Narratives are currently in beta

Key Takeaways

- Revenue growth anticipated in B&I and Technical Solutions segments due to U.S. market turnaround and microgrid expansion.

- Investments in AI and workforce tools expected to enhance sales, reduce costs, and boost net margins.

- Dependence on the macroeconomic environment and ongoing expenses could dampen ABM Industries' revenue and margins amid potential financial volatility and growth risks.

Catalysts

About ABM Industries- Through its subsidiaries, engages in the provision of integrated facility, infrastructure, and mobility solutions in the United States and internationally.

- ABM Industries anticipates revenue growth in the B&I segment due to an expected turnaround in the U.S. commercial real estate market, driven by increased leasing activity and stabilizing office attendance. This could positively impact overall revenue and earnings as the segment returns to growth.

- The Technical Solutions segment is poised for continued strong growth in 2025, driven by a robust backlog exceeding $500 million and significant market opportunities in the U.S. microgrid sector, which is expected to grow to $50 billion over the next decade. This should contribute to higher revenue and improved earnings.

- The Aviation segment is expected to benefit from ongoing investments in airport infrastructure and a forecasted 5.6% growth in North American air passenger traffic in 2025. With strong new business wins and ABM's differentiated service offerings, this could drive revenue expansion and profitability.

- ABM's introduction of a workforce productivity optimization tool has already reduced labor as a percent of revenue by nearly 1% in the fourth quarter. As these tools are more broadly implemented, they may lead to lower costs and improved net margins across the company.

- The company's strategic investments in artificial intelligence are anticipated to provide revenue growth opportunities and improved operational efficiencies, particularly by enhancing sales processes and customer service, ultimately impacting earnings positively.

