Key Takeaways

- Reinvestment in higher-yielding securities and strategic deposit cost management could enhance net interest margins and earn growth.

- Wealth management expansion and increased C&I lending may boost noninterest income and drive future loan growth and revenue.

- Revenue and earnings may be negatively impacted by loan payoffs, security sales losses, and increased credit loss allowance due to economic concerns.

Catalysts

About Southside Bancshares- Operates as the bank holding company for Southside Bank that provides a range of financial services to individuals, businesses, municipal entities, and nonprofit organizations.

- The reinvestment of proceeds from the sale of lower-yielding securities into higher-yielding agency mortgage-backed securities could enhance net interest income and potentially improve net interest margin.

- The continued growth in the wealth management and trust department, resulting in more new clients and fee income, points to a potential increase in noninterest income.

- The initiative to expand commercial and industrial (C&I) lending in metropolitan markets by hiring additional relationship managers, with expected results in 2025, may drive future loan growth and revenue.

- A solid loan pipeline alongside recent loan growth, despite anticipated payoffs, suggests potential improvements in loan balances and revenue in the near future.

- The strategic management of deposit costs and wholesale funding, possibly allowing reductions in funding costs, can lead to an improvement in net interest margins, supporting earnings growth.

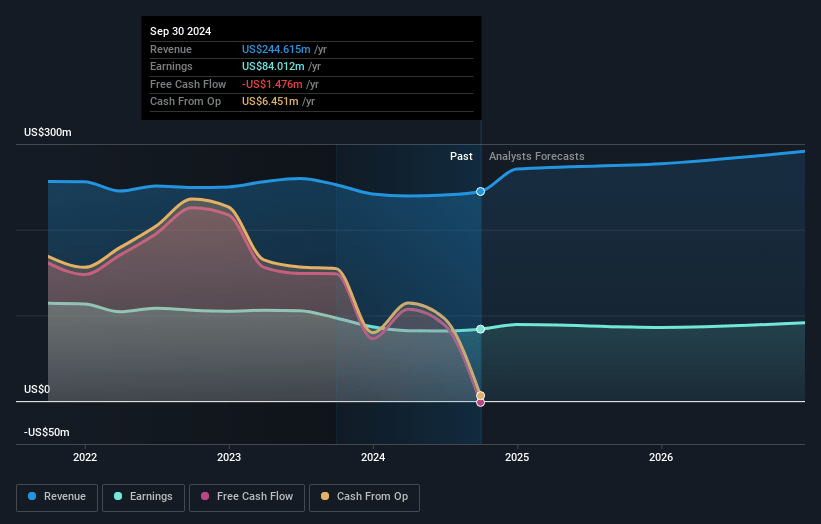

Southside Bancshares Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Southside Bancshares's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 34.3% today to 30.2% in 3 years time.

- Analysts expect earnings to reach $92.4 million (and earnings per share of $3.03) by about November 2027, up from $84.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.4x on those 2027 earnings, up from 13.0x today. This future PE is greater than the current PE for the US Banks industry at 12.9x.

- Analysts expect the number of shares outstanding to grow by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.08%, as per the Simply Wall St company report.

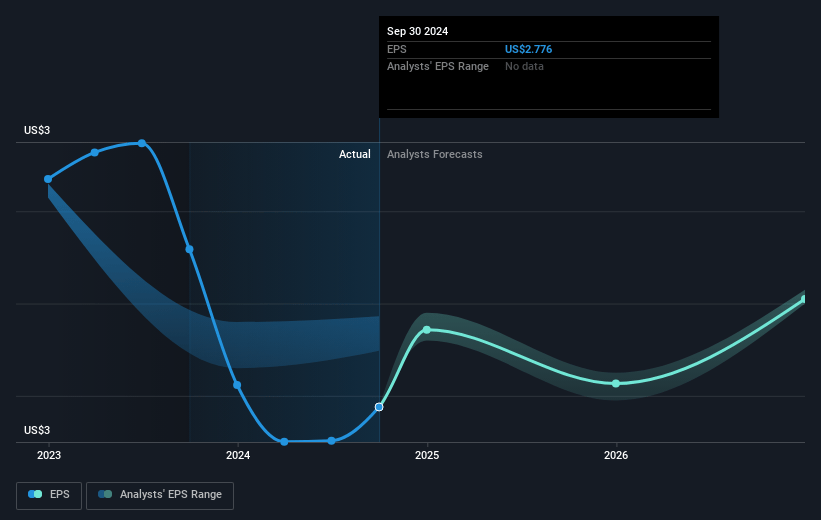

Southside Bancshares Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decrease in revenue due to loan payoffs and a reduction in target loan growth from 5% to 3% could negatively impact future earnings.

- The sale of lower-yielding securities and the unwind of fair value swaps resulted in a $1.9 million loss, which could lead to volatility in revenue and affect net margins.

- A net unrealized loss in the AFS securities portfolio of $24.7 million might impact the company's net earnings and financial health.

- The increase in the allowance for credit losses due to economic concerns forecasts, specifically in metro areas, might suggest a potential risk to asset quality, impacting net margins.

- Decrease in noninterest income by 16.7% due to impairment loss on AFS securities sales could affect overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $36.0 for Southside Bancshares based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $305.7 million, earnings will come to $92.4 million, and it would be trading on a PE ratio of 14.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $36.09, the analyst's price target of $36.0 is 0.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

WA

Consensus Narrative from 3 Analysts

Restructuring Mortgage-Backed Securities Will Reduce Volatility In 2025

Key Takeaways Restructuring the mortgage-backed securities portfolio and favorable interest rate conditions may boost net interest margins and income in 2025. Loan growth and strategic hires in wealth management are expected to enhance revenue, earnings, and profitability.

View narrativeUS$36.50

FV

16.9% undervalued intrinsic discount6.81%

Revenue growth p.a.

0users have liked this narrative

0users have commented on this narrative

0users have followed this narrative

8 days ago author updated this narrative