Key Takeaways

- Strategic acquisitions and project completions are poised to enhance Boliden's resource base, capacity, and profitability, driving future revenue and earnings growth.

- Dividend cancellation to fund investments is aimed at maintaining long-term financial health and fostering future earnings growth.

- Fluctuating earnings, unstable cash flow, canceled dividends, and operational risks may pressure Boliden's stock and investor confidence amidst favorable metal prices.

Catalysts

About Boliden- Engages in the extracting, producing, and recycling of base metals in Sweden, Finland, other Nordic region, Germany, the United Kingdom, Europe, North America, and internationally.

- The completion of the dam project at Aitik sets the stage for increased throughput and improved operational efficiency, which could drive higher future revenues and better margins as the project reduces current constraints.

- Strategic acquisitions, including the Lundin mines in Neves-Corvo and Zinkgruvan, are expected to expand Boliden's resource base and production capacity, potentially boosting revenue growth and enhancing long-term earnings prospects.

- The expansion project at Odda, with a completion milestone reached, aims to increase production capacity and profitability, contributing to future revenue and earnings growth once fully operational.

- Exploration successes, particularly in Garpenberg with a large increase in mineral resources, indicate potential for extending mine life and increasing production, likely bolstering future revenues and sustaining earnings growth.

- The strategic decision to cancel the dividend to partially fund acquisitions can preserve cash for key investments, supporting long-term financial health and future earnings growth.

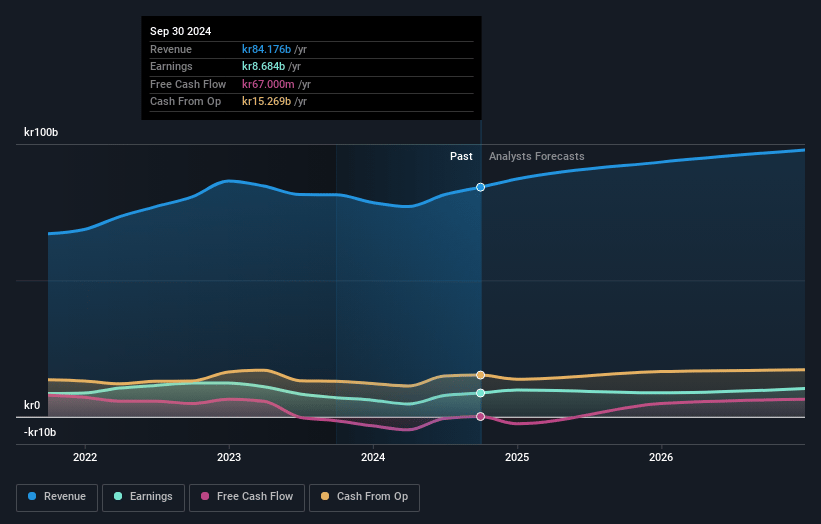

Boliden Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Boliden's revenue will grow by 3.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.2% today to 12.1% in 3 years time.

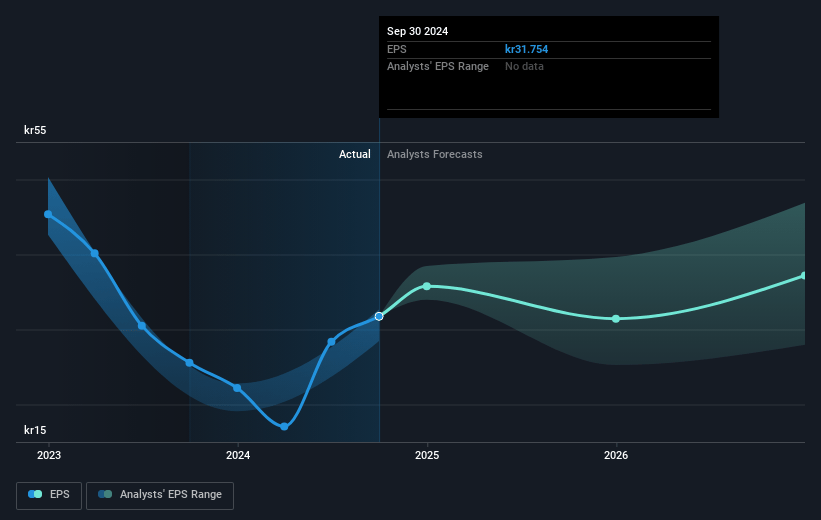

- Analysts expect earnings to reach SEK 11.8 billion (and earnings per share of SEK 43.87) by about March 2028, up from SEK 10.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting SEK16.8 billion in earnings, and the most bearish expecting SEK8.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.9x on those 2028 earnings, which is the same as it is today today. This future PE is lower than the current PE for the GB Metals and Mining industry at 13.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.27%, as per the Simply Wall St company report.

Boliden Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The strong Q4 profit, which included a significant one-off insurance claim of SEK 935 million, might not be sustainable in the future, leading to potential fluctuations in earnings.

- The company faces volatility in cash flow, which currently appears strong due to timing issues and reduced working capital, but is acknowledged as being unstable, potentially impacting future cash reserves.

- The decision to cancel dividends to finance acquisitions could impact investor confidence, resulting in potential pressure on the stock price and affecting shareholder returns.

- There are operational risks, such as limited production in certain areas due to environmental permits, and completed projects like the Aitik dam did not immediately improve production figures, affecting throughput and net margins.

- Pressure from lower treatment charges, especially in zinc smelters, could squeeze future profit margins despite favorable current metal prices, impacting overall revenue and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK355.571 for Boliden based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK500.0, and the most bearish reporting a price target of just SEK290.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK97.6 billion, earnings will come to SEK11.8 billion, and it would be trading on a PE ratio of 9.9x, assuming you use a discount rate of 6.3%.

- Given the current share price of SEK363.7, the analyst price target of SEK355.57 is 2.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.