Narratives are currently in beta

Key Takeaways

- International reseller network expansion and V-XR platform introduction could boost revenue through increased sales in diverse markets.

- Improved operational efficiencies and military channel penetration strategies may enhance profitability and drive substantial revenue growth.

- Delays in federal funding and strategic challenges are impacting VirTra's revenue stability, sales growth, and profitability, with long decision cycles causing further uncertainty.

Catalysts

About VirTra- Provides use of force training and firearms training simulators for the law enforcement, military, and commercial markets worldwide.

- VirTra's expansion of its international reseller network in regions like Canada, South America, and Europe is expected to drive further bookings growth, likely boosting revenue in international markets.

- The introduction of the V-XR platform, which offers flexible training options across various sectors, and its early positive reception could lead to increased sales and revenue growth in both traditional and new markets.

- Operational efficiencies and cost management improvements have increased gross margins, which can enhance net margins and overall profitability as the company scales.

- Strategic initiatives in penetrating military channels and advancements with the U.S. Army's IVAS program aim to capture a larger military market share, potentially leading to substantial revenue growth through large-scale contracts.

- Ongoing strategic investments in sales and marketing, alongside efforts to support customers in securing federal grants, are anticipated to accelerate sales growth and positively affect earnings as funding becomes more accessible.

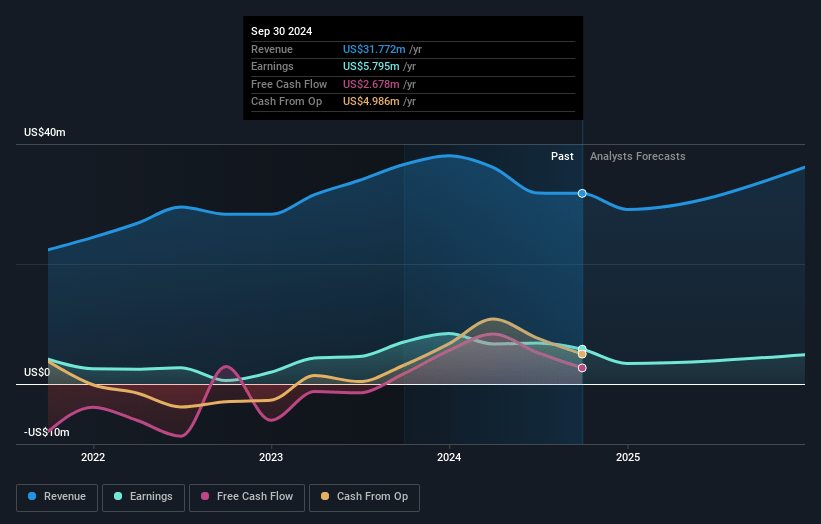

VirTra Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming VirTra's revenue will grow by 11.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 18.2% today to 9.7% in 3 years time.

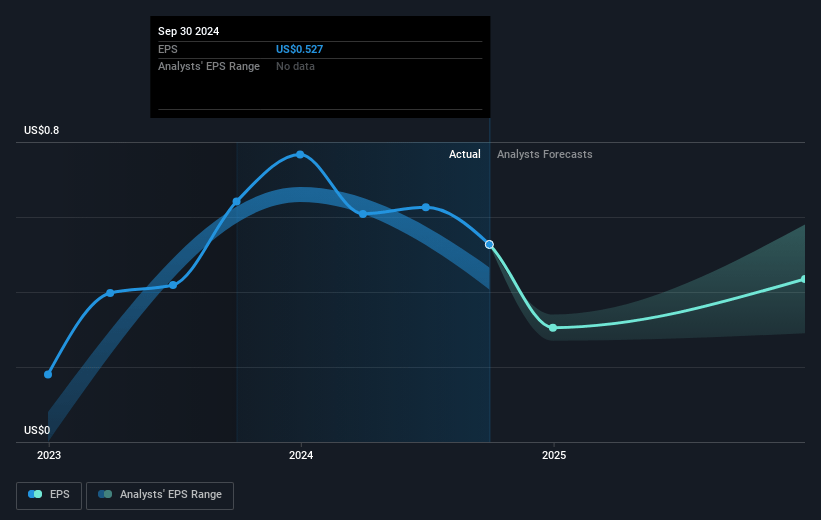

- Analysts expect earnings to reach $4.3 million (and earnings per share of $0.37) by about November 2027, down from $5.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.1x on those 2027 earnings, up from 14.4x today. This future PE is lower than the current PE for the US Aerospace & Defense industry at 34.3x.

- Analysts expect the number of shares outstanding to grow by 1.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.2%, as per the Simply Wall St company report.

VirTra Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- VirTra's government revenue decreased in Q3 due to federal funding delays and the time needed to rebuild its sales team, which could impact future revenue stability and growth prospects.

- The introduction of the V-XR platform faced initial delivery delays due to finalizing terms with a hardware provider, potentially affecting short-term sales growth and customer satisfaction.

- VirTra’s strategic investments in sales and marketing and increased hiring led to a significant rise in net operating expenses, impacting net margins and limiting immediate profitability.

- The company's focus on large-scale military contracts, which involve intricate and lengthy sales processes, presents uncertainty and potential delays in revenue recognition and earnings.

- Extended decision-making cycles and funding delays among government customers contributed to lower bookings in previous quarters, potentially affecting overall revenue and earnings growth trajectory.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $11.25 for VirTra based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.5, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $44.6 million, earnings will come to $4.3 million, and it would be trading on a PE ratio of 34.1x, assuming you use a discount rate of 6.2%.

- Given the current share price of $7.4, the analyst's price target of $11.25 is 34.2% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives