Key Takeaways

- Strategic international expansion and acquisitions are poised to enhance market penetration, operational efficiency, and net margins.

- Innovations in vehicle models and sustainability initiatives could drive sales growth, enhance brand reputation, and attract eco-conscious consumers.

- High financial leverage and operating losses, coupled with export halts, pose risks to Lotus Technology's profitability and future revenue growth.

Catalysts

About Lotus Technology- Engages in the design, development, and sale of battery electric lifestyle vehicles worldwide.

- Lotus Technology's expansion into new international markets, including GCC region, Asia, and Oceania, can lead to significant revenue growth by capturing new customer bases and increasing global market penetration.

- The strategic acquisition of 51% equity interest in Lotus U.K. will allow consolidation of operations, potentially increasing overall efficiency and reducing costs, thus positively impacting net margins.

- The introduction of new models and upgraded configurations, along with enhancements like the mapless urban NOA Navigation On Autopilot system, should boost vehicle sales and improve customer appeal, driving higher revenues.

- The company's focus on sustainable vehicle development and recognition in sustainability awards can enhance brand reputation and attract eco-conscious consumers, thereby supporting higher profit margins over time.

- Potential manufacturing initiatives in the U.S. could mitigate tariff impacts and enable more aggressive U.S. market penetration, supporting revenue growth and stabilizing margins despite geopolitical tensions.

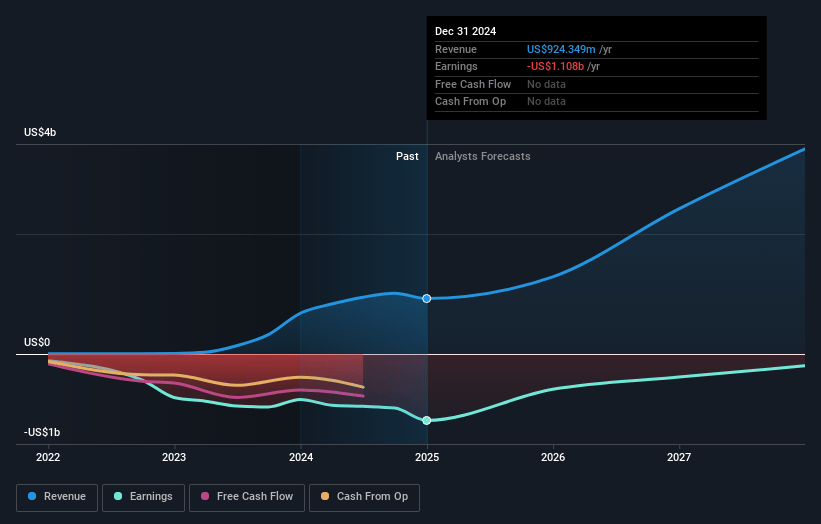

Lotus Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Lotus Technology's revenue will grow by 56.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -119.9% today to 1.7% in 3 years time.

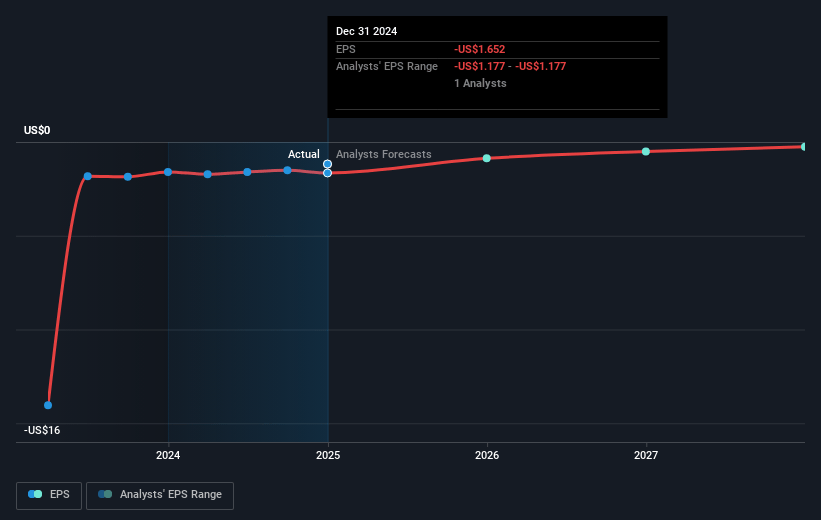

- Analysts expect earnings to reach $61.5 million (and earnings per share of $0.08) by about April 2028, up from $-1.1 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 78.5x on those 2028 earnings, up from -0.8x today. This future PE is greater than the current PE for the US Auto industry at 18.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.29%, as per the Simply Wall St company report.

Lotus Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Lotus Technology reported a significant operating loss of $786 million for the year 2024, with a net loss of $1,107 million, highlighting substantial financial challenges that could impact the company's long-term earnings potential.

- The gross profit margin was notably low at 3% for the full year, which may indicate difficulties in achieving profitability and could negatively affect net margins if not addressed.

- The geopolitical tensions and high U.S. tariffs have resulted in the company halting exports of its lifestyle vehicles to the U.S. market, potentially affecting future revenue growth in a major market.

- The company's high debt asset ratio of over 130% by the end of 2024 suggests a significant leverage risk, which could pose challenges to cash flow and balance sheet stability.

- There is uncertainty regarding the financial impact of the planned acquisition of 51% of Lotus UK, as it's still subject to due diligence and potential regulatory approvals, which could further influence financial stability and shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.0 for Lotus Technology based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.5 billion, earnings will come to $61.5 million, and it would be trading on a PE ratio of 78.5x, assuming you use a discount rate of 13.3%.

- Given the current share price of $1.29, the analyst price target of $4.0 is 67.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.