Narratives are currently in beta

Key Takeaways

- Strong fee business performance and loan growth, particularly in commercial real estate, could boost interest income and total revenue.

- Acquisition of Heartland Financial and optimized funding strategies may enhance growth and profitability through diversified business models and improved net interest margins.

- Heavy reliance on volatile non-interest income and interest-bearing deposits, along with integration and credit risks, could affect revenue and earnings stability.

Catalysts

About UMB Financial- Operates as the bank holding company that provides banking services and asset servicing in the United States and internationally.

- The company is expecting to see continued growth in revenue from strong performance in its fee business and loan growth, with particular strength in commercial real estate and C&I activities, which could boost interest income and total revenue.

- UMB is on track to complete the acquisition of Heartland Financial, which management believes will accelerate its growth strategy, diversify its business model, and be financially and strategically beneficial. This could positively impact revenue and earnings.

- UMB has seen growth in assets under administration and increased trading and investment banking volumes, particularly in municipal and mortgage-backed securities, which have driven a 30% increase in quarterly fee income. This could lead to further increases in net margins.

- The loan growth momentum, particularly from commercial real estate and multifamily sectors, combined with excellent credit quality, suggests the potential for rising net interest income and earnings.

- The company's plan to optimize its funding mix, such as reducing borrowing levels and managing deposit costs with interest rate cuts, is expected to improve net interest margin, enhancing earnings in future quarters.

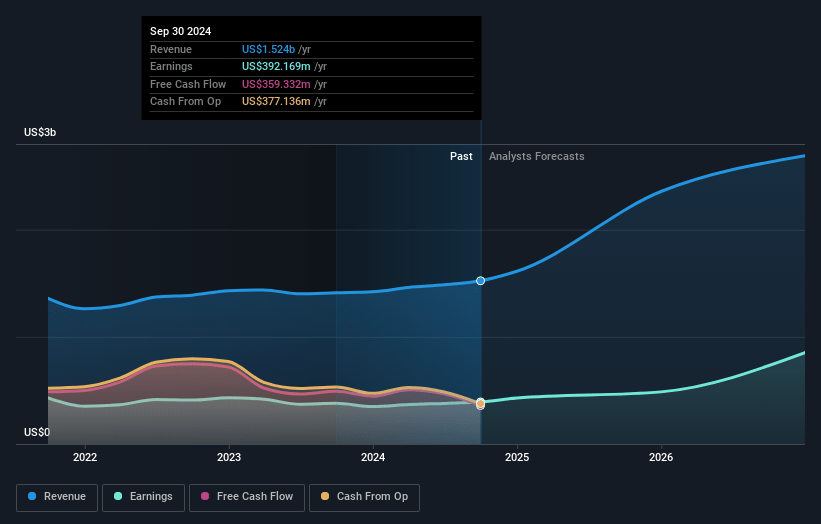

UMB Financial Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming UMB Financial's revenue will grow by 29.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.7% today to 31.0% in 3 years time.

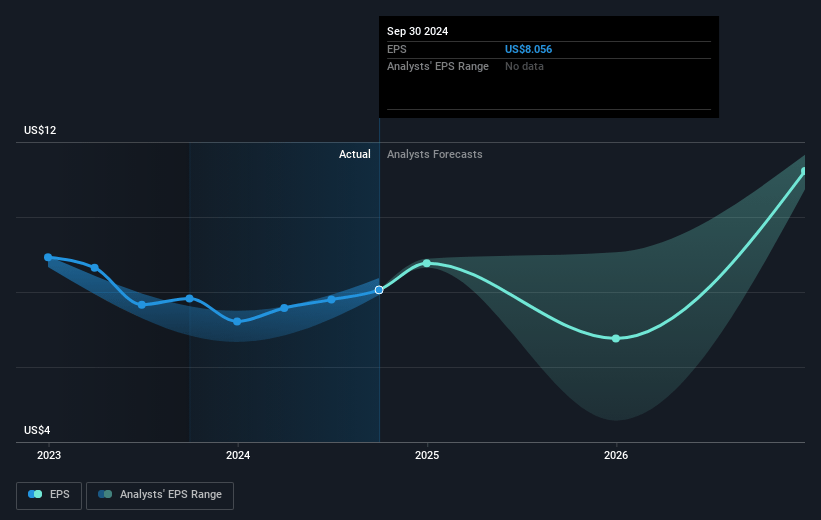

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $11.24) by about January 2028, up from $392.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.8x on those 2028 earnings, up from 13.7x today. This future PE is greater than the current PE for the US Banks industry at 12.2x.

- Analysts expect the number of shares outstanding to grow by 23.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.24%, as per the Simply Wall St company report.

UMB Financial Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company relies heavily on non-interest income from volatile sources such as trading volumes in municipal and mortgage-backed securities, which could impact revenue stability if market conditions change.

- UMB's growth in deposits partly depends on episodic events and seasonality, particularly in the public funds and asset servicing sectors, potentially affecting revenue if these patterns shift.

- The cost of interest-bearing deposits has been a challenge, with the bank relying on a high beta response to rate changes; failure to manage this effectively could compress net interest margins.

- The UMB's credit card portfolio acquisition, which possesses a different credit profile, could pose unknown risks in credit quality and result in increased credit losses, thus impacting net earnings.

- With plans for the pending acquisition of Heartland Financial, integration risks and the realization of projected synergies are pivotal and failure to achieve targeted cost saves could negatively influence the net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $138.89 for UMB Financial based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $156.0, and the most bearish reporting a price target of just $120.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.3 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 14.8x, assuming you use a discount rate of 6.2%.

- Given the current share price of $110.34, the analyst's price target of $138.89 is 20.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives