Key Takeaways

- Transition to A2L products and digital platform adoption could enhance revenue growth and operational efficiency, boosting future sales and profitability.

- Strong financial position and continuous acquisitions support long-term growth, market share gains, and improved net margins through diversification and scalability.

- Challenges in regulatory compliance, pricing strategies, and customer focus may temporarily impact sales growth, profit margins, and market share goals for Watsco.

Catalysts

About Watsco- Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

- Transition to next-generation A2L products is underway, creating an opportunity to upgrade existing equipment with more efficient, environmentally friendly systems, which is expected to influence 50% to 60% of sales. This could drive future revenue growth.

- Expansion of technology platforms, including a community of over 64,000 users on Watsco mobile apps and a 16% increase in e-commerce sales, suggests an increase in digital adoption expected to bolster revenue and operating efficiency.

- OnCall Air's digital sales platform presented proposals generating $1.5 billion in gross merchandise value, with a 25% increase. This platform enables better sales performance, potentially boosting revenue and net margins through higher-margin deals.

- Watsco's strong financial position allows it to invest in significant growth opportunities and gain market share, suggesting long-term revenue growth and improved earnings potential.

- Continuous acquisitions, with the 70th since 1989 completed recently, highlight a strategy for growth and diversification, expected to provide revenue enhancement and potentially better net margins through economies of scale.

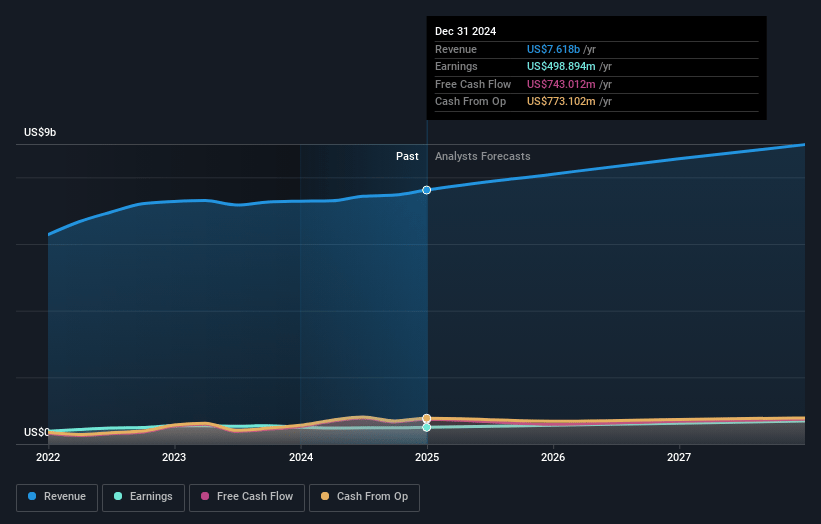

Watsco Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Watsco's revenue will grow by 5.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.5% today to 7.7% in 3 years time.

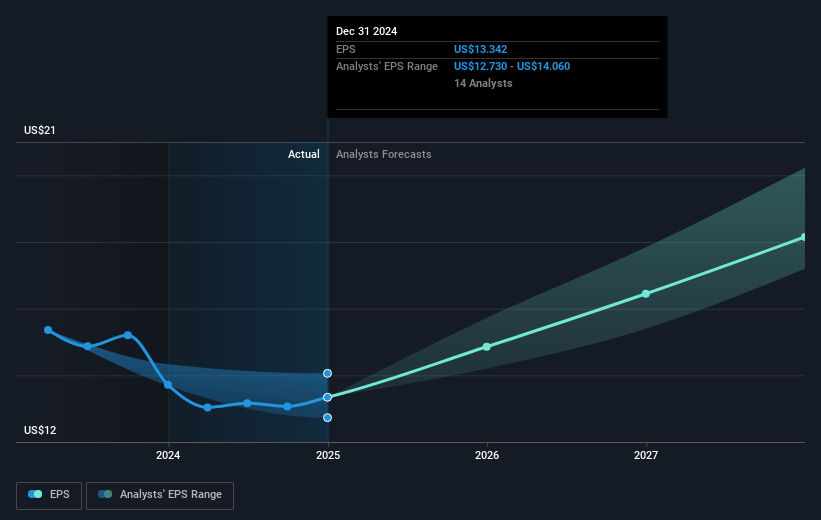

- Analysts expect earnings to reach $696.2 million (and earnings per share of $18.31) by about March 2028, up from $498.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.8x on those 2028 earnings, down from 38.8x today. This future PE is greater than the current PE for the US Trade Distributors industry at 18.3x.

- Analysts expect the number of shares outstanding to grow by 0.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.26%, as per the Simply Wall St company report.

Watsco Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The transition from 410A to A2L products could face regulatory, logistical, or market acceptance challenges, potentially causing a temporary dip in sales and affecting revenue.

- Increased pricing due to tariffs, particularly on products sourced from China or Mexico, may lead to higher costs that could either compress margins or reduce sales if passed on to consumers, impacting net margins.

- Watsco's pricing strategies with new A2L products might not immediately lead to increased gross margins due to the complexity and cost of the new technology, potentially affecting earnings growth in the short term.

- Heavy reliance on technological implementation and training for both their workforce and their customers may not yield the anticipated competitive advantages in time, which could impact their market share and revenue projections.

- The assumption that incremental growth will come from entirely new customer acquisition and a lack of focus on retaining and expanding current customer revenues might pose a risk to achieving the desired revenue and profitability targets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $486.647 for Watsco based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $560.0, and the most bearish reporting a price target of just $330.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $9.0 billion, earnings will come to $696.2 million, and it would be trading on a PE ratio of 32.8x, assuming you use a discount rate of 7.3%.

- Given the current share price of $512.94, the analyst price target of $486.65 is 5.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives