Key Takeaways

- BBSI's strong growth in new client acquisition and high retention will positively impact future revenue, driven by expansion into new markets.

- Strategic investments in sales diversification and partnerships are expected to enhance sales efficiency and convert prospects into clients, boosting revenue and earnings.

- Competitive pressures and below-average client hiring may hinder Barrett Business Services' revenue growth, along with regional market challenges and strategic shifts affecting operations.

Catalysts

About Barrett Business Services- Provides business management solutions for small and mid-sized companies in the United States.

- BBSI is experiencing strong controllable growth with the addition of 4,600 worksite employees, driven by new client acquisitions and high client retention, which will positively impact future revenue.

- The successful expansion into new markets with an asset-light model and development of 21 new market managers is expected to further increase client acquisition and support, boosting revenue growth.

- The roll-out of BBSI Benefits, including the strategic partnership with Kaiser Permanente, is anticipated to be accretive to earnings in 2025, as more clients are added and the firm achieves operational scale.

- Continued strong performance in the workers' compensation program, with favorable claim frequency and development, is likely to support stable profitability and benefit net margins.

- Strategic investments in sales pipeline diversification (SEO, SEM, direct efforts) and increased referral partnerships are expected to enhance sales efficiency and convert higher numbers of prospects into clients, positively impacting revenue and earnings.

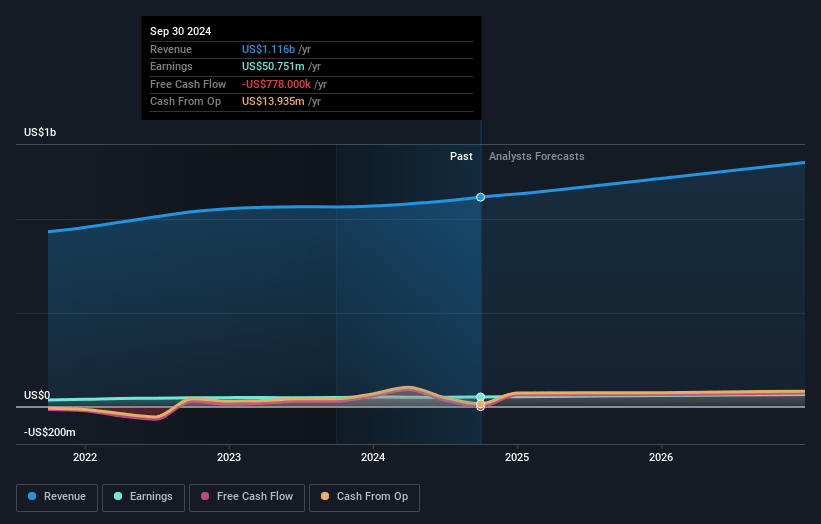

Barrett Business Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Barrett Business Services's revenue will grow by 6.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.5% today to 5.0% in 3 years time.

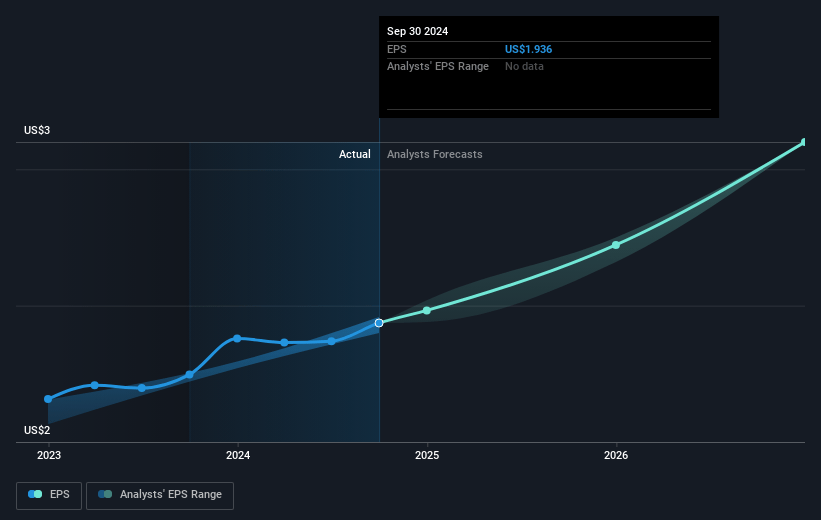

- Analysts expect earnings to reach $68.3 million (and earnings per share of $2.74) by about January 2028, up from $50.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.4x on those 2028 earnings, down from 22.2x today. This future PE is lower than the current PE for the US Professional Services industry at 25.1x.

- Analysts expect the number of shares outstanding to decline by 1.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.3%, as per the Simply Wall St company report.

Barrett Business Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The client's workforce hiring is below historical averages and remains a significant driver for growth, as more hiring can directly increase gross billings and revenue. If client hiring continues to underperform, revenue growth could be constrained.

- Staffing business has seen a 2% decline due to strategic shifts and client repricing, impacting top-line revenue despite efforts to stabilize the business.

- The Pacific Northwest region experienced a decline in growth, which may indicate regional market challenges that could affect overall revenue growth if similar trends emerge in other areas.

- Although the company has removed underwriting risk from their health and workers’ compensation insurance offerings, it still faces competitive pressures in the PEO market, which could affect client retention and revenue stability.

- With an increasingly competitive landscape in the PEO industry, maintaining high client retention and continued growth in gross billings may become challenging, impacting both revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $46.0 for Barrett Business Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.4 billion, earnings will come to $68.3 million, and it would be trading on a PE ratio of 19.4x, assuming you use a discount rate of 6.3%.

- Given the current share price of $43.49, the analyst's price target of $46.0 is 5.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives