Key Takeaways

- SCB X's digital strategy and wealth management focus support revenue growth, with improved asset quality and RM productivity boosting net margins.

- Strategic efforts in yield improvement and expense management enhance earnings growth and financial stability, minimizing NIM risks.

- Economic challenges, including high household debt and subdued GDP growth in Thailand, threaten SCB X's revenues, profit margins, and future expansion.

Catalysts

About SCB X- Operates as a holding company for The Siam Commercial Bank Public Company Limited that provides various financial products and services.

- SCB X's digital strategy and focus on wealth management have led to double-digit growth in wealth management fees, which is expected to positively impact future revenue as capital market conditions improve and RM productivity increases.

- The stabilization and potential improvement in asset quality, particularly with a decline in NPL formation, may contribute to better net margins by reducing credit costs, especially as CardX shows signs of stabilization and performance improvement.

- The company's strategic efforts to improve yield and Net Interest Margin (NIM) through corporate loan yield increases indicate potential future earnings growth, especially with improved tourism industry contributions.

- SCB X's proactive measures to manage operational expenses and optimize cost-to-income ratios signal potential for enhancing net margins, as the company continues to control costs while facing seasonal marketing expenses.

- Ongoing improvements in the Gen 2 business, coupled with strategic adjustments in underwriting models and collections, may support future earnings growth and mitigate NIM downside risks, contributing to overall financial stability.

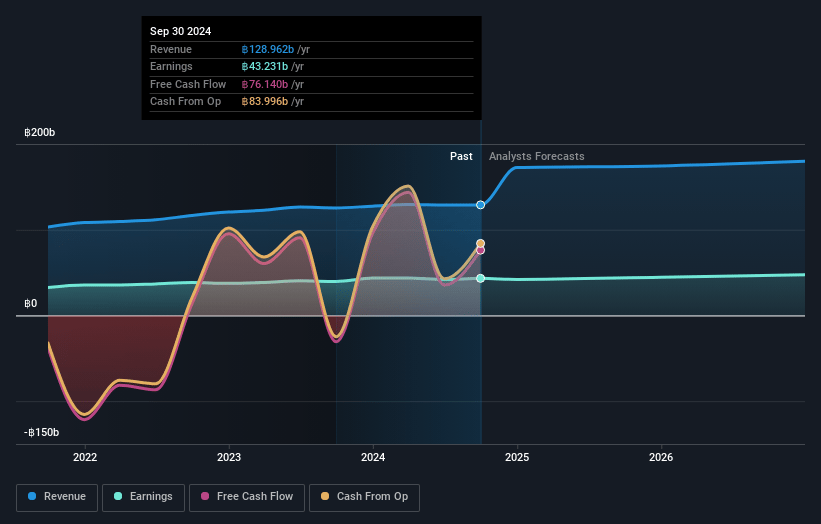

SCB X Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming SCB X's revenue will grow by 11.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 33.9% today to 27.9% in 3 years time.

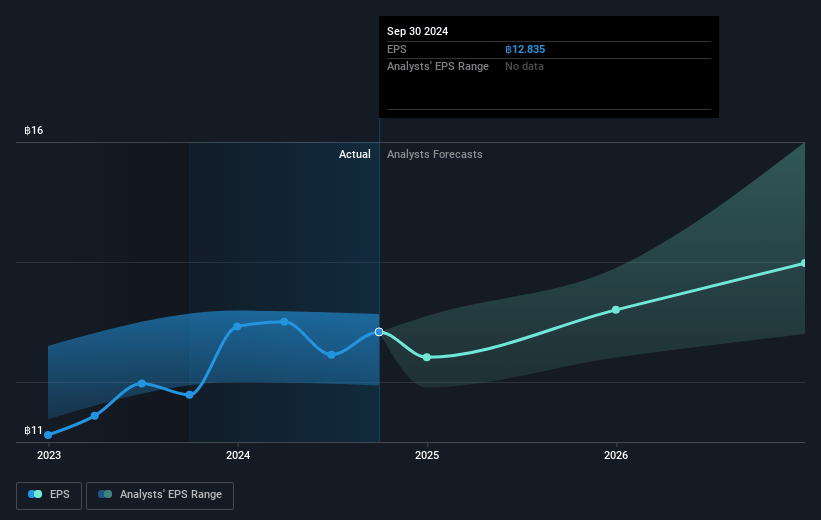

- Analysts expect earnings to reach THB 50.3 billion (and earnings per share of THB 14.91) by about January 2028, up from THB 43.9 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, up from 9.7x today. This future PE is greater than the current PE for the TH Banks industry at 7.9x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.05%, as per the Simply Wall St company report.

SCB X Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- High household debt in Thailand poses a significant economic risk, potentially leading to reduced consumer spending and therefore negatively affecting SCB X's revenues and profit margins.

- Subdued GDP growth projections in Thailand, alongside declining competitiveness in exports, may result in slower overall economic growth, which can impact SCB X's future earnings and expansion capabilities.

- A downward revision in private consumption due to low agricultural income and weakened consumer credit could lead to decreased demand for financial products and services provided by SCB X, affecting its revenue.

- Rate cuts by the Bank of Thailand are likely to compress SCB X’s net interest margins (NIM), impacting overall earnings if loan growth does not offset the reduced income from interest.

- Potential increased credit costs due to deteriorating credit quality and heightened lending standards pose a risk to SCB X's profitability, as they could lead to higher provisions and reduced net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of THB126.24 for SCB X based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of THB140.0, and the most bearish reporting a price target of just THB100.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be THB180.3 billion, earnings will come to THB50.3 billion, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of THB126.0, the analyst's price target of THB126.24 is 0.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives