Last Update 16 Aug 25

Fair value Increased 5.13%Analysts have raised their price target for AZZ to $125.89, citing consistent execution, a stronger balance sheet, improved margins, and favorable market and policy dynamics that support sustained growth and free cash flow.

Analyst Commentary

- Bullish analysts see AZZ as a quality franchise focused on profitable growth.

- Recent analyst model updates reflect consistent execution and a strengthened balance sheet, increasing capital allocation flexibility.

- Improved sales and margins, market share growth, and reduced debt position AZZ to sustain free cash flow.

- Recent quarterly results prompted increased estimates and higher price targets, signaling confidence in ongoing performance.

- Near-term optimism is supported by U.S. steel price support and expected tariff benefits, with favorable medium-term demand and supply dynamics for U.S.-focused steel companies.

What's in the News

- The Board of Directors authorized a fiscal first quarter 2026 cash dividend of $0.20 per share, a 17.6% increase from the previous $0.17 per share.

- AZZ Inc. was dropped from multiple Russell value and small cap indices, including the Russell 2000, 2500, 3000, and related value and defensive indices.

- The company was added to the Russell 2000 Dynamic Index.

- From March 1 to May 31, 2025, no shares were repurchased under the existing buyback program; cumulatively, 932,651 shares (3.71%) have been repurchased for $46.81 million since the buyback's inception.

- AZZ Inc. scheduled an Analyst/Investor Day event.

Valuation Changes

Summary of Valuation Changes for AZZ

- The Consensus Analyst Price Target has risen from $119.75 to $125.89.

- The Consensus Revenue Growth forecasts for AZZ has fallen from 5.5% per annum to 5.0% per annum.

- The Future P/E for AZZ has risen slightly from 23.78x to 24.66x.

Key Takeaways

- Strategic investments in technology and infrastructure expansion are expected to boost operating efficiency, revenue growth, and elevate net margins.

- AZZ's focus on debt reduction, market share expansion, and infrastructure demand positions it for long-term value enhancement and income margin improvement.

- Adverse weather, tariff uncertainties, competition, new facility execution risks, and acquisition challenges could affect AZZ's operational reliability, margins, and market position.

Catalysts

About AZZ- Provides hot-dip galvanizing and coil coating solutions in North America.

- AZZ's new greenfield facility near St. Louis, Missouri is ramping up production, which could drive future revenue growth as it expands capacity and taps into strong local demand. This investment is expected to positively impact earnings as the facility becomes fully operational and contributes to higher sales volumes.

- AZZ plans to continue strengthening its balance sheet by paying down debt and improving capital allocation, which should reduce interest expenses and enhance net income margins over time as borrowing costs are minimized.

- The company's strategic investments in enterprise-wide technologies, such as enhancing the Digital Galvanizing System (DGS), aim to improve operating productivity and efficiency, which could lead to higher net margins through cost savings and improved operational performance.

- AZZ is actively pursuing bolt-on acquisitions and expanding market share, which are expected to drive revenue growth and operational synergies. This inorganic growth strategy, alongside organic expansion, positions the company to enhance long-term shareholder value and improve net margins.

- The anticipated continuation of infrastructure spending related to the AIIJA program and urbanization trends will likely boost demand for AZZ's services, supporting top-line growth. This sustained strong demand, especially in bridge, highway, transmission, and distribution projects, is expected to positively impact revenue.

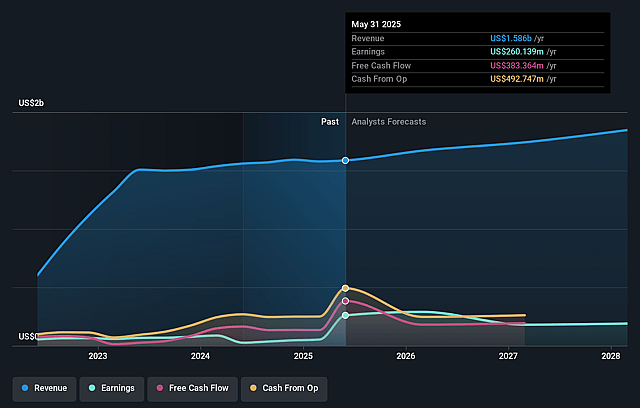

AZZ Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AZZ's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 16.4% today to 10.6% in 3 years time.

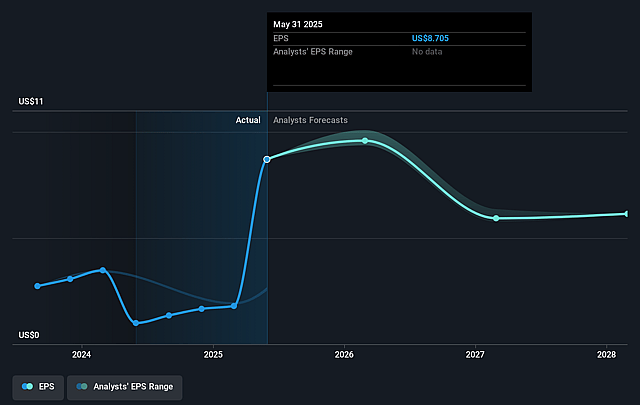

- Analysts expect earnings to reach $195.5 million (and earnings per share of $6.46) by about September 2028, down from $260.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.7x on those 2028 earnings, up from 13.1x today. This future PE is greater than the current PE for the US Building industry at 23.0x.

- Analysts expect the number of shares outstanding to grow by 0.46% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.49%, as per the Simply Wall St company report.

AZZ Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The fourth quarter results were negatively impacted by adverse weather, leading to over 200 days of lost production, which could affect seasonal earnings reliability in future periods if such conditions persist.

- Uncertainty around tariffs could lead to volatility in the availability and cost of materials, which might impact margins if costs cannot be fully passed on to customers.

- There is potential for increased competition in the U.S. as reshoring trends may bring in new market participants, possibly affecting AZZ's revenue and market share.

- With the ramp-up of new facilities such as the Washington aluminum coil coating plant, there exists execution risk associated with achieving expected production efficiencies, which could impact net margins if delays or inefficiencies occur.

- While there is a focus on acquisitions, the successful integration of new businesses without disrupting current operations is necessary to maintain earnings growth, and there is always acquisition-related risk that could affect financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $125.889 for AZZ based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $141.0, and the most bearish reporting a price target of just $105.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.8 billion, earnings will come to $195.5 million, and it would be trading on a PE ratio of 24.7x, assuming you use a discount rate of 8.5%.

- Given the current share price of $113.63, the analyst price target of $125.89 is 9.7% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.