Narratives are currently in beta

Key Takeaways

- Strong performance in refueling C-stores, grocery, and Display Solutions, plus robust EMI sales, signals potential revenue growth.

- Integration of EMI and strategic initiatives enhance operational efficiency, expecting improved margins and future earnings growth.

- Competitive pressures and external factors pose risks to sales, margins, and earnings, while integration challenges and timing delays could disrupt revenue predictability.

Catalysts

About LSI Industries- Produces and sells non-residential lighting and retail display solutions in the United States, Canada, Mexico, and Latin America.

- The robust project activity in the refueling C-store space, increased demand in the grocery market, and growth in the Display Solutions segment, along with strong sales from EMI, suggest increased future revenue potential.

- The successful integration of EMI, combined with strategic synergies in commercial and operational areas, is expected to yield cost savings and operational efficiencies, potentially improving net margins.

- The significant increase in grocery order rates and backlog, driven by transitioning to environmentally friendly R290 refrigerants, indicates potential for sustained revenue growth in the coming quarters.

- Expansion of the product line with the next generation of outdoor lighting products, like Velocity, is aligned with strategic investments in new product development, likely contributing to increased revenues and better margins.

- Strong cash flow generation, demonstrated by reducing net debt and maintaining a healthy balance sheet, provides financial flexibility for future growth investments or strategic acquisitions, potentially enhancing earnings growth.

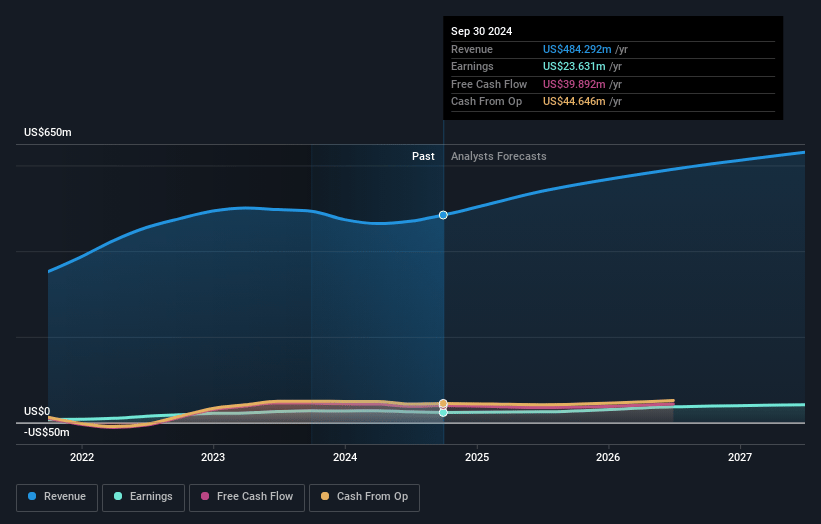

LSI Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LSI Industries's revenue will grow by 9.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.9% today to 6.8% in 3 years time.

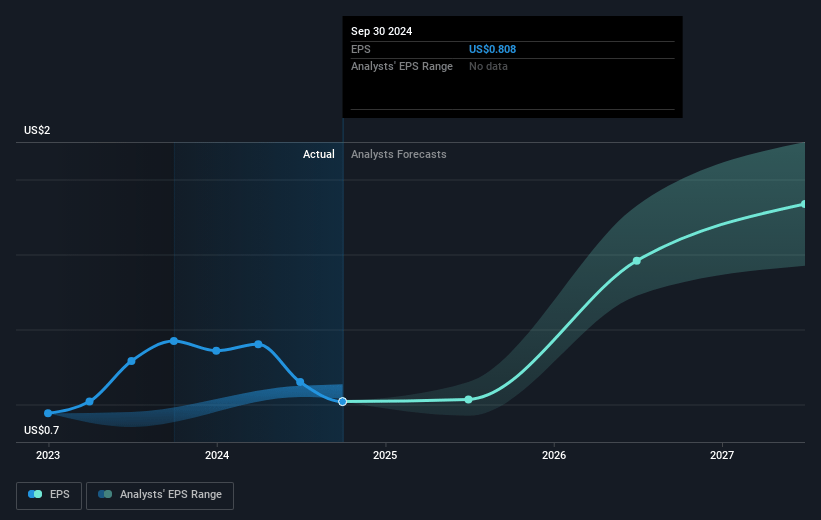

- Analysts expect earnings to reach $43.2 million (and earnings per share of $1.38) by about November 2027, up from $23.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $36.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.1x on those 2027 earnings, down from 24.4x today. This future PE is lower than the current PE for the US Electrical industry at 22.9x.

- Analysts expect the number of shares outstanding to grow by 2.83% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.39%, as per the Simply Wall St company report.

LSI Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Grocery segment faces uncertainty due to court hearings, potentially impacting sales and revenue if delays continue.

- Timing volatility and delays in large projects within the Lighting segment could affect revenue flow and create unpredictability in earnings.

- The integration of acquired company EMI, although progressing well, carries inherent risks that could disrupt operations and impact net margins if executed poorly.

- Competitive pressure in the C-store and grocery markets may affect LSI Industries' ability to maintain pricing power, directly impacting net margins.

- External factors, such as changing refrigerant standards and evolving administration policies, could impose additional costs and impact net earnings if not managed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $22.67 for LSI Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $639.5 million, earnings will come to $43.2 million, and it would be trading on a PE ratio of 20.1x, assuming you use a discount rate of 7.4%.

- Given the current share price of $20.02, the analyst's price target of $22.67 is 11.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives