Key Takeaways

- Strong demand and strategic initiatives in the modular business and education sectors could drive future revenue growth.

- Favorable pricing and increased sales in the modular segment suggest potential for improved earnings and net margins.

- Terminated merger and industry challenges could impact McGrath RentCorp's growth strategies, rental revenue, and overall profitability amid economic uncertainties.

Catalysts

About McGrath RentCorp- Operates as a business-to-business rental company in the United States and internationally.

- The modular business has been showing strong growth due to strategic initiatives and increased demand from commercial and education sectors, which could drive future revenue growth.

- Positive quote activity in early 2025, particularly in Mobile Modular, suggests improving customer demand, potentially translating into higher future revenues.

- The $10 billion bond passed in California for school facilities indicates a significant potential boost for revenue growth in the Education segment, as projects move forward.

- Modular sales initiatives have led to increased sales revenues, benefiting from higher new equipment sales, which could further enhance future earnings.

- Pricing optimization and the gap between current fleet pricing and new shipment pricing indicate a favorable pricing tailwind, likely contributing to improved net margins in the modular segment.

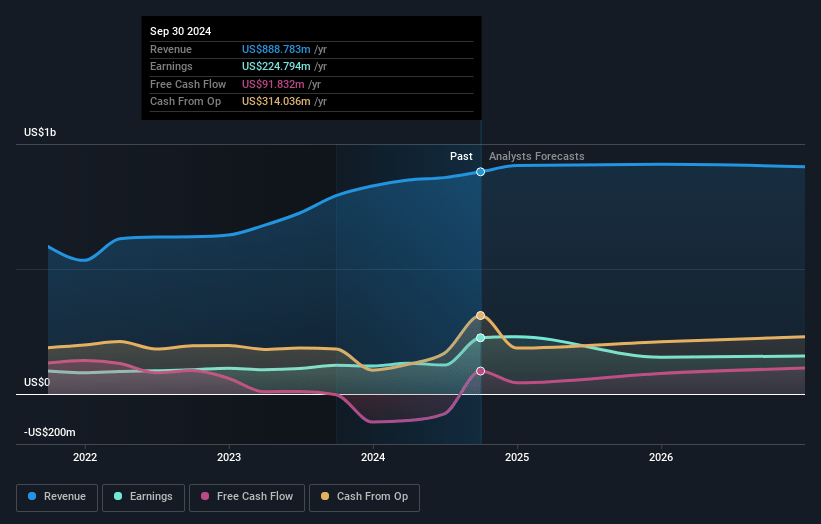

McGrath RentCorp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming McGrath RentCorp's revenue will grow by 4.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.4% today to 12.4% in 3 years time.

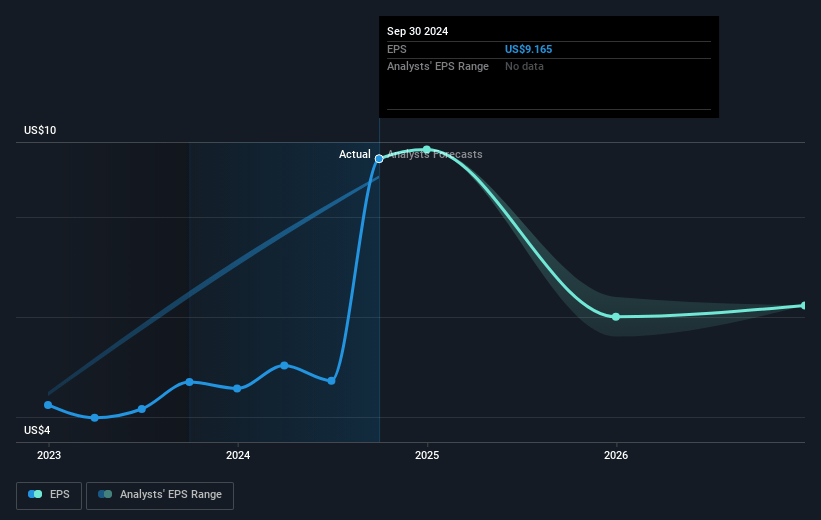

- Analysts expect earnings to reach $129.7 million (and earnings per share of $5.29) by about March 2028, down from $231.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.9x on those 2028 earnings, up from 11.7x today. This future PE is greater than the current PE for the US Trade Distributors industry at 18.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.73%, as per the Simply Wall St company report.

McGrath RentCorp Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The terminated merger with WillScot and the distractions it caused could be a risk to executing growth strategies, potentially impacting future revenue and earnings.

- Decreasing rental revenues and utilization in Portable Storage due to weaker demand and high interest rates could negatively affect net margins and overall profitability.

- The decline in rental revenues at TRS-RenTelco due to the industry-wide slowdown in test and measurement equipment markets reflects ongoing demand challenges, which could affect revenue and earnings.

- Strong revenue growth in sales compared to rental operations may lead to lower margins, impacting overall profitability despite increasing revenues.

- Ongoing macroeconomic challenges such as construction-related demand softness and interest rate impacts create uncertainty, which could affect revenue predictability and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $146.333 for McGrath RentCorp based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.0 billion, earnings will come to $129.7 million, and it would be trading on a PE ratio of 33.9x, assuming you use a discount rate of 7.7%.

- Given the current share price of $109.99, the analyst price target of $146.33 is 24.8% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives