Narratives are currently in beta

Key Takeaways

- Focus on specialized staffing and outcome-based models aims to stabilize revenue and enhance margins amid stabilizing market demand.

- Strategic acquisitions and leveraging advanced technology like AI could improve efficiency and bolster earnings.

- Ongoing market uncertainties, staffing pressures, and integration costs from acquisitions could negatively impact Kelly Services' revenue growth and profitability.

Catalysts

About Kelly Services- Provides workforce solutions to various industries.

- Kelly Services is focusing on higher-margin, more resilient solutions, such as specialized education and therapy staffing, which can enhance revenue stability and potentially increase net margins.

- The company's strategic shift towards a higher-margin outcome-based model in segments like SETT and P&I suggests potential for improved earnings as demand in these markets stabilizes.

- Kelly is leveraging its advanced Helix technology platform and upgrading it with AI-enabled market intelligence, which could drive efficiencies and improve net margins.

- The acquisition of Motion Recruitment Partners and potential synergies from this integration are expected to enhance revenue and cost efficiency, positively impacting earnings.

- Kelly's continued investment in expanding capacity in growth markets and developing a pipeline of high-quality acquisition targets suggests ongoing efforts to bolster revenue and potentially improve net margins.

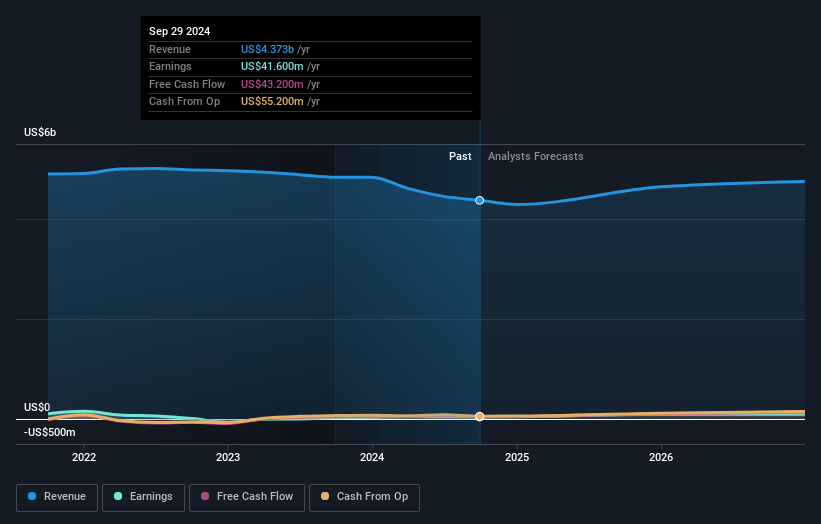

Kelly Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kelly Services's revenue will grow by 4.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.0% today to 2.8% in 3 years time.

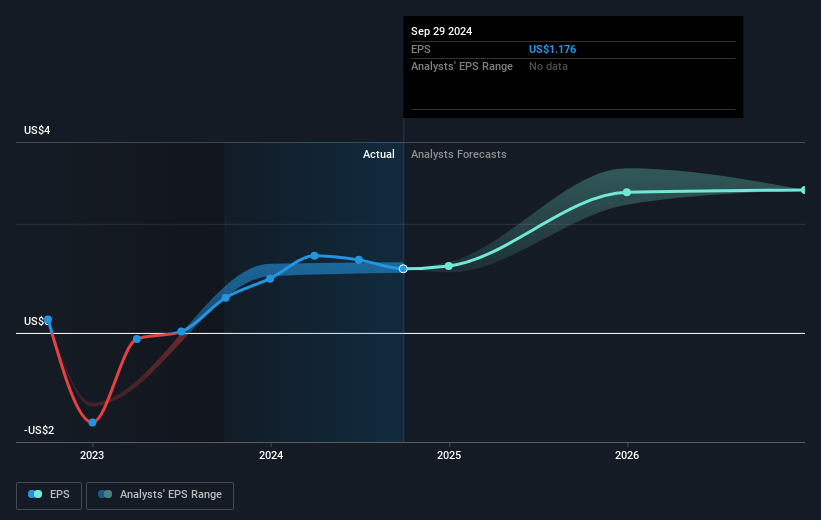

- Analysts expect earnings to reach $138.9 million (and earnings per share of $3.79) by about January 2028, up from $41.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.4x on those 2028 earnings, down from 12.3x today. This future PE is lower than the current PE for the US Professional Services industry at 25.1x.

- Analysts expect the number of shares outstanding to grow by 0.97% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.3%, as per the Simply Wall St company report.

Kelly Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Kelly Services faces ongoing uncertain market conditions, particularly in the SETT segment, which has experienced a deceleration in demand that could impact overall revenue growth prospects.

- The company is dealing with continued pressure in the staffing and recruiting sectors, with large enterprises deferring hiring, managing headcount through attrition, and not backfilling roles, which could negatively affect revenue generation.

- The integration of Motion Recruitment Partners, while strategic, involves significant costs related to technology integration and other expenses, potentially impacting net margins in the short term.

- Kelly's gross profit rate has been under pressure due to a changing business mix towards lower-margin offerings, which could negatively affect net margins and profitability if not balanced by higher margin operations.

- The company's recent acquisition includes additional interest expenses, adding financial obligations that could constrain earnings and diminish financial flexibility if not offset by increased revenue and profitability from the acquisition.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $26.33 for Kelly Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.9 billion, earnings will come to $138.9 million, and it would be trading on a PE ratio of 8.4x, assuming you use a discount rate of 7.3%.

- Given the current share price of $14.36, the analyst's price target of $26.33 is 45.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives