Key Takeaways

- EXL's data and AI focus is set to drive growth and revenue through improved operational analytics, new client expansions, and industry-specific AI capabilities.

- Strategic partnerships with major tech firms enhance AI innovation, positioning EXL as a strategic partner with improved earnings potential through proprietary AI solutions.

- Heavy investments in AI and digital solutions might pressure profit margins, with success reliant on client readiness and effective global market expansion.

Catalysts

About ExlService Holdings- Operates as a data analytics, and digital operations and solutions company in the United States and internationally.

- EXL's focus on accelerating their execution of data and AI strategy is expected to drive long-term growth by capturing a greater share of the growing AI market and improving operational analytics, data engineering, and AI capabilities specific to their chosen industries. This change is anticipated to boost revenue through new client wins and expansions with existing clients.

- The implementation of a new operating model with industry market units and strategic growth units is designed to deepen industry expertise and foster greater collaboration, allowing EXL to swiftly develop and deploy innovative data and AI solutions. This is likely to impact their net margins by enabling more efficient resource utilization and scalable infrastructure deployment.

- EXL's pivot towards developing and scaling proprietary AI solutions and their partnerships with major tech firms like NVIDIA, Databricks, AWS, Microsoft, and Google are expected to provide higher value to clients and position EXL as a strategic partner. This strategy should improve their earnings by leveraging these partnerships for AI innovation and deployment.

- The launch of EXLerate.AI, a platform designed to integrate AI agents into business workflows, is anticipated to lead to greater efficiency, increased accuracy, and scalability across operations. This is likely to enhance revenue growth by embedding AI solutions more deeply into client operations.

- EXL's planned shift in financial reporting segments starting in 2025 will provide greater transparency in data and AI revenue, potentially leading to more dynamic pricing models and improved revenue forecasts, enhancing overall earnings potential through more targeted sales strategies.

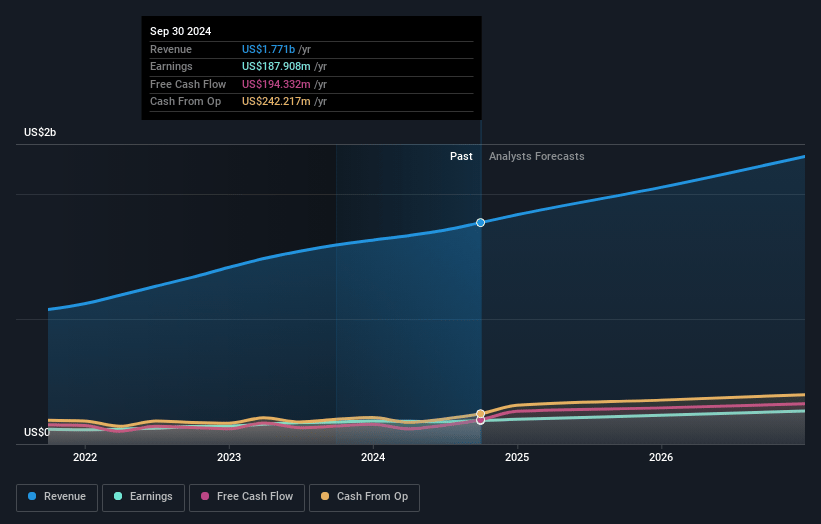

ExlService Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ExlService Holdings's revenue will grow by 12.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.8% today to 11.9% in 3 years time.

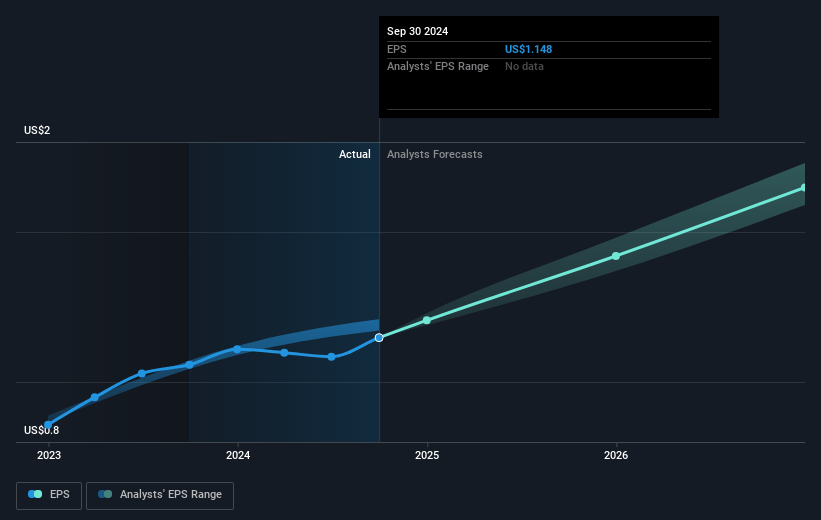

- Analysts expect earnings to reach $311.8 million (and earnings per share of $1.9) by about March 2028, up from $198.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.4x on those 2028 earnings, down from 38.2x today. This future PE is greater than the current PE for the US Professional Services industry at 21.7x.

- Analysts expect the number of shares outstanding to decline by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.64%, as per the Simply Wall St company report.

ExlService Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The shift in the IT spend towards AI and the need to embed AI into client workflows might present challenges if clients are not ready with modernized infrastructure or data assets, impacting EXL's ability to drive revenue growth through these services.

- The integration of analytics into the industry verticals and the new operating model might lead to potential execution risks in cross-selling and delivering integrated deals, which could affect revenue growth targets.

- Heavy investments in R&D, AI, and digital solutions may exert pressure on profit margins. If these investments do not yield the anticipated returns, they could negatively impact net margins.

- The expansion into international markets, while promising, involves risks related to execution, competition, and local market conditions, which may affect revenue growth in these regions.

- The reliance on partnerships with major tech companies like NVIDIA, AWS, Microsoft, and Google for AI infrastructure could expose EXL to competitive risks and cost fluctuations, potentially affecting operating margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $55.0 for ExlService Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.6 billion, earnings will come to $311.8 million, and it would be trading on a PE ratio of 34.4x, assuming you use a discount rate of 6.6%.

- Given the current share price of $46.64, the analyst price target of $55.0 is 15.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.