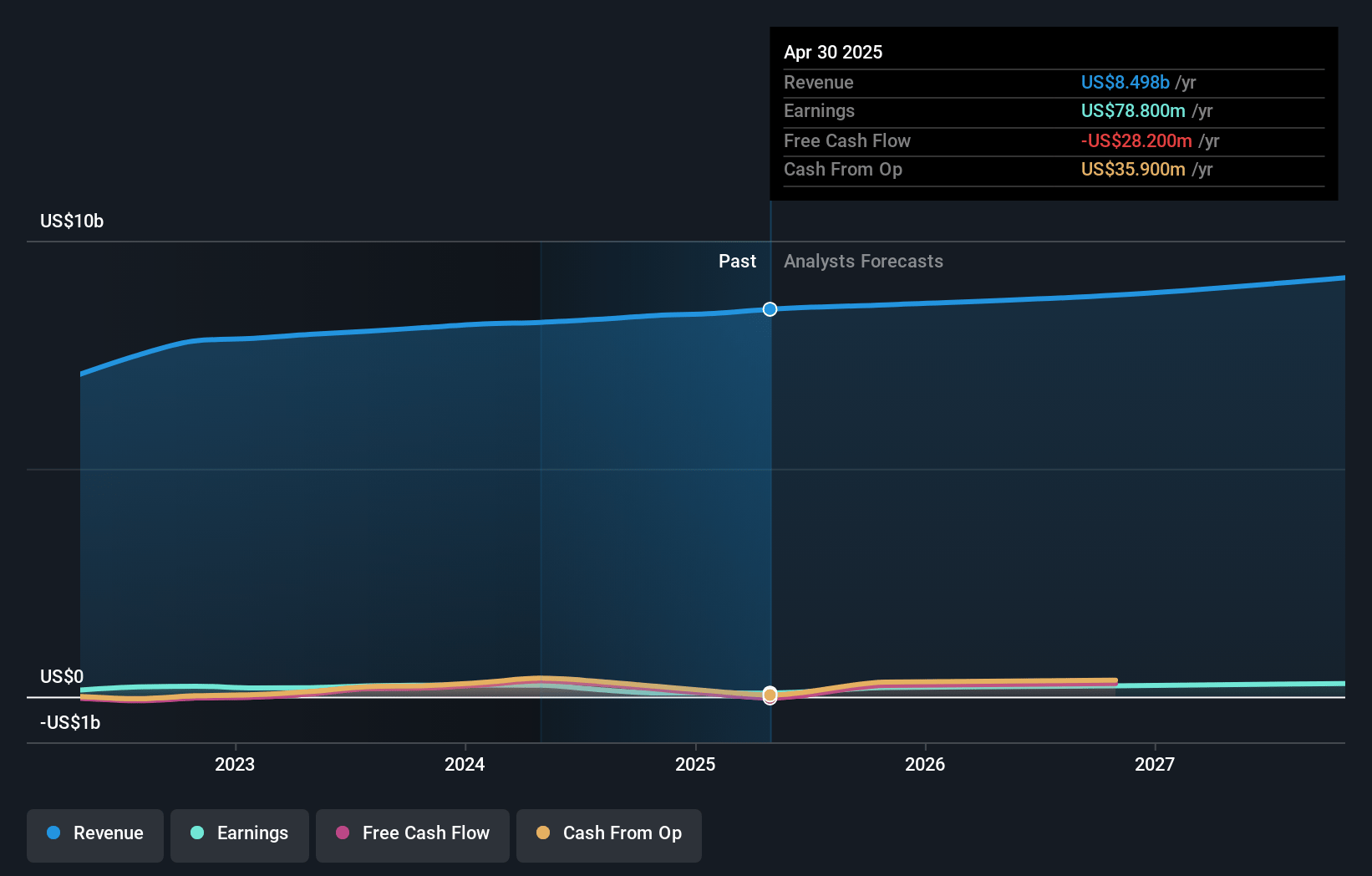

ABM Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ABM Industries's revenue will grow by 1.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.9% today to 3.1% in 3 years time.

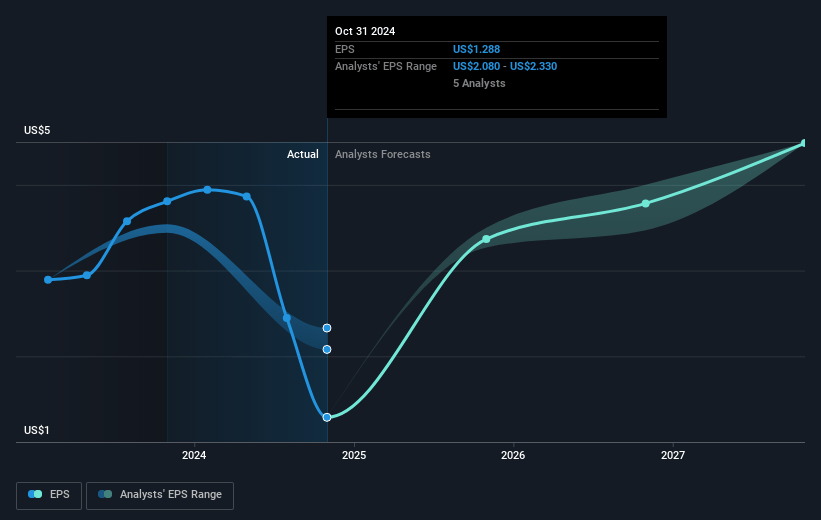

- Analysts expect earnings to reach $263.5 million (and earnings per share of $4.4) by about December 2027, up from $155.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.0x on those 2027 earnings, down from 22.1x today. This future PE is lower than the current PE for the US Commercial Services industry at 31.0x.

- Analysts expect the number of shares outstanding to decline by 1.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.26%, as per the Simply Wall St company report.

ABM Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The projected growth in ABM's Manufacturing & Distribution (M&D) segment hinges on the rebalancing with a large e-commerce client, which could face headwinds if these forecasts are overly optimistic, potentially impacting revenue and profit margins.

- The net loss in the fourth quarter due to adjustments and charges demonstrates potential financial volatility; recurring issues like these could harm earnings stability and investor confidence.

- While the Aviation segment is currently performing well, longer sales cycles and moderated market exuberance pose a risk of slowing growth, impacting revenue growth potential.

- The dependence on the macroeconomic environment and commercial real estate markets for B&I and other segments reflects vulnerability to economic downturns, which could dampen revenue and profitability.

- With ongoing expenses from the ELEVATE program and transformation initiatives, there is a risk that anticipated savings or benefits may not materialize as expected, which could affect net margins and free cash flow outcomes.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $57.83 for ABM Industries based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $8.6 billion, earnings will come to $263.5 million, and it would be trading on a PE ratio of 16.0x, assuming you use a discount rate of 7.3%.

- Given the current share price of $54.91, the analyst's price target of $57.83 is 5.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives