Key Takeaways

- Hubbell's segments are experiencing strong organic growth and improving margins supported by demand in data centers and grid modernization.

- Actions tackling cost inflation are anticipated to stabilize earnings, while investments in acquisitions should sustain revenue growth and EPS expansion.

- Hubbell's profitability is threatened by tariff risks, cost inflation, and macroeconomic uncertainty, necessitating effective pricing strategies to maintain net margins.

Catalysts

About Hubbell- Designs, manufactures, and sells electrical and utility solutions in the United States and internationally.

- Hubbell's Electrical Solutions segment is achieving mid-single-digit organic growth and improved operating margins, bolstered by strong demand in data centers and continuing efforts in business simplification, which should support long-term margin expansion. This is expected to positively impact revenue and net margins.

- The Utility Solutions segment is experiencing organic growth resurgence, particularly in grid infrastructure, supported by strong transmission and substation markets due to increasing grid modernization and electrification. This growth trend should drive higher future revenues.

- Hubbell is implementing pricing and productivity actions to combat cost inflation from raw materials and tariffs, aiming for neutral impact in 2025. Successfully offsetting these costs is expected to stabilize earnings and improve net margins in the latter part of the year.

- Significant order growth in grid infrastructure, driven by broad market strength and favorable end-market dynamics, suggests a strong future revenue stream as the company moves beyond a period of inventory normalization.

- Continued investment in acquisitions and focus on market-leading positions in utility and electrical markets, underpinned by secular growth trends, are expected to sustain long-term revenue growth and EPS expansion.

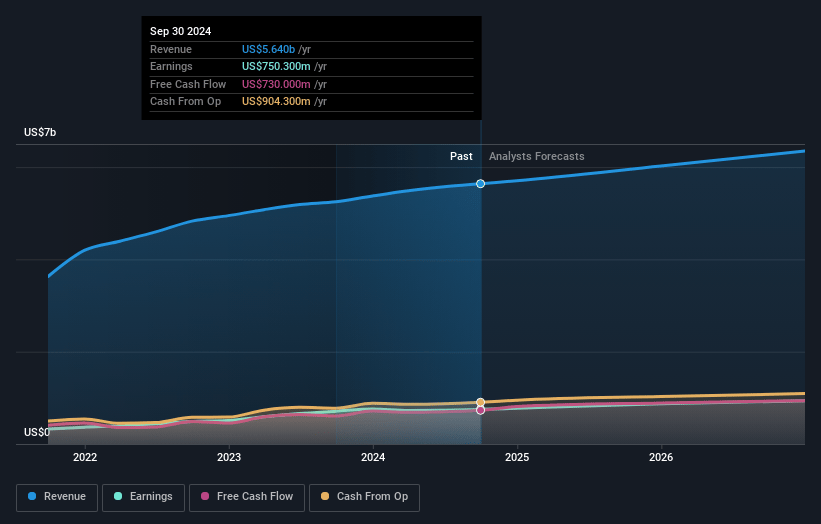

Hubbell Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Hubbell's revenue will grow by 5.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.3% today to 15.6% in 3 years time.

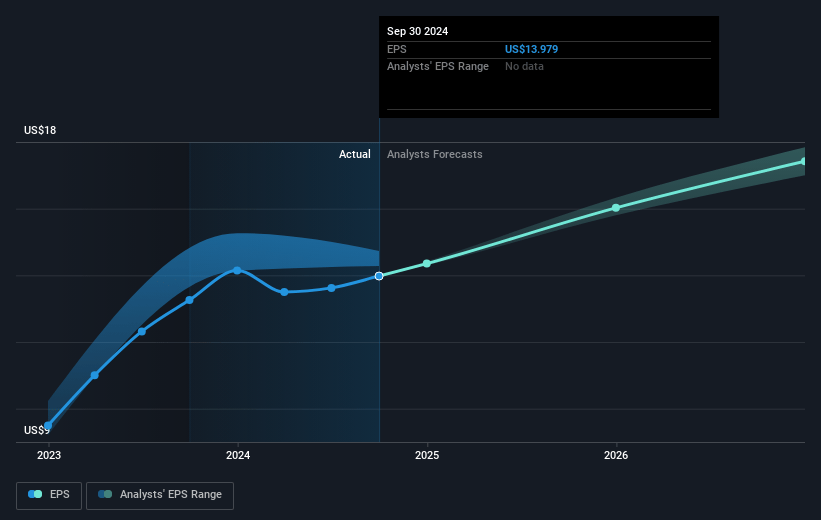

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $19.36) by about May 2028, up from $798.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.7x on those 2028 earnings, up from 23.3x today. This future PE is greater than the current PE for the US Electrical industry at 21.9x.

- Analysts expect the number of shares outstanding to decline by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.86%, as per the Simply Wall St company report.

Hubbell Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Hubbell is facing increased cost inflation from higher raw material prices and newly implemented tariffs, which could negatively impact net margins if not fully offset by pricing actions.

- Grid automation sales were down due to challenging prior year comparisons, and a continued decline could affect future revenue growth in this segment.

- The reliance on components sourced from China exposes Hubbell to tariff risks and potential supply chain disruptions, which might impact earnings if not managed well.

- The recent macroeconomic uncertainty and potential recession may dampen demand, leading to lower sales volumes and affecting overall revenue and earnings.

- There is execution risk associated with effectively implementing pricing strategies to fully mitigate tariff and cost increases, which could impact net margins and profitability if not successfully managed.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $406.463 for Hubbell based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $450.0, and the most bearish reporting a price target of just $352.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.6 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 25.7x, assuming you use a discount rate of 7.9%.

- Given the current share price of $348.31, the analyst price target of $406.46 is 14.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.