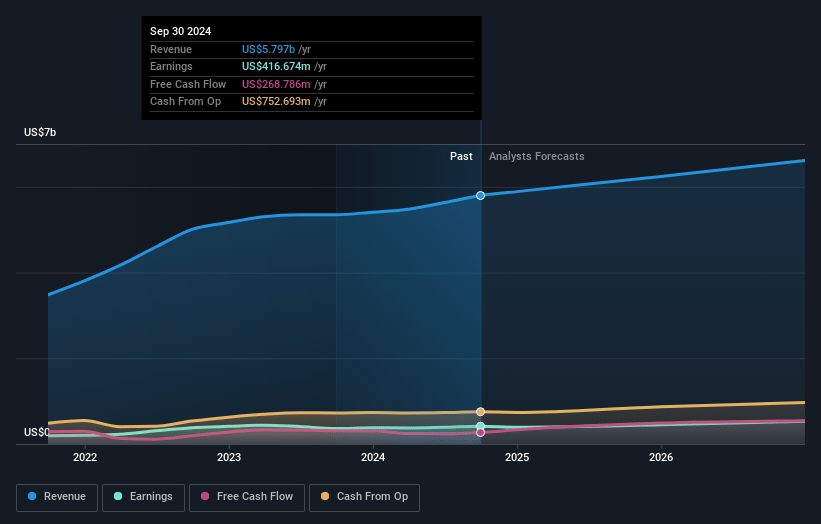

Clean Harbors Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Clean Harbors's revenue will grow by 5.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.2% today to 8.3% in 3 years time.

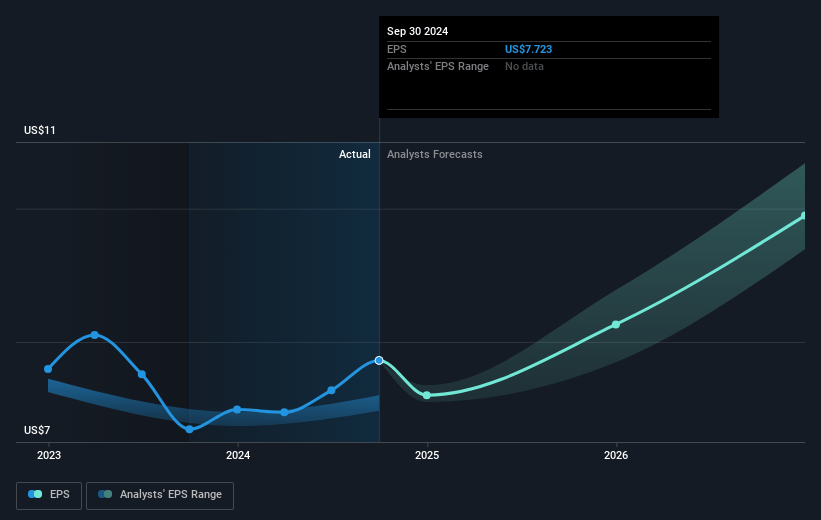

- Analysts expect earnings to reach $570.0 million (and earnings per share of $10.51) by about January 2028, up from $416.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.1x on those 2028 earnings, up from 30.5x today. This future PE is about the same as the current PE for the US Commercial Services industry at 32.1x.

- Analysts expect the number of shares outstanding to grow by 0.2% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.97%, as per the Simply Wall St company report.

Clean Harbors Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Industrial Services segment faced challenges due to a weaker-than-anticipated turnaround in refineries, affecting revenue and possibly net margins due to reduced activity and profitability in this part of the business.

- The Safety-Kleen Sustainability Solutions (SKSS) segment experienced softer-than-expected demand and declining pricing, particularly for base oil, which impacted quarterly earnings by about $11 million, signaling potential ongoing pressure on this segment's revenue.

- Increased corporate costs due to recent acquisitions, insurance, and healthcare expenses might pressure net margins if top-line growth doesn't adequately offset these expenses.

- Delays in accounts receivable collection, attributed partly to the integration of the HEPACO acquisition onto the billing system, could temporarily impact cash flow and contribute to increased working capital requirements.

- Oversupply of re-refined base oil and high inventory levels in SKSS, exacerbated by lower market demand, may continue to negatively impact earnings and cash flow if not adequately managed through cost structure adjustments and refining capacity idling.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $276.47 for Clean Harbors based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $325.0, and the most bearish reporting a price target of just $250.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.9 billion, earnings will come to $570.0 million, and it would be trading on a PE ratio of 32.1x, assuming you use a discount rate of 7.0%.

- Given the current share price of $236.07, the analyst's price target of $276.47 is 14.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives