Key Takeaways

- Strategic acquisitions and investments in technology sectors are poised to drive growth and improve margins for Applied Industrial Technologies.

- Renewed capital strategies suggest increased shareholder returns through buybacks and dividends, solidifying financial commitments.

- Potential ongoing revenue challenges and unsustainable margin improvements threaten earnings, amid macroeconomic headwinds and weak sales in major end markets.

Catalysts

About Applied Industrial Technologies- Distributes industrial motion, power, control, and automation technology solutions in the United States, Canada, Mexico, Australia, New Zealand, Singapore, and Costa Rica.

- The strategic acquisition of Hydradyne is expected to enhance Applied Industrial Technologies' position in the fluid power market, expand their footprint, and offer cross-selling opportunities, which could drive future revenue growth.

- Investments in the Engineered Solutions segment and automation business are anticipated to capitalize on secular trends like IoT and machine vision, expected to improve revenue and drive margin expansion.

- Enhanced operational efficiencies and cost control measures, alongside internal margin enhancement initiatives, are projected to positively impact net margins and earnings in upcoming quarters.

- Positive order momentum and sales funnel development in the technology and semiconductor sectors indicate potential significant revenue growth, especially as these markets recover and investment accelerates.

- Capital deployment for share buybacks and increased dividends underscores a commitment to returning value to shareholders, likely boosting earnings per share and shareholder returns.

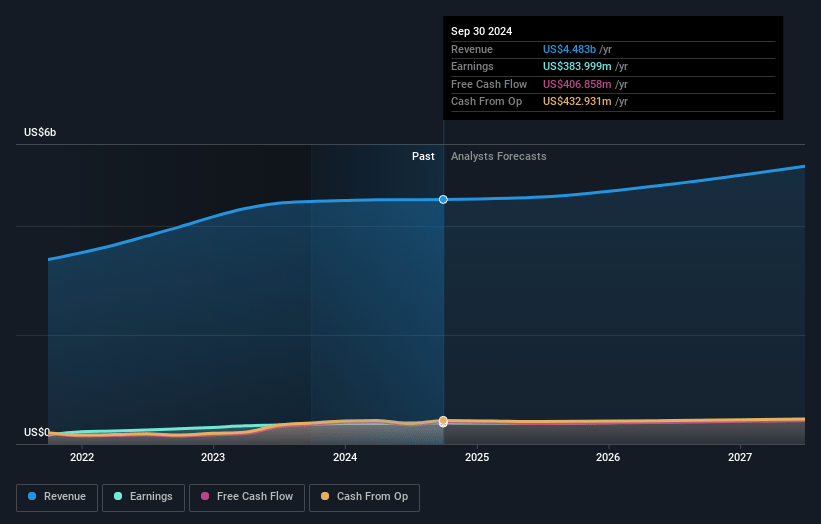

Applied Industrial Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Applied Industrial Technologies's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.6% today to 9.0% in 3 years time.

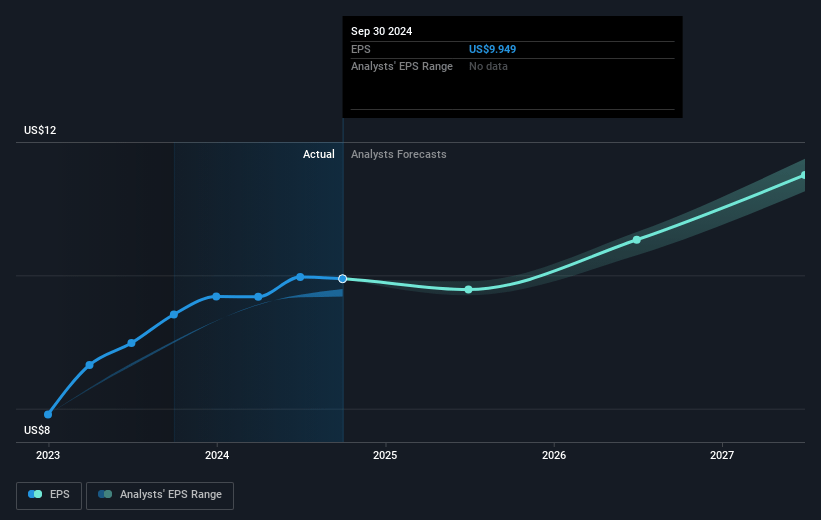

- Analysts expect earnings to reach $470.3 million (and earnings per share of $12.01) by about April 2028, up from $386.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.5x on those 2028 earnings, up from 22.1x today. This future PE is greater than the current PE for the US Trade Distributors industry at 19.0x.

- Analysts expect the number of shares outstanding to decline by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.27%, as per the Simply Wall St company report.

Applied Industrial Technologies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue has been negatively impacted by a decline in average daily sales, particularly in service center operations, due to reduced MRO spending, lower capital maintenance activity, and extended customer plant idling, indicating potential ongoing revenue challenges.

- Despite growth in some sectors, there has been significant sales weakness in major end markets such as machinery, transportation, oil and gas, and mining, potentially affecting overall revenue streams.

- The cost control and gross margin enhancements were attributed to temporary factors like lower LIFO expense, which may not be sustainable and could affect net margins if underlying operational improvements don't consistently materialize.

- The integration of the Hydradyne acquisition entails $1.5 million in transaction-related costs and a future increase in depreciation and amortization expenses, which could impact net margins and earnings if synergistic benefits are delayed or less than anticipated.

- Potential macroeconomic headwinds, including uncertainty over macro policies, interest rates, and potential tariff developments, could further dampen customer capital spending and industrial production, influencing future revenue growth and market demand.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $283.571 for Applied Industrial Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.2 billion, earnings will come to $470.3 million, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 7.3%.

- Given the current share price of $221.93, the analyst price target of $283.57 is 21.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.