Key Takeaways

- Strategic adjustments and a strong opportunity pipeline position DLH for revenue and earnings growth through large contracts and high-margin tech solutions.

- Focus on digital transformation and cybersecurity can expand DLH's market, boosting net margins with efficient, in-demand services.

- DLH faces revenue and profitability challenges from contract changes and strategic shifts amid uncertain government procurement and a changing federal landscape.

Catalysts

About DLH Holdings- Provides technology-enabled business process outsourcing, program management solutions, and public health research and analytics services in the United States.

- The recent $76 million contract with the United States Navy is a key growth driver, reflecting DLH's ability to compete for and win large contracts, which is expected to positively impact revenue.

- A robust pipeline of opportunities valued at over $4 billion positions DLH well for future expansion, potentially leading to improved operating performance and increased revenue.

- DLH has made strategic adjustments to its business development capabilities, allowing for more organic growth opportunities, which should enhance earnings through higher-margin technology solutions.

- The transition within the government procurement landscape offers DLH a chance to capitalize on changing priorities, potentially increasing their addressable market and revenue growth.

- DLH’s focus on digital transformation, cybersecurity, and scientific capabilities enables them to offer high-tech solutions, which are in demand and can improve net margins by providing more efficient and cost-effective services.

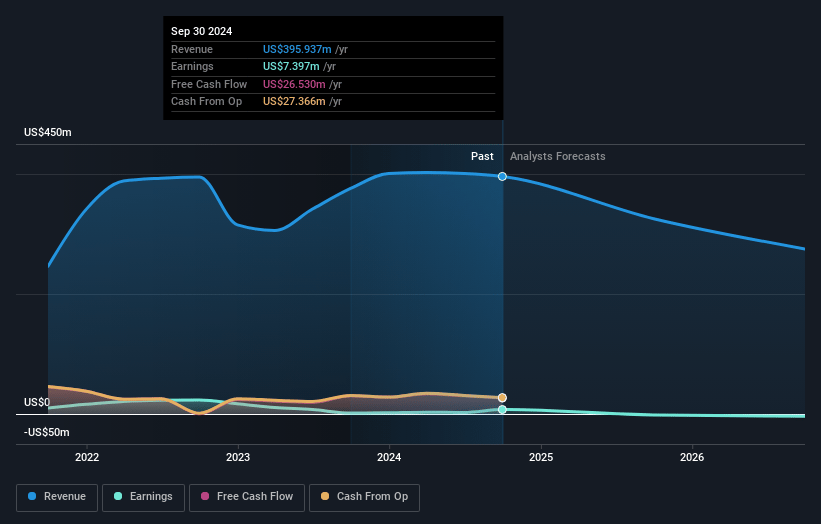

DLH Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DLH Holdings's revenue will decrease by -17.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 1.9% today to 0.5% in 3 years time.

- Analysts expect earnings to reach $1.2 million (and earnings per share of $0.08) by about January 2028, down from $7.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 224.1x on those 2028 earnings, up from 14.8x today. This future PE is greater than the current PE for the US Professional Services industry at 25.1x.

- Analysts expect the number of shares outstanding to grow by 0.84% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.95%, as per the Simply Wall St company report.

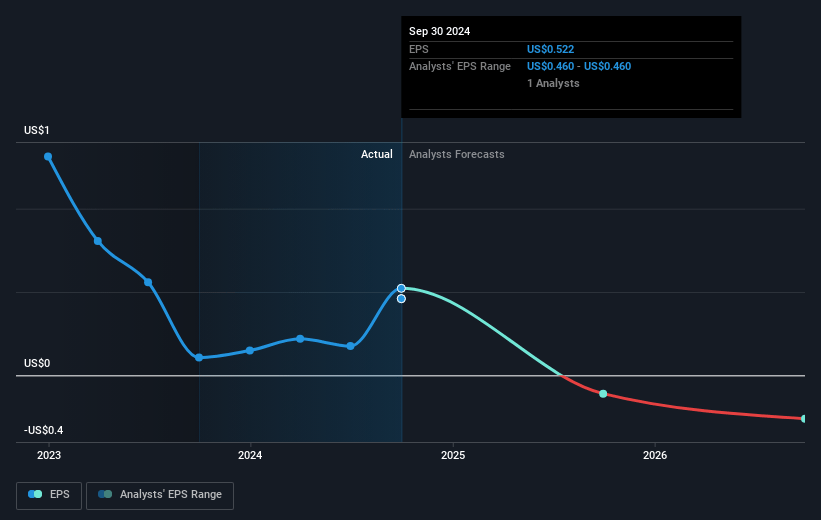

DLH Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- DLH faces headwinds due to the conversion of contracts to small business set-aside programs, which could continue impacting revenue and profitability as the company transitions certain contracts away from its portfolio.

- The success of DLH in pursuing its $4 billion new business pipeline is not guaranteed, given uncertainties related to the government procurement processes and potential delays, which could affect future revenue growth and operating performance.

- The company's decisions to not pursue certain VA (Veterans Affairs) contract bids and instead participate selectively as a subcontractor could reduce its revenue from these sources, impacting DLH's overall revenue performance.

- DLH's need to continually adjust in response to a potentially reshaped federal procurement landscape due to the changing administration and other political factors presents strategic risks that could hinder revenue targets or lead to additional costs.

- The company's strategy to achieve significant organic growth through increased investments in strategic solutioning and business development could compress EBITDA margins in the near term, which may affect overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.0 for DLH Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $224.9 million, earnings will come to $1.2 million, and it would be trading on a PE ratio of 224.1x, assuming you use a discount rate of 8.9%.

- Given the current share price of $7.61, the analyst's price target of $15.0 is 49.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives