Key Takeaways

- Transitioning to a build, own, and operate strategy enhances revenue predictability and margins, supporting earnings growth and stability.

- Increasing contract backlog indicates strong demand and potential for future revenue growth, particularly in the Australian and U.S. markets.

- Energy Vault faces revenue challenges due to declining battery prices, project timing, and market volatility, impacting financial stability and short-term profitability.

Catalysts

About Energy Vault Holdings- Develops and sells energy storage solutions.

- Energy Vault's transition to a build, own and operate strategy allows for capturing more predictable and higher-margin revenue streams from energy infrastructure ownership, which can enhance net margins and earnings over time.

- The 14-year LTESA with guaranteed minimum revenues and the potential for higher merchant revenues provides a stable and creditworthy revenue base, potentially driving consistent and significant revenue growth.

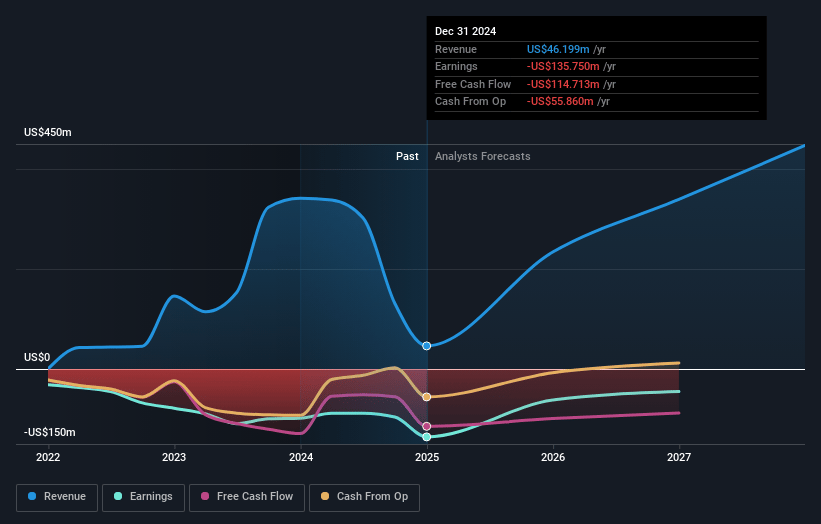

- The company's growing contract backlog, which increased by 90% quarter-over-quarter to $660 million, suggests robust future revenue growth, driven by strong demand in Australia and the United States.

- Strategic focus and optimization of project financing for owned assets, such as Calistoga, should effectively manage cash flow and strengthen the balance sheet, potentially minimizing equity dilution while enhancing earnings visibility.

- Declining battery prices and successful project execution could lead to improved gross margins, offering potential for higher profitability as Energy Vault leverages global market opportunities, including in non-tariff-sensitive regions like Australia.

Energy Vault Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Energy Vault Holdings's revenue will grow by 113.1% annually over the next 3 years.

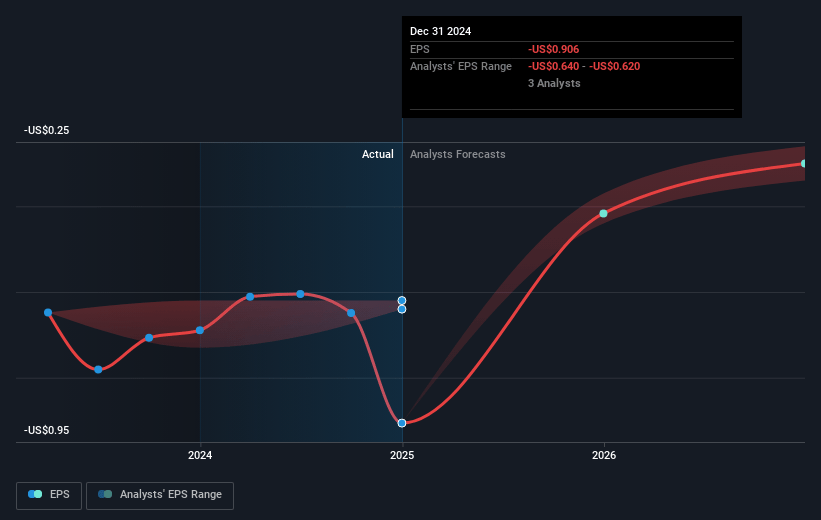

- Analysts are not forecasting that Energy Vault Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Energy Vault Holdings's profit margin will increase from -293.8% to the average US Electrical industry of 10.5% in 3 years.

- If Energy Vault Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $46.8 million (and earnings per share of $0.27) by about May 2028, up from $-135.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.4x on those 2028 earnings, up from -0.8x today. This future PE is lower than the current PE for the US Electrical industry at 22.8x.

- Analysts expect the number of shares outstanding to grow by 3.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

Energy Vault Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Energy Vault's revenue was slightly below expectations in 2024 due to rapidly declining battery prices and timing issues with project starts, which could affect future earnings if such trends continue.

- The shift to owning energy storage assets led to $100 million in projects retained on the company's balance sheet instead of recognizing revenue immediately, impacting short-term revenue expectations.

- The company has experienced gross margin fluctuations due to external factors, such as a supplier bankruptcy, which could lead to uncertain net margins and financial stability.

- Energy Vault's reliance on new project financing and potential delays in cash flow from these projects pose risks to timely and consistent revenue and earnings.

- The volatile market conditions, including tariff impacts on lithium-ion prices, could affect project pricing and profitability, potentially influencing net margins negatively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $1.625 for Energy Vault Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $2.5, and the most bearish reporting a price target of just $0.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $447.1 million, earnings will come to $46.8 million, and it would be trading on a PE ratio of 7.4x, assuming you use a discount rate of 7.6%.

- Given the current share price of $0.74, the analyst price target of $1.62 is 54.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.