Key Takeaways

- Simplifying the capital structure and reducing debt through asset sales and buybacks should improve profitability, margins, and earnings per share.

- Strategic growth initiatives in utilities and various sectors are expected to drive strong revenue growth through increased bookings and investments.

- Internal control weaknesses, declining sales, and dependency on volatile markets pose risks to MRC Global's revenue growth and profitability.

Catalysts

About MRC Global- Through its subsidiaries, distributes pipes, valves, fittings, and other infrastructure products and services in the United States, Canada, and internationally.

- The simplification of MRC Global's capital structure by repurchasing convertible preferred shares is expected to be accretive to both cash generation and earnings in 2025 and beyond, positively impacting net margins and EPS.

- The sale of the Canada business and reinvestment of proceeds to reduce debt should improve profitability and margins, enhancing the company's overall financial health and net earnings.

- A $125 million share buyback program reflects confidence in future performance and the strengthened balance sheet, potentially increasing EPS as shares are repurchased and earnings are distributed across fewer shares.

- Growth in gas utilities, supported by improving fundamentals and increased capital expenditures over the next five years, is expected to drive stronger revenue growth, particularly as customer investment in infrastructure is bolstered.

- Strategic supply agreements and new growth initiatives in sectors such as chemicals, mining, and data centers are anticipated to contribute to higher revenue growth, with increased bookings and backlog indicating future revenue increases.

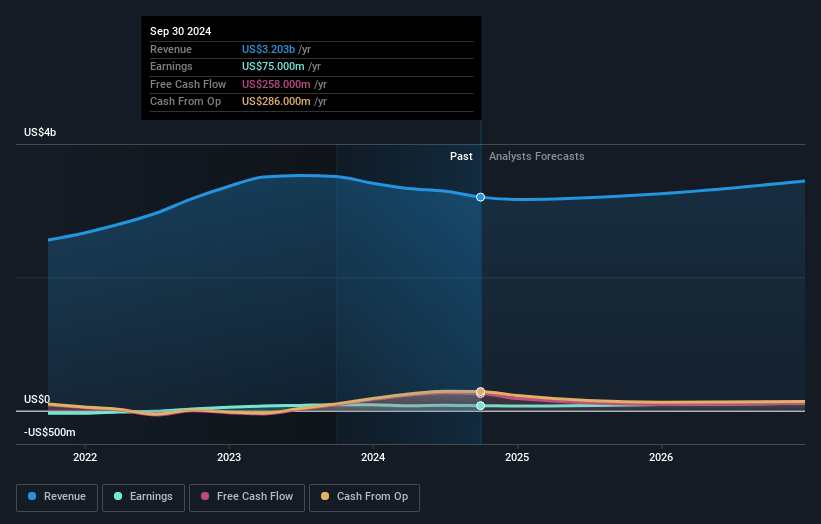

MRC Global Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MRC Global's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.6% today to 3.5% in 3 years time.

- Analysts expect earnings to reach $118.2 million (and earnings per share of $1.51) by about March 2028, up from $49.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.7x on those 2028 earnings, down from 21.3x today. This future PE is lower than the current PE for the US Trade Distributors industry at 19.0x.

- Analysts expect the number of shares outstanding to grow by 1.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.56%, as per the Simply Wall St company report.

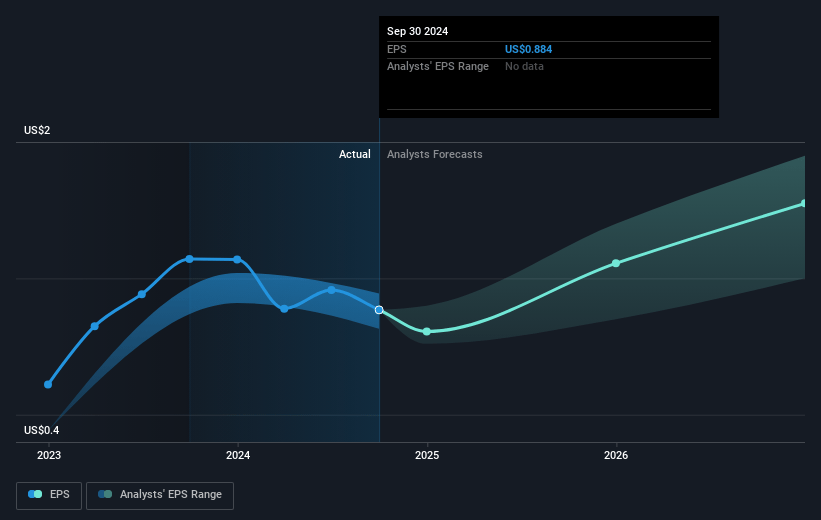

MRC Global Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The discovery of inventory process noncompliance at two North American locations and the need for additional physical inventory counts highlight potential internal control weaknesses, which could impact future financial reporting accuracy and overall earnings.

- A sequential 14% decline in total company sales in the fourth quarter and a 10% decrease compared to the same quarter last year indicate potential difficulties in sustaining revenue growth if these trends continue into the future.

- Lower project activity due to timing delays and customer pullbacks, particularly in the U.S. segment, suggest that revenue may remain volatile and exposed to cyclical and external factors, impacting overall revenue stability.

- Dependency on market conditions such as tariffs and inflation for price increases may create uncertainty in maintaining gross margins, where unexpected changes could adversely affect profitability and earnings.

- High reliance on a few market sectors, such as gas utilities, for growth could pose a risk if expected increases in capital expenditures do not materialize, affecting revenue projections and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $16.25 for MRC Global based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.4 billion, earnings will come to $118.2 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 8.6%.

- Given the current share price of $12.12, the analyst price target of $16.25 is 25.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